Concept explainers

Videos

Finlon Upholstery, Inc. uses a

Finlon applies manufacturing

Job no. 2077 was completed in January 20x2; there was no work in process at year-end. All jobs produced during 20x2 were sold with the exception of job no. 2143, which contained direct-material costs of $156,000 and direct-labor charges of $85,000. The company charges any under- or overapplied overhead to Cost of Goods Sold.

Required:

- 1. Determine the company’s predetermined overhead application rate.

- 2. Determine the additions to the Work-in-Process Inventory account for direct material used, direct labor, and manufacturing overhead.

- 3. Compute the amount that the company would disclose as finished-goods inventory on the December 31, 20x2, balance sheet.

- 4. Prepare the

journal entry needed to record the year’s completed production. - 5. Compute the amount of under- or overapplied overhead at year-end, and prepare the necessary journal entry to record its disposition.

- 6. Determine the company’s 20x2 cost of goods sold.

- 7. Would it be appropriate to include selling and administrative expenses in either manufacturing overhead or cost of goods sold? Briefly explain.

1.

Calculate the amount of Company F’s predetermined overhead application rate.

Explanation of Solution

Predetermined Overhead Rate: Predetermined overhead rate is a measure used to allocate the estimated manufacturing overhead cost to the products or job orders during a particular period. This is generally evaluated at the beginning of each reporting period. The evaluation takes into account the estimated manufacturing overhead cost and the estimated allocation base that includes direct labor hours, direct labor in dollars, machine hours and direct materials.

Calculate the amount of Company F’s predetermined overhead application rate.

Thus, the amount of Company F’s predetermined overhead application rate is 130% of direct labor cost.

2.

Calculate the additions that are made to the work-in-process inventory account for direct materials used, direct labor, and manufacturing overhead.

Explanation of Solution

Work-in-process is the middle part of raw materials and finished goods. This inventory is the portion of the manufactured inventory for which the process has been started but not yet completed.

Calculate the additions that are made to the work-in-process inventory account for direct materials used, direct labor, and manufacturing overhead.

| Particulars | Amount ($) |

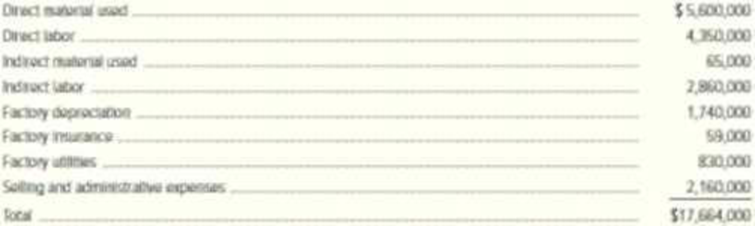

| Direct materials used | $5,600,000 |

| Direct labor | $4,350,000 |

| Manufacturing overhead | $5,655,000 |

| Total | $15,605,000 |

Table (1)

Thus, the total addition (debits) made to work-in process inventory account is $15,605,000.

3.

Identify the amount that would be disclosed by the company as finished goods inventory on the balance sheet as of December 31, 20x2.

Explanation of Solution

Finished goods inventory are completely ready for sale after completing the production process.

The amount that would be disclosed by the company as finished goods inventory on the balance sheet as of December 31, 20x2 is $351,500

4.

Prepare the journal entry in the books of Company F to record the year’s completed production.

Explanation of Solution

Prepare the journal entry in the books of Company F to record the year’s completed production.

| Date | Account title and explanation | Debit ($) | Credit ($) |

| Finished-goods inventory | 15,761,800 | ||

| Work-in-process inventory | 15,761,800 | ||

| (To record the company’s completed production) |

Table (2)

5.

Calculate the amount of under-applied or over-applied at year end and record its disposition.

Explanation of Solution

Under-applied overhead:

When there is a debit balance in the manufacturing overhead account during the month end, it indicates that overheads applied to jobs are less than the actual overhead cost incurred by the business. Therefore, the debit balance in the manufacturing overhead account is referred to as under-applied overhead.

Over-applied overhead:

When there is a credit balance in the manufacturing overhead account during the month end, indicates that overheads applied to jobs is more than the actual overhead cost incurred by the business. Therefore, the credit balance in the manufacturing overhead account is referred to as over- applied overhead.

Step 1: calculate the amount of actual overhead.

| Particulars | Amount ($) |

| Indirect materials used | $65,000 |

| Indirect labor | $2,860,000 |

| Factory depreciation | $1,740,000 |

| Factory insurance | $59,000 |

| Factory utilities | $830,000 |

| Total | $5,554,000 |

Table (3)

Step 2: Calculate the amount of under-applied or over-applied overhead.

Working note (1):

Calculate the amount of applied overhead.

Thus, the overhead is over-applied by $101,000.

Prepare the journal entry.

| Date | Account title and explanation | Debit ($) | Credit ($) |

| Manufacturing overhead | 101,000 | ||

| Cost of goods sold | 101,000 | ||

| (To record the company’s completed production) |

Table (4)

6.

Calculate the cost of goods sold of Company F for the year 20x2.

Explanation of Solution

Cost of goods sold: Cost of goods sold is the total of all the expenses incurred by a company to sell the goods during the given period.

Calculate the cost of goods sold of Company F for the year 20x2.

| Particulars | Amount ($) |

| Finished-goods inventory, January 1 | $0 |

| Add: Cost of goods manufactured | $15,761,800 |

| Cost of goods available for sale | $15,761,800 |

| Less: Finished-goods inventory, December 31 | $351,500 |

| Unadjusted cost of goods sold | $15,410,300 |

| Less: Over applied overhead | $101,000 |

| Cost of goods sold | $15,309,300 |

Table (5)

Thus, the amount of cost of goods sold is $15,309,300.

7.

Explain whether it would be appropriate to include selling and administrative expenses in either manufacturing overhead or cost of goods sold.

Explanation of Solution

Selling and administrative expenses are the operating expenses of the company. These costs are considered as the period cost rather than the product costs. Hence, these costs are unrelated to manufacturing overhead and cost of goods sold. Thus, it cannot be included.

Want to see more full solutions like this?

Chapter 3 Solutions

Connect 1-Semester Access Card for Managerial Accounting: Creating Value in a Dynamic Business Environment (NEW!!)

- Channel Products Inc. uses the job order cost system of accounting. The following is a list of the jobs completed during March, showing the charges for materials issued to production and for direct labor. Assume that factory overhead is applied on the basis of direct labor costs and that the predetermined rate is 200%. Required: Compute the amount of overhead to be added to the cost of each job completed during the month. Compute the total cost of each job completed during the month. Compute the total cost of producing all the jobs finished during the month.arrow_forwardBaldwin Printing Company uses a job order cost system and applies overhead based on machine hours. A total of 150,000 machine hours have been budgeted for the year. During the year, an order for 1,000 units was completed and incurred the following: The accountant computed the inventory cost of this order to be 4.30 per unit. The annual budgeted overhead in dollars was: a. 577,500. b. 600,000. c. 645,000. d. 660,000.arrow_forwardThe cost accountant for River Rock Beverage Co. estimated that total factory overhead cost for the Blending Department for the coming fiscal year beginning February 1 would be 3,150,000, and total direct labor costs would be 1,800,000. During February, the actual direct labor cost totalled 160,000, and factory overhead cost incurred totaled 283,900. a. What is the predetermined factory overhead rate based on direct labor cost? b. Journalize the entry to apply factory overhead to production for February. c. What is the February 28 balance of the account Factory OverheadBlending Department? d. Does the balance in part (c) represent over- or underapplied factory overhead?arrow_forward

- Abbey Products Company is studying the results of applying factory overhead to production. The following data have been used: estimated factory overhead, 60,000; estimated materials costs, 50,000; estimated direct labor costs, 60,000; estimated direct labor hours, 10,000; estimated machine hours, 20,000; work in process at the beginning of the month, none. The actual factory overhead incurred for November was 80,000, and the production statistics on November 30 are as follows: Required: 1. Compute the predetermined rate, based on the following: a. Direct labor cost b. Direct labor hours c. Machine hours 2. Using each of the methods, compute the estimated total cost of each job at the end of the month. 3. Determine the under-or overapplied factory overhead, in total, at the end of the month under each of the methods. 4. Which method would you recommend? Why?arrow_forwardGeneva, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountants before making any allocations: The total cost of purchasing and receiving parts used in manufacturing is 60,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were 48,000 and 12,000 for X and Y, respectively. If an activity-based system is used, what would be the allocated costs for each product?arrow_forwardOReilly Manufacturing Co.s cost of goods sold for the month ended July 31 was 345,000. The ending work in process inventory was 90% of the beginning work in process inventory. Factory overhead was 50% of the direct labor cost. No indirect materials were used during the period. Other information pertaining to OReillys inventories and production for July is as follows: Required: 1. Prepare a statement of cost of goods manufactured for the month of July. (Hint: Set up a statement of cost of goods manufactured, putting the given information in the appropriate spaces and solving for the unknown information. Start by using cost of goods sold to solve for the cost of goods manufactured.) 2. Prepare a schedule to compute the prime cost incurred during July. 3. Prepare a schedule to compute the conversion cost charged to Work in Process during July.arrow_forward

- Kenkel, Ltd. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 80,000. b. Requisitioned raw materials to production, 80,000. c. Distributed direct labor costs, 10,000. d. Factory overhead costs incurred, 60,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 225,000, on account.arrow_forwardDavis Co. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 70,000. b. Requisitioned raw materials to production, 70,000. c. Distributed direct labor costs, 15,000. d. Factory overhead costs incurred, 45,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 195,000, on account. (Hint: Use a single account for raw materials and work in process.)arrow_forwardDuring March, the following costs were charged to the manufacturing department: $14886 for materials; $14,656 for labor; and $13,820 for manufacturing overhead. The records show that 30,680 units were completed and transferred, while 2,400 remained in ending inventory. There were 33,080 equivalent units of material and 31,640 of conversion costs. Using the weighted-average method, what is the cost of inventory transferred and the balance in work in process inventory?arrow_forward

- The following information, taken from the books of Herman Brothers Manufacturing represents the operations for January: The job cost system is used, and the February cost sheet for Job M45 shows the following: The following actual information was accumulated during February: Required: 1. Using the January data, ascertain the predetermined factory overhead rates to be used during February, based on the following: a. Direct labor cost b. Direct labor hours c. Machine hours 2. Prepare a schedule showing the total production cost of Job M45 under each method of applying factory overhead. 3. Prepare the entries to record the following for February operations: a. The liability for total factory overhead. b. Distribution of factory overhead to the departments. c. Application of factory overhead to the work in process in each department, using direct labor hours. (Use the predetermined rate calculated in Requirement 1.) d. Closing of the applied factory overhead accounts. e. Recording under- and overapplied factory overhead and closing the actual factory overhead accounts.arrow_forwardLeen Production Co. uses the job order cost system of accounting. The following information was taken from the companys books after all posting had been completed at the end of May: a. Compute the total production cost of each job. b. Prepare the journal entry to transfer the cost of jobs completed to Finished Goods. c. Compute the selling price per unit for each job, assuming a mark-on percentage of 40%. d. Prepare the journal entries to record the sale of Job 1065.arrow_forwardHigh-End Products Inc. uses a standard cost system in accounting for the cost of production of its only product, Swank. The standards for the production of one unit of Swank follow: Direct materials: 10 feet of Class at $.75 per foot and 3 feet of Chic at $1.00 per foot. Direct labor: 4 hours at $12.00 per hour. Factory overhead: applied at 150% of standard direct labor costs. There was no beginning inventory on hand at July 1. Following is a summary of costs and related data for the production of Swank during the following year ended June 30: 100,000 feet of Class were purchased at $.72 per foot. 30,000 feet of Chic were purchased at $1.05 per foot. 8,000 units of Swank were produced that required 78,000 feet of Class, 26,000 feet of Chic, and 31,000 hours of direct labor at $11.80 per hour. 6,000 units of product Swank were sold. On June 30, there are 22,000 feet of Class, 4,000 feet of Chic, and 2,000 completed units of Swank on hand. All purchases and transfers are “charged in” at standard. Required: Calculate the following, using the formulas on pages 421–422 and 424 and compute the materials variances for both Class and Chic: Materials quantity variance. Materials purchase price variance. Labor efficiency variance. Labor rate variance.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,