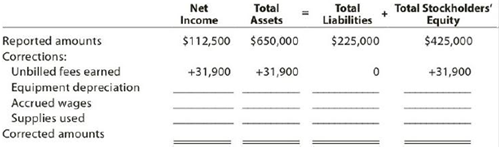

Adjusting entries and errors At the end of August, the first month of operations, the following selected data were taken from the financial statements of Tucker jacobs, an attorney: Net income for August $112,500 Total assets at August 31 650,000 Total liabilities at August 31 225,000 Total stockholders’ equity at August 31 425,000 In preparing the financial statements, adjustments for the following data were overlooked: Unbilled fees earned at August 31, $31,900. Depreciation of equipment for August, $7,500. Accrued wages at August 31, $5,200. Supplies used during August, $3,000. Instructions 1. journalize the entries to record the omitted adjustments. 2. Determine the correct amount of net income for August and the total assets, liabilities, and stockholders’ equity at August 31. In addition to indicating the corrected amounts, indicate the effect of each omitted adjustment by setting up and completing a columnar table similar to the following. The first adjustment is presented as an example.

Adjusting entries and errors At the end of August, the first month of operations, the following selected data were taken from the financial statements of Tucker jacobs, an attorney: Net income for August $112,500 Total assets at August 31 650,000 Total liabilities at August 31 225,000 Total stockholders’ equity at August 31 425,000 In preparing the financial statements, adjustments for the following data were overlooked: Unbilled fees earned at August 31, $31,900. Depreciation of equipment for August, $7,500. Accrued wages at August 31, $5,200. Supplies used during August, $3,000. Instructions 1. journalize the entries to record the omitted adjustments. 2. Determine the correct amount of net income for August and the total assets, liabilities, and stockholders’ equity at August 31. In addition to indicating the corrected amounts, indicate the effect of each omitted adjustment by setting up and completing a columnar table similar to the following. The first adjustment is presented as an example.

Solution Summary: The author explains the rules of debiting and crediting different accounts while they occur in business transactions.

At the end of August, the first month of operations, the following selected data were taken from the financial statements of Tucker jacobs, an attorney:

Net income for August

$112,500

Total assets at August 31

650,000

Total liabilities at August 31

225,000

Total stockholders’ equity at August 31

425,000

In preparing the financial statements, adjustments for the following data were overlooked:

Unbilled fees earned at August 31, $31,900.

Depreciation of equipment for August, $7,500.

Accrued wages at August 31, $5,200.

Supplies used during August, $3,000.

Instructions

1. journalize the entries to record the omitted adjustments.

2. Determine the correct amount of net income for August and the total assets, liabilities, and stockholders’ equity at August 31. In addition to indicating the corrected amounts, indicate the effect of each omitted adjustment by setting up and completing a columnar table similar to the following. The first adjustment is presented as an example.

Definition Definition Financial statement that provides a snapshot of an organization's financial position at a specific point in time. It summarizes a company's assets, liabilities, and shareholder's equity, detailing what the company owns, what it owes, and what is left over for its owners. The balance sheet serves as a crucial tool to assess the financial health and stability of a company, as well as to help management make informed decisions about its future investments and financial obligations.

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning