Concept explainers

Videos

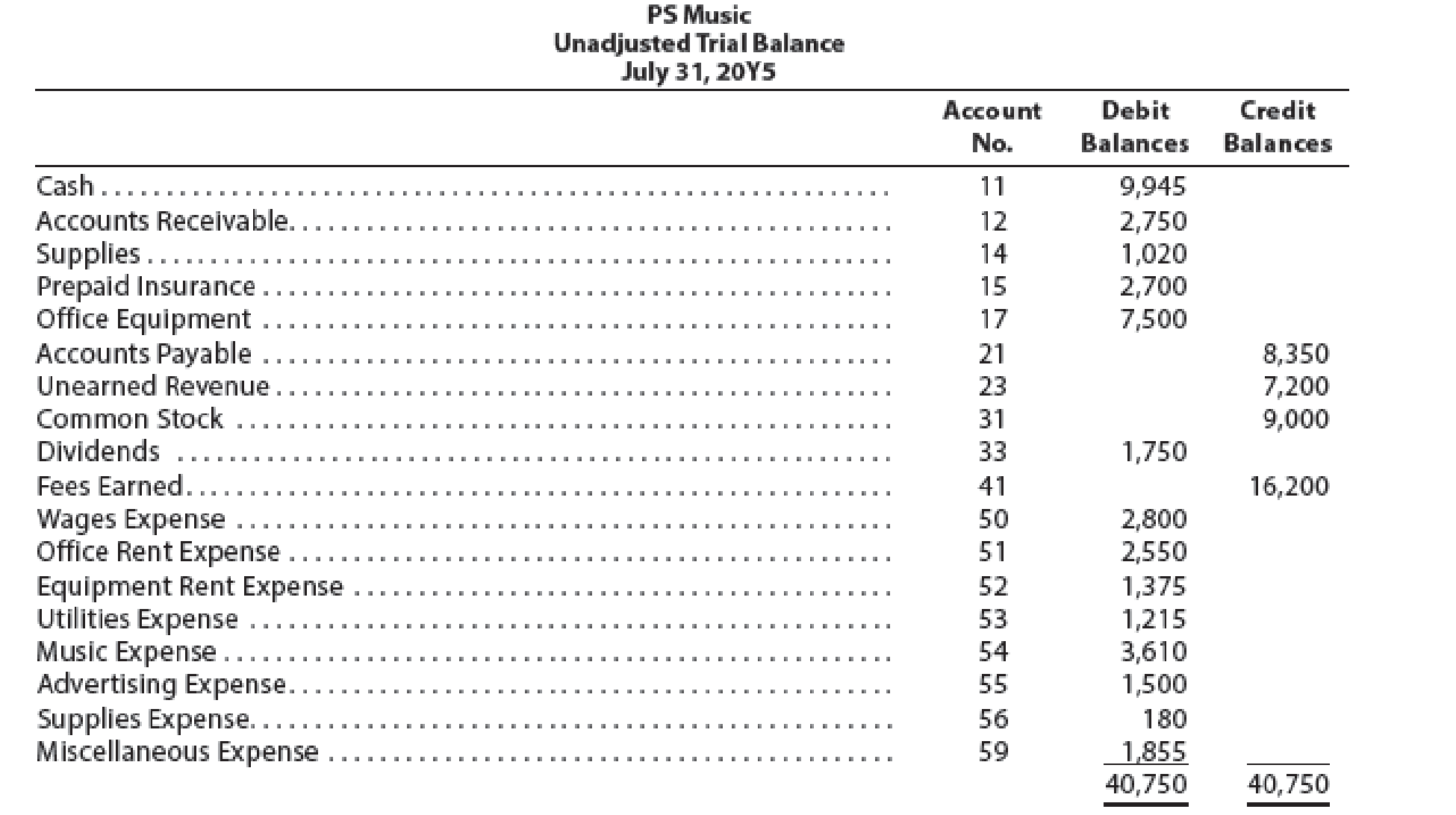

The unadjusted

The data needed to determine adjustments are as follows:

- During July, PS Music provided guest disc jockeys for KXMD for a total of 115 hours. For information on the amount of the accrued revenue to be billed to KXMD, see the contract described in the July 3 transaction at the end of Chapter 2.

- Supplies on hand at July 31, $275.

- The balance of the prepaid insurance account relates to the July 1 transaction at the end of

- Chapter 2.

Depreciation of the office equipment is $50.- The balance of the unearned revenue account relates to the contract between PS Music and KXMD, described in the July 3 transaction at the end of Chapter 2.

- Accrued wages as of July 31 were $140.

Instructions

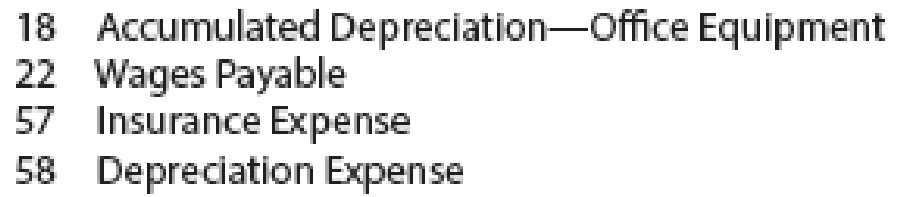

- 1. Prepare adjusting

journal entries. You will need the following additional accounts:

- 2.

Post the adjusting entries , inserting balances in the accounts affected. - 3. Prepare an adjusted trial balance.

1.

Prepare the adjusting entries in the books of Company PS at the end of the July 31, 2019.

Explanation of Solution

Adjusting entries:

Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. All adjusting entries affect at least one income statement account (revenue or expense), and one balance sheet account (asset or liability).

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- • Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- • Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, expenses.

| Journal Page 18 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2019 | Accounts receivable | 12 | 1,400 | ||

| July | 31 | Fees earned (1) | 41 | 1,400 | |

| (To record the fees earned at the end of July) | |||||

| 31 | Supplies expense (2) | 56 | 745 | ||

| Supplies | 14 | 745 | |||

| (To record supplies expense incurred at the end of the July) | |||||

| 31 | Insurance expense (3) | 57 | 225 | ||

| Prepaid insurance | 15 | 225 | |||

| (To record insurance expense incurred at the end of the July) | |||||

| 31 | Depreciation expense | 58 | 50 | ||

| Accumulated depreciation-Office equipment | 18 | 50 | |||

| (To record depreciation expense incurred at the end of the July) | |||||

| 31 | Unearned revenue (4) | 23 | 3,600 | ||

| Fees earned | 41 | 3,600 | |||

| (To record the service performed to the customer at the end of the July) | |||||

| 31 | Wages expense | 50 | 140 | ||

| Wages payable | 22 | 140 | |||

| (To record wages expense incurred at the end of the July) | |||||

Table (1)

Working notes:

1. Calculated the value of accrued fees during the July

Hence, fees earned during the July are $1,400.

2. Calculate the value of supplies expense

Hence, supplies expense during the July is $745.

3. Calculate the value of insurance expense

Hence, insurance expense during the July is $745.

4. Calculate the value of unearned fees at the end of the July

Hence, unearned fees at the end of the July are $3,600.

2.

Post the adjusting entries to the ledger in the books of Company PS.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholder’s equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- (a) The title of the account

- (b) The left or debit side

- (c) The right or credit side

Post the adjusting entries to the ledger account as follows:

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 3,920 | |||

| 1 | 1 | 5,000 | 8,920 | ||||

| 1 | 1 | 1,750 | 7,170 | ||||

| 1 | 1 | 2,700 | 4,470 | ||||

| 2 | 1 | 1,000 | 5,470 | ||||

| 3 | 1 | 7,200 | 12,670 | ||||

| 3 | 1 | 250 | 12,420 | ||||

| 4 | 1 | 900 | 11,520 | ||||

| 8 | 1 | 200 | 11,320 | ||||

| 11 | 1 | 1,000 | 12,320 | ||||

| 13 | 1 | 700 | 11,620 | ||||

| 14 | 1 | 1,200 | 10,420 | ||||

| 16 | 2 | 2,000 | 12,420 | ||||

| 21 | 2 | 620 | 11,800 | ||||

| 22 | 2 | 800 | 11,000 | ||||

| 23 | 2 | 750 | 11,750 | ||||

| 27 | 2 | 915 | 10,835 | ||||

| 28 | 2 | 1,200 | 9,635 | ||||

| 29 | 2 | 540 | 9,095 | ||||

| 30 | 2 | 500 | 9,595 | ||||

| 31 | 2 | 3,000 | 12,595 | ||||

| 31 | 2 | 1,400 | 11,195 | ||||

| 31 | 2 | 1,250 | 9,945 | ||||

Table (2)

| Account: Accounts Receivable Account no. 12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 1,000 | |||

| 2 | 1 | 1,000 | |||||

| 23 | 2 | 1,750 | 1,750 | ||||

| 30 | 2 | 1,000 | 2,750 | ||||

| 31 | Adjusting | 3 | 1,400 | 4,150 | |||

Table (3)

| Account: Supplies Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 170 | |||

| 18 | 850 | 1,020 | |||||

| 31 | Adjusting | 745 | 275 | ||||

Table (4)

| Account: Prepaid Insurance Account no. 15 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | 1 | 2,700 | 2,700 | |||

| 31 | Adjusting | 3 | 225 | 2,475 | |||

Table (5)

| Account: Office equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 5 | 1 | 7,500 | 7,500 | |||

Table (6)

| Account: Accumulated Depreciation Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 31 | Adjusting | 3 | 50 | 50 | ||

Table (7)

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 250 | |||

| 3 | 1 | 250 | |||||

| 5 | 1 | 7,500 | 7,500 | ||||

| 18 | 2 | 850 | 8,350 | ||||

Table (8)

| Account: Wages Payable Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 31 | Adjusting | 3 | 140 | 140 | ||

Table (9)

| Account: Unearned revenue Account no. 23 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | 1 | 7,200 | 7,200 | |||

| 31 | Adjusting | 3 | 3,600 | 3,600 | |||

Table (10)

| Account: P’s capital Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 4,000 | |||

| 1 | 1 | 5,000 | 9,000 | ||||

Table (11)

| Account: P’s drawings Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 500 | |||

| 31 | 2 | 1,250 | 1,750 | ||||

Table (12)

| Account: Fees earned Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 6,200 | |||

| 11 | 1 | 1,000 | 7,200 | ||||

| 16 | 2 | 2,000 | 9,200 | ||||

| 23 | 2 | 2,500 | 11,700 | ||||

| 30 | 2 | 1,500 | 13,200 | ||||

| 31 | 2 | 3,000 | 16,200 | ||||

| 31 | Adjusting | 3 | 1,400 | 17,600 | |||

| 31 | Adjusting | 3 | 3,600 | 21,200 | |||

Table (13)

| Account: Wages expense Account no. 50 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 400 | |||

| 14 | 1 | 1,200 | 1,600 | ||||

| 28 | 2 | 1,200 | 2,800 | ||||

| 31 | Adjusting | 3 | 140 | 2,940 | |||

Table (14)

| Account: Office rent expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 800 | |||

| 1 | 1 | 1,750 | 2,550 | ||||

Table (15)

| Account: Equipment rent expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 675 | |||

| 13 | 1 | 700 | 1,375 | ||||

Table (16)

| Account: Utilities expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 300 | |||

| 27 | 2 | 915 | 1,215 | ||||

Table (17)

| Account: Music expense Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 1,590 | |||

| 21 | 2 | 620 | 2,210 | ||||

| 31 | 2 | 1,400 | 3,610 | ||||

Table (18)

| Account: Advertising expense Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 500 | |||

| 8 | 1 | 200 | 700 | ||||

| 22 | 2 | 800 | 1,500 | ||||

Table (19)

| Account: Supplies expense Account no. 56 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 180 | |||

| 31 | Adjusting | 3 | 745 | 925 | |||

Table (20)

| Account: Insurance expense Account no. 57 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 31 | Adjusting | 3 | 225 | 225 | ||

Table (21)

| Account: Depreciation expense Account no. 58 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 31 | Adjusting | 3 | 50 | 50 | ||

Table (22)

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| July | 1 | Balance | ✓ | 415 | |||

| 4 | 900 | 1,315 | |||||

| 29 | 540 | 1,855 | |||||

Table (23)

3.

Prepare an adjusted trial balance of Company PS at July 31, 2019.

Explanation of Solution

Adjusted trial balance:

Adjusted trial balance is a summary of all the ledger accounts, and it contains the balances of all the accounts after the adjustment entries are journalized, and posted.

Prepare an adjusted trial balance of Company PS at July 31, 2019 as follows:

| Company PS | |||

| Adjusted Trial Balance | |||

| July 31, 2019 | |||

| Particulars | AccountNo. | Debit $ | Credit $ |

| Cash | 11 | 9,945 | |

| Accounts receivable | 12 | 4,150 | |

| Supplies | 14 | 275 | |

| Prepaid insurance | 15 | 2,475 | |

| Office equipment | 17 | 7,500 | |

| Accumulated depreciation-Equipment | 18 | 50 | |

| Accounts payable | 21 | 8,350 | |

| Wages payable | 22 | 140 | |

| Unearned revenue | 23 | 3,600 | |

| P's capital | 31 | 9,000 | |

| P's drawings | 32 | 1750 | |

| Fees earned | 41 | 21,200 | |

| Wages expense | 50 | 2,940 | |

| Office rent expense | 51 | 2,550 | |

| Equipment rent expense | 52 | 1,375 | |

| Utilities expense | 53 | 1,215 | |

| Music expense | 54 | 3,610 | |

| Advertising expense | 55 | 1,500 | |

| Supplies expense | 56 | 925 | |

| Insurance expense | 57 | 225 | |

| Depreciation expense | 58 | 50 | |

| Miscellaneous expense | 59 | 1,855 | |

| 42,340 | 42,340 | ||

Table (24)

The debit column and credit column of the adjusted trial balance are agreed, both having the balance of $42,340.

Want to see more full solutions like this?

Chapter 3 Solutions

Financial and Managerial Accounting - CengageNow

- On October 1, Goodwell Company rented warehouse space to a tenant for $1,600 per month and received $8,000 for five months' rent in advance on that date, with the lease beginning immediately. The cash receipt was credited to the Unearned Revenue account. The company's annual accounting period ends on December 31. The Unearned Revenue account balance at the end of December, after adjustment, should be: Multiple Choice $3,200. $1,600. $8,000. $6,400. $4,800.arrow_forwardOn October 1, Vista View Company rented warehouse space to a tenant for $2,100 per month and received $10,500 for five months' rent in advance on that date, with the lease beginning immediately. The cash receipt was credited to the Unearned Rent account. The company's annual accounting period ends on December 31. The Unearned Rent account balance at the end of December, after adjustment, should be: Multiple Choice $10,500. $6,300. $2,100. $8,400. $4,200. < Prev 20 of 30 Next MacBook Airarrow_forwardThe unadjusted trial balance that you prepared for PS Music at the end of Chapter 2 should appear as follows: The data needed to determine adjustments are as follows: a. During July, PS Music provided guest disc jockeys for KXMD for a total of 115 hours. For information on the amount of the accrued revenue to be billed to KXMD, see the contract described in the July 3, 2016, transaction at the end of Chapter 2. b. Supplies on hand at July 31, 275. c. The balance of the prepaid insurance account relates to the July 1, 2016, transaction at the end of Chapter 2. d. Depreciation of the office equipment is 50. e. The balance of the unearned revenue account relates to the contract between PS Music and KXMD, described in the July 3, 2016, transaction at the end of Chapter 2. f. Accrued wages as of July 31, 2016, were 140. Instructions 1. Prepare adjusting journal entries. You will need the following additional accounts: 18 Accumulated DepreciationOffice Equipment 22 Wages Payable 57 Insurance Expense 58 Depreciation Expense 2.Post the adjusting entries, inserting balances in the accounts affected. 3.Prepare an adjusted trial balance.arrow_forward

- Suppose a customer rents a vehicle for three months from Franklin Rental on November 1, paying $3,750 ($1,250/month). Required: 1.&2. Record the necessary entries in the Journal Entry Worksheet below. 3. Calculate the year-end adjusted balances of Deferred Revenue and Service Revenue (assuming the balance of Deferred Revenue at the beginning of the year is $0).arrow_forwardAccounting Questionarrow_forwardCalco Inc. rents its store location. Rent is $950 per month, payable quarterly in advance. On July 1, a check for $2,850 was issued to the landlord for the July–September quarter.Required: Prepare the Horizontal model and Journal entry for each of the following transactions. To record the payment on July 1, assuming that all $2,850 is initially recorded as Rent Expense. To record the adjustment that would be appropriate at July 31 if your entry in a had been made. To record the payment on July 1, assuming instead that all $2,850 is initially recorded as Prepaid Rent. To record the adjustment that would be appropriate at July 31 if your entry in c had been made. To record the adjustment that would be appropriate at August 31 and September 30, regardless of how the payment on July 1 had been initially recorded (and assuming that the July 31 adjustment had been made). Indicate the financial statement effect. If you were supervising the bookkeeper, how would you suggest that the July…arrow_forward

- Assuming a year-end in March 31,it is now April 4.A staff member asks you to process an unpaid invoice with details as follows: The invoice is for bus transportation in the amount of P800 and is dated April. The invoice indicates the charges relate to transportation on March 20.A transfer is processed to pay the invoice on April 7. Hiw would you proceed? You may describe how you would record the transaction in the general ledger, including a description of journal entries and the dates each item will be recordedarrow_forwardThe unadjusted trial balance that you prepared for PS Music at the end of Chapter 2 should appear as follows: PS Music Unadjusted Trial Balance July 31, 2018 The data needed to determine adjustments are as follows: During July, PS Music provided guest disc jockeys for KXMD for a total of 115 hours. For information on the amount of the accrued revenue to be billed to KXMD, see the contract described in the July 3 transaction at the end of Chapter 2. Supplies on hand at July 31, 275. The balance of the prepaid insurance account relates to the July 1 transaction at the end of Chapter 2. Depreciation of the office equipment is 50. The balance of the unearned revenue account relates to the contract between PS Music and KXMD, described in the July 3 transaction at the end of Chapter 2. Accrued wages as of July 31 were 140. Instructions 1. Prepare adjusting journal entries. You will need the following additional accounts: 18 Accumulated DepreciationOffice Equipment 22 Wages Payable 57 Insurance Expense 58 Depreciation Expense 2. Post the adjusting entries, inserting balances in the accounts affected. 3. Prepare an adjusted trial balance.arrow_forwardOn December 1 Simpson marketing company received $6900 from a customer for a two month marketing plan to be completed January 31 of the following year. The cash receipt was recorded as unearned fees the adjustment entry for the year and then December 31 would include:arrow_forward

- Question involving Revenue Recognition: How much revenue should be recognized by the following Company, in each of the month's of March, April, May, June, July, August, and September? A company pre-sells services to be performed from May through September, inclusive. If payment is made in full by April 1, a 4% discount is allowed. In March, 245 customers took advantage of the discount and purchased the services for $650 each. In June, 220 customers purchased the services for $785, and in July, 95 purchased it for the same price. For the customers who pay after May 1, services start in the month the customer makes the payment. Please explain for each month. Months $ March April May June July August Septemberarrow_forwardTopic: REVENUE FROM CONTRACTS WITH CUSTOMERS Requirement: Provide the entries during the first 90 days of the contract (assume that the product was not returned)arrow_forwardABC Ltd received $15,000 on the 1st of July 2015 from one of its customers for services expected to be completed by December 31 on the equal monthly paces. If 45% of the requested services performed by the end of September, how would ABC record this revenue? Select one: Dr Service Revenue - $7,500 Cr Unearned Service Revenue - $7,500 Dr Service Revenue - $6,750 Cr Unearned Service Revenue - $6,750 Dr Unearned Service Revenue - $6,750 Cr Service Revenue - $6,750 Dr Unearned Service Revenue - $7,500 Cr Service Revenue - $7,500arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning