Videos

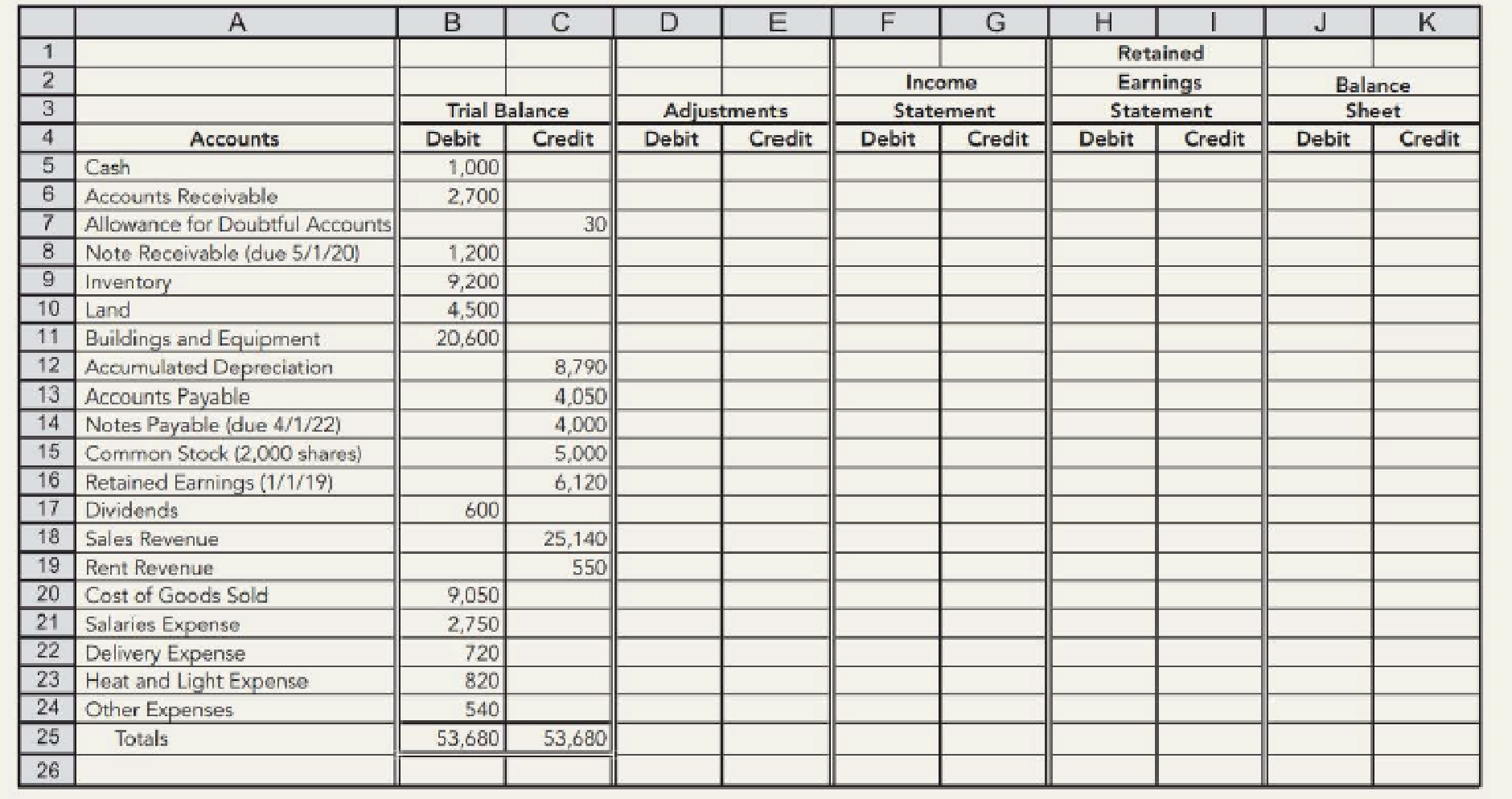

Worksheet Devlin Company has prepared the following partially completed worksheet for the year ended December 31, 2019:

The following additional information is available: (a) salaries accrued but unpaid total $250; (b) the $80 heat and light bill for December has not been recorded or paid; (c) depreciation expense totals $810 on the buildings and equipment; (d) interest accrued on the note payable totals $380 (this will be paid when the note is repaid); (e) the company leases a portion of its floor space to KT & Daniel Specialty Company for $50 per month, and KT & Daniel has not yet paid its December rent; (f) interest accrued on the note receivable totals $80; (g)

Required:

- 1. Complete the worksheet. (Round to the nearest dollar.)

- 2. Prepare the company’s financial statements.

- 3. Prepare (a) adjusting and (b) closing entries in the general journal.

Trending nowThis is a popular solution!

Chapter 3 Solutions

Intermediate Accounting: Reporting and Analysis (Looseleaf)

- Prepare journal entries to record the following transactions. You are required to show all calculations: the financial year-end of the client is 30 November 2021. 3.1 The company adopted the straight-line depreciation method. Record the 15% depreciation on the plant and equipment purchased On 1 December 2020 for R125 000. 3.2 The allowance for credit losses account has an opening balance of R4 500. The policy requires the allowance to equate 8% of the total accounts receivable. The debtors sub-ledger totaled R52 000 prior receiving 40c in the rand on an account of R3 000. The financial manager instructed the write off on the balance WITH GENERAL LEDGER ENTERIES: Please dont provide answer in image format thnkuarrow_forwardThe notes payable are dated June 30, 2023, and are due on June 30, 2025. Interest at 5% is payable annually on June 30. Depreciation on the furniture and fixtures for 2024 is $29,000. The furniture and fixtures originally cost $390,000. Required: Prepare a classified balance sheet at December 31, 2024, by updating ending balances from 2023 for transactions during 2024 and the additional information. The cost of furniture and fixtures and their accumulated depreciation are shown separately. Note: Amounts to be deducted should be indicated by a minus sign. Current assets: Cash Accounts receivable Inventory Total current assets Property, plant, and equipment: Furniture and fixtures Accumulated depreciation Net property, plant, and equipment Total assets Current liabilities: Accounts payable Interest payable Notes payable KORVER SUPPLY COMPANY Balance Sheet At December 31, 2024 Assets Total current liabilities Shareholders' equity: Common stock Retained earnings Liabilities and…arrow_forwardKoolman Construction Company began work on a contract in 2019. The contract price is 3,000,000, and the company determined that its performance obligation was satisfied over time. Other information relating to the contract is as follows: Required: 1. Compute the gross profit or loss recognized in 2019 and 2020. 2. Prepare the appropriate sections of the income statement and ending balance sheet for each year.arrow_forward

- The following are independent errors: a. In January 2019, repair costs of 9,000 were debited to the Machinery account. At the beginning of 2019, the book value of the machinery was 100,000. No residual value is expected, the remaining estimated life is 10 years, and straight-line depreciation is used. b. All purchases of materials for construction contracts still in progress have been immediately expensed. It is discovered that the use of these materials was 10,000 during 2018 and 12,000 during 2019. c. Depreciation on manufacturing equipment has been excluded from manufacturing costs and treated as a period expense. During 2019, 40,000 of depreciation was accounted for in that manner. Production was 15,000 units during 2019, of which 3,000 remained in inventory at the end of the year. Assume there was no inventory at the beginning of 2019. Required: Prepare journal entries for the preceding errors discovered during 2020. Ignore income taxes.arrow_forwardDuring 2019, Ryel Companys controller asked you to prepare correcting journal entries for the following three situations: 1. Machine A was purchased for 50,000 on January 1, 2014. Straight-line depreciation has been recorded for 5 years, and the Accumulated Depreciation account has a balance of 25,000. The estimated residual value remains at 5,000, but the service life is now estimated to be 1 year longer than estimated originally. 2. Machine B was purchased for 40,000 on January 1, 2017. It had an estimated residual value of 5,000 and an estimated service life of 10 years. it has been depreciated under the double-declining-balance method for 2 years. Now, at the beginning of the third year, Ryel has decided to change to the straight-line method. 3. Machine C was purchased for 20,000 on January 1, 2018, Double-declining-balance depreciation has been recorded for 1 year. The estimated residual value of the machine is 2,000 and the estimated service life is 5 years. The computation of the depreciation erroneously included the estimated residual value. Required: Prepare any necessary correcting journal entries for each situation. Also prepare the journal entry necessary for each situation to record depreciation expense for 2019.arrow_forwardThe Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Depreciation is computed from the first of the month of acquisition to the first of the month of disposition. Land A and Building A were acquired from a predecessor corporation. Thompson paid $792,500 for the land and building together. At the time of acquisition, the land had a fair value of $70,400 and the building had a fair value of $809,600. Land B was acquired on October 2, 2019, in exchange for 2,800 newly issued shares of…arrow_forward

- Cadillac Construction Company uses the retirement method to determine depreciation on its small tools. During 2019, the first year of the company’s operations, tools were purchased at a cost of $11,500. In 2021, tools originally costing $4,400 were sold for $850 and replaced with new tools costing $5,000. Required:1. Prepare journal entries to record each of the above transactions.2. Prepare journal entries to record each of the above transactions, assuming that the company uses the replacement depreciation method instead of the retirement method.arrow_forwardThe following selected transactions relate to liabilities of Interstate Farm Implements for December 2018. Interstate’s fiscal year ends on December 31.Required:Prepare the appropriate journal entries for these transactions.1. On December 15, received $7,500 from Bradley Farms toward the purchase of a $98,000 tractor to be delivered on January 6, 2019.2. During December, received $25,500 of refundable deposits relating to containers used to transport equipment parts.3. During December, credit sales totaled $800,000. The state sales tax rate is 5% and the local sales tax rate is2%. (This is a summary journal entry for the many individual sales transactions for the period).arrow_forwardGunkelson Company sells equipment on September 30, 2019, for $18,000 cash. The equipment originally cost $72,000 and as of January 1, 2019, had accumulated depreciation of $42,000. Depreciation for the first 9 months of 2019 is $5,250.Prepare the journal entries to (a) update depreciation to September 30, 2019, and (b) record the sale of the equipment. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.)arrow_forward

- Cadillac Construction Company uses the retirement method to determine depreciation on its small tools. During 2019, the first year of the company’s operations, tools were purchased at a cost of $8,000. In 2021, tools originally costing $2,000 were sold for $250 and replaced with new tools costing $2,500.Required:1. Prepare journal entries to record each of the above transactions.2. Repeat requirement 1 assuming that the company uses the replacement depreciation method instead of the retirement method.arrow_forwardRahman Company, a manufacturer of steel products, began operations on January 1, 2020. Rahman has a December 31 fiscal year-end and adjusts its accounts annually. Selected transactions related to its Brampton plant are as follows: Jan. 1, 2020 Paid cash for six (6) stamping machines for a total price of $15,300 plus delivery costs of $200 per unit Dec. 31, 2020 Recorded depreciation at year end. Assume that the stamping machines have a 5 year useful life and a residual (salvage) value of 10% of the original cost. Dec. 31, 2021 Recorded depreciation at year end. Jan. 1, 2022 One (1) stamping machine was sold for $1,250. . Dec. 31, 2022 Exchanged one (1) stamping machine for a welding machine. The list price of the welding machine was $8,000 and Rahman received a trade-in allowance for the stamping machine of $2,000 (remainder paid in cash). A new welding machine could be bought (without a trade-in) for $7,500. The fair market value of the stamping machine was $1,000.…arrow_forwardOn January 1, 2020, Miller Construction Company contracted to build a parking lot for the city of St. Louis for $525,000. The following transactions and estimates relate to this contract. Construction costs incurred during 2020 $280,000 $133,000 $122,500 Estimated costs to complete $280,000 a. Prepare the 2020 journal entry to record profit or loss assuming revenue is recognized over time. Note: Record any multiple debits in alphabetical order and any multiple credits in alphabetical order. Progress billings Cash collections a. Account To recognize revenues and expenses b. ♦ ◆ b. Prepare the 2020 journal entry to record profit or loss assuming revenue is recognized at a point in time. Account Debit Note: If a journal entry (or a line of the journal entry) isn't required for the transaction, select "N/A" as the account names and leave the Dr. and Cr. answers blank (zero). To recognize revenues and expenses Credit Debit Creditarrow_forward

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT