Videos

The current price of Estelle Corporation stock is $25. In each of the next two years, this stock price will either go up by 20% or go down by 20%. The stock pays no dividends. The one-year risk-free interest rate is 6% and will remain constant. Using the Binomial Model, calculate the price of a one-year call option on Estelle stock with a strike price of $25.

To determine: The price of a one year call option on ET stock.

Introduction: A binomial model portrays the development of irregular variables over a progression of time steps, relegating specified probabilities to increase or decrease in the variable. The binomial option pricing model makes the improving supposition that, toward the finish of every period, the price of stocks has just two conceivable values.

Answer to Problem 1P

Explanation of Solution

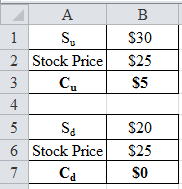

Determine the increase or decrease in the stock price.

Therefore, the stock price either increases to $30 or decreases to $20

Here

S – Denotes the current stock price

K – Denotes the strike price

C – Denotes the call price

B – Denotes the risk-free investment or initial investment in the portfolio

Su – Denotes the probability of increase in stock price (the price to go up)

Sd – Denotes the probability of decrease in stock price next period (the price to go down)

rf – Denotes the risk-free rate

Cu – Denotes the price of the call option if the stock price increases (the price to go up)

Cd – Denotes the price of the call option if the stock price decreases (the price to go down)

Δ – Denotes the shares of stock in the portfolio or the sensitivity of option price to stock price

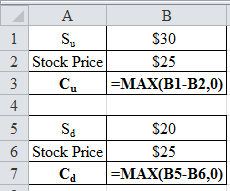

Determine the option payoff:

Using Excel function =MAX, the option payoff is determined as follows:

Excel spreadsheet:

Excel workings:

Therefore, the option payoff either increases to $5 or decreases to $0.

Determine the shares of stock in the replicating portfolio:

Therefore, the share of stock in the replicating portfolio is 0.5.

Determine the risk-free investment or initial investment in the portfolio:

Therefore, the risk-free investment or initial investment in the portfolio is -9.4340.

Determine the price of a one year call option on ET stock:

Therefore, the price of a one year call option on ET stock is $3.07.

Want to see more full solutions like this?

Chapter 21 Solutions

EBK CORPORATE FINANCE

Additional Business Textbook Solutions

Financial Accounting: Tools for Business Decision Making, 8th Edition

Engineering Economy (17th Edition)

Gitman: Principl Manageri Finance_15 (15th Edition) (What's New in Finance)

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

Horngren's Financial & Managerial Accounting, The Financial Chapters (Book & Access Card)

Horngren's Accounting (12th Edition)

- Don't used Ai solutionarrow_forwardllumina Inc. is expected to pay its next dividend of $0.4 two years from now. This dividend should then grow at a rate of 10% for 3 years (till the end of year 5), and at a reduced rate of 6% thereafter. The market required rate of return is 16%. The price of the company's shares today is: $4.15 $4.39 $3.79 $3.96arrow_forwardA bank has made a loan charging a base lending rate of 8%. It expects a probability of default of 5%. If the loan is defaulted, it expects to recover 50% of its money through the sale of its collateral. The expected return on this loan is _____% (rounded to two decimal places).arrow_forward

- Ch 26: Assignment - Mergers and Corporate Control Widget Corp., which is considering the acquisition of Exteter Enterprise Inc., estimates that acquiring Exteter will result in an incremental value for the firm. The analysts involved in the deal have collected the following information from the projected financial statements of the target company: Data Collected (in millions of dollars) Year 1 Year 2 Year 3 EBIT $13.0 $15.6 $19.5 Interest expense 5.0 5.5 6.0 Debt 35.2 41.6 44.8 Total net operating capital 107.1 109.2 111.3 Exteter Enterprise Inc. is a publicly traded company, and its market-determined pre-merger beta is 1.00. You also have the following information about the company and the projected statements: •Exteter currently has a $38.00 million market value of equity and $24.70 million in debt. The risk-free rate is 3.5%, there is a 5.60% market risk premium, and the Capital Asset Pricing Model produces a pre-merger required rate of return on equity ISL of 9.10%. •Exteter's cost…arrow_forward3. Problem 30-03 (Plan Funding) Plan Funding eBook Consolidated Industries is planning to operate for 10 more years and then cease operations. At that time (in 10 years), it expects to have the following pension benefit obligations: Year 11-15 16-20 21-25 Annual Total Payment $3,480,000 2,980,000 26-30 31-35 2,480,000 1,980,000 1,480,000 The current value of the firm's pension fund is $5.6 million. Assume that all cash flows occur at year-end. a. Consolidated's expected return on pension assets is 11%, and it uses 11% to discount the expected pension benefit payments. What is the present value of the firm's pension fund benefits? Do not round intermediate calculations. Round your answer to the nearest dollar. $ b. Is the plan underfunded or overfunded? Do not round intermediate calculations. Round your answer to two decimal places. Funding ratio= which means the assets are select than the PV of benefits and the plan is select Less or greater Select underfunded overfundedarrow_forwardPlan Funding Consolidated Industries is planning to operate for 10 more years and then cease operations. At that time (in 10 years), it expects to have the following pension benefit obligations: Year 11-15 16-20 21-25 Annual Total Payment $3,500,000 3,000,000 2,500,000 26-30 31-35 2,000,000 1,500,000 The current value of the firm's pension fund is $6.1 million. Assume that all cash flows occur at year-end. a. Consolidated's expected return on pension assets is 12%, and it uses 12% to discount the expected pension benefit payments. What is the present value of the firm's pension fund benefits? Do not round intermediate calculations. Round your answer to the nearest dollar. $ b. Is the plan underfunded or overfunded? Do not round intermediate calculations. Round your answer to two decimal places. Funding ratio = which means the assets are -Select- than the PV of benefits and the plan is -Select- ☑. Less or Greater Overfunded or Underfundedarrow_forward

- Benefits and Contributions The Certainty Company (CC) operates in a world of certainty. It has just hired Mr. Jones, age 27, who will retire at age 65, draw retirement benefits for 14 years, and die at age 79. Mr. Jones' salary is $21,000 per year, but wages are expected to increase at the 6% annual rate of inflation. CC has a defined benefit plan in which workers receive 1% of the final year's wage for each year employed. The retirement benefit, once started, does not have a cost-of-living adjustment. CC earns 12% annually on its pension fund assets and uses a 10% rate to discount its expected future benefit payments. Assume that pension contribution and benefit cash flows occur at year-end. Do not round intermediate calculations. Round your answers to the nearest dollar. a. How much will Mr. Jones receive in annual retirement benefits? $ b. What is CC's required annual contribution to fully fund Mr. Jones' retirement benefits? $ c. Assume now that CC hires Mr. Smith at the same…arrow_forwardlab.infoseclearning.com/console/5061763/3047 310-win10 Project Three Milestone - GNS3 File Edit View Control Node Annotate Tools Help e 41 Sales_PC1 0000 Sales_PC2 Sales_PC3 Enforce US Keyboard Layout View Fullscreen Send Ctrl+Alt+Delete Reboot To exit full screen, press and hold esc ■C00/6@ Q Sales_Switch Human Resources_Switch Office_Router Sales PC4 Customer_Service_Switch X: -299.0 Y: -136.0 Z: 1.0 H Type here to search CS_FTP_Server HR_PC2 HR_PC1 7:19 PM 12/14/2024 Barrow_forwardAGG is a US multinational that manufactures specialist high tech parts in the airline engine industry. AGG is an established company with steady growth in turnover and dividends over the last 10 years. The company is undertaking a projected titled Project Big as a strategic response to the changing market scene. AGG will develop a new state of the art highly automated plant located in Cambodia which is expected to result in cost advantages if it is implemented. The details about the project are below • Initital investment has been estimated at $500m • • The annual pre tax savings in operating costs at current exchange rates has been calculated at $150m for the first four years (starting in the first year) The residual value of the project at the end of the four years is estimated to be $250m The initial investment, net of residual value, qualifies for capital allowance and can be claimed back on a straight line basis over the four years of the project. Current AGG's cost of capital is…arrow_forward

- You have just won the Strayer Lottery jackpot of $11,000,000. You will be paid in twenty-six equal annual installments beginning immediately. If you had the money now, you could invest it in an account with a quoted annual interest rate of 9% with monthly compounding of interest. Calculate the present value of the payments you will receive. Show your calculations using formulas in your paper or provide how to do the calculations in Excel. Explain why there is a difference between the present value of the Strayer lottery jackpot and the future value of the twenty-six annual payments based on your calculations and the information provided.arrow_forwardYou have just won the Strayer Lottery jackpot of $11,000,000. You will be paid in twenty-six equal annual installments beginning immediately. If you had the money now, you could invest it in an account with a quoted annual interest rate of 9% with monthly compounding of interest. Calculate the present value of the payments you will receive. Show your calculations using formulas in your paper or in an attached spreadsheet file.arrow_forwardThe approach uses a weighted average cost of capital that is unique to a particular project while determining the appropriate discount rate.arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT