Concept explainers

Videos

Using transactions from the following assignments, record

Based on Serial Problem SP 2

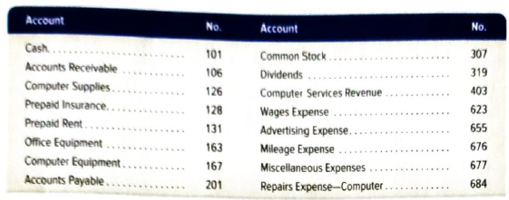

On October 1, 2018, Santana Rey launched a computer services company called Business Solutions, which provides consulting services, computer system installations, and custom program development. Rey adopts the calendar year for reporting purposes and expects to prepare the company’s first set of financial statements on December 31, 2018. The company’s initial chart of accounts follows.

Required

- Prepare journal entries to record each of the following transactions for Business Solutions.

| Oct. |

1.

Introduction: Journal entry is a technique of booking and recording financial transactions on any company. Ledger is used to record all economic transactions of the account by account type, with debits and credits in separate columns and a beginning monetary balance and ending monetary balance for each account.

To prepare: The general journal entries for the following transaction.

Explanation of Solution

Journal entries of KT for the month of April are shown below.

| Date | Particular | PR | Dr. | Cr. |

| Oct 1 | Cash | 20,000 | ||

| Office equipment | 45,000 | |||

| Computer equipment | 8,000 | |||

| To Common stock | 73,000 | |||

| (Owner’s investment) | ||||

| 2 Oct | Prepaid rent | 3,300 | ||

| cash | 3,300 | |||

| (rent paid in advance) | ||||

| 3 Oct | Computer supplies | 1,420 | ||

| Account payable company H | 1,420 | |||

| (purchase of supplies on credit from company H) | ||||

| 5 Oct | Prepaid insurance | 2,220 | ||

| Cash | 2,220 | |||

| (payment of insurance) | ||||

| 6 Oct | Account receivable company E | 4,800 | ||

| Service revenue | 4,800 | |||

| (service provided on credit) | ||||

| 8 Oct | Account payable company H | 1,420 | ||

| Cash | 1,420 | |||

| (cash to company H) | ||||

| 12 Oct | Account receivable company E | 1,400 | ||

| Service revenue | 1,400 | |||

| (service provided on credit) | ||||

| 15 Oct | Cash | 4,800 | ||

| Account receivable company E | 4,800 | |||

| (cash received from company E) | ||||

| 17 Oct | Repair computer equipment | 805 | ||

| Cash | 805 | |||

| (cash paid for repair of computer equipment) | ||||

| 20 Oct | Advertisement | 1,728 | ||

| Cash | 1,728 | |||

| (cash paid for advertisement ) | ||||

| 22 Oct | Cash | 1,400 | ||

| Account receivable company E | 1,400 | |||

| (cash received from company E) | ||||

| 28 Oct | Account receivable | 5,208 | ||

| Service revenue | 5,208 | |||

| 31 Oct | Wages expense | 875 | ||

| Cash | 875 | |||

| (Cash paid for wages) | ||||

| 31 Oct | Dividend cash | 3600 | ||

| (dividend paid in cash) | 3600 | |||

| 1 Nov | Miscellaneous expense | 320 | ||

| Cash | 320 | |||

| (cash paid for miscellaneous expense) | ||||

| 2 Nov | Cash | 4,633 | ||

| Service revenue | 4,633 | |||

| (cash received for provided revenue) | ||||

| 5 Nov | Computer supplies | 1,125 | ||

| Cash | 1125 | |||

| (purchase of computer supplies on cash) | ||||

| 8 Nov | Account receivable Company G | 5,668 | ||

| Service revenue | 5,668 | |||

| (service provided on credit) | ||||

| 18 Nov | Cash | 2,208 | ||

| Account receivable company I | 2,208 | |||

| (cash received from company I) | ||||

| 22 Nov | Donation | 250 | ||

| Cash | 250 | |||

| (cash given as donation) | ||||

| 24 Nov | Account receivable Company A | 3950 | ||

| Computer service revenue | 3950 | |||

| (to record service revenue) | ||||

| 28 Nov | Miscellaneous expense | 384 | ||

| Cash | 384 | |||

| (cash paid for miscellaneous expense) | ||||

| 30 Nov | Wages expense | 1750 | ||

| Cash | 1750 | |||

| (cash paid for wages) | ||||

| 30 Nov | Dividend | 2000 | ||

| Cash | 2000 | |||

| (Dividend paid) | ||||

2.

Introduction: Journal entry is a technique of booking and recording financial transactions on any company. Ledger is used to record all economic transactions of the account by account type, with debits and credits in separate columns and a beginning monetary balance and ending monetary balance for each account.

To prepare: T account for the following transactions.

Explanation of Solution

| Cash Account No.101 | ||||

| Date | PR | Debit | Credit | Balance |

| 1 Oct | 45000 | 45,000 | ||

| 2 Oct | 3300 | 41,700 | ||

| 3 Oct | 2220 | 39,480 | ||

| 5 Oct | 1420 | 38,060 | ||

| 6 Oct | 4800 | 42,860 | ||

| 8 Oct | 875 | 41,985 | ||

| 12 Oct | 805 | 41,180 | ||

| 15 Oct | 1728 | 39,452 | ||

| 17 Oct | 1400 | 40,850 | ||

| 20 Oct | 3600 | 37,252 | ||

| 22 Oct | 320 | 36,932 | ||

| 28 Oct | 4633 | 41,565 | ||

| 31 Oct | 1125 | 40,440 | ||

| 31 Oct | 2208 | 42,648 | ||

| 15 Nov | 250 | 42,398 | ||

| 1 Nov | 3841 | 42,014 | ||

| 2 Nov | 1750 | 40,264 | ||

| 30 Nov | 2000 | 38,264 | ||

| Accounts Receivable company E | Account no. 106 | |||

| Date | PR | Debit | Credit | Balance |

| 6 Oct | 4800 | 4800 | ||

| 12 Oct | 1400 | 6200 | ||

| 15 Oct | 4800 | 1400 | ||

| 22 Oct | 1400 | 0 |

| Account receivable company E | Account no.108 | |||

| Date | PR | Debit | Credit | Balance |

| 8 Oct | 5668 | 5668 | ||

| Account receivable company I | Account no. 108 | |||

| Date | PR | Debit | Credit | Balance |

| 6 Oct | 5208 | 5208 | ||

| 15 Oct | 2208 | 3000 | ||

| Account payable | Account no.201 | |||

| Date | PR | Debit | Credit | Balance |

| 6 Oct | 1420 | 1420 | ||

| 15 Oct | 1420 | 0 | ||

| Supplies | Account no. 126 | |||

| Date | PR | Debit | Credit | Balance |

| 3 Oct | 1420 | 1420 | ||

| 5 Nov | 1125 | 2545 | ||

| Equipment | Account no. 163 | |||

| Date | PR | Debit | Credit | Balance |

| 1 Oct | 8000 | 8000 | ||

| Prepaid insurance | Account no.128 | |||

| Date | PR | Debit | Credit | Balance |

| 2 oct | 2220 | 2220 |

| Prepaid rent | Account no. 131 | |||

| Date | PR | Debit | Credit | Balance |

| 1 oct | 3300 | 3300 |

| Computer supplies | Account no. 167 | |||

| Date | PR | Debit | Credit | Balance |

| 1 Oct | 20000 | 20000 |

| Common stock | Account no. 307 | |||

| Date | PR | Debit | Credit | Balance |

| 1 oct | 45000 | 45000 | ||

| 1 Oct | 20000 | 65000 | ||

| 1 Oct | 8000 | 73000 |

| Dividend | Account no. 319 | |||

| Date | PR | Debit | Credit | Balance |

| 31 oct | 2000 | 2000 | ||

| 31 oct | 3600 | 5600 |

| Computer Service revenue | Account no. 403 | |||

| Date | PR | Debit | Credit | Balance |

| 24 Nov | 3950 | 3950 | ||

| 6 Oct | 4800 | 8750 | ||

| 12 Oct | 1400 | 10150 | ||

| 28 Oct | 5208 | 15358 | ||

| 8 Nov | 5668 | 21026 |

3.

Introduction: Journal entry is a technique of booking and recording financial transactions on any company. Ledger is used to record all economic transactions of the account by account type, with debits and credits in separate columns and a beginning monetary balance and ending monetary balance for each account.

To prepare: Trail balance.

Answer to Problem 8GLP

Total of trail balance is $98,659

Explanation of Solution

| S Trail balance | ||

| Particular | Dr. | Cr. |

| Cash | 38,264 | |

| Account receivable | 12,618 | |

| Equipment | 8,000 | |

| Supplies | 2,545 | |

| Prepaid insurance | 2,220 | |

| Prepaid rent | 3,300 | |

| Account payable | 0 | |

| Wages expense | 2,625 | |

| Common stock | 73,000 | |

| Divided | 5,600 | |

| Service revenue | 21,709 | |

| Computer service revenue | 3950 | |

| Donation | 250 | |

| Computer equipment | 20,000 | |

| Repair expense | 805 | |

| Advertisement | 1728 | |

| Mileage expense | 320 | |

| Miscellaneous expense | 384 | |

| Total | 98,659 | 98,659 |

Want to see more full solutions like this?

Chapter 2 Solutions

Financial Accounting: Information for Decisions

- You have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance.3.What is the ethical dilemma you face? What are the ethical considerations? Consider your options and responsibilities as assistant controller.4.Identify the key internal and external stakeholders. What are the negative impacts that can happen if you do not follow the instructions of your supervisor?5.What are the…arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forwardYou have been recently hired as an assistant controller for XYZ Industries, a large, publically held manufacturing company. Your immediate supervisor is the controller who also reports directly to the VP of Finance. The controller has assigned you the task of preparing the year-end adjusting entries. In the receivables area, you have prepared an aging accounts receivable and have applied historical percentages to the balances of each of the age categories. The analysis indicates that an appropriate estimated balance for the allowance for uncollectible accounts is $180,000. The existing balance in the allowance account prior to any adjusting entry is a $20,000 credit balance. After showing your analysis to the controller, he tells you to change the aging category of a large account from over 120 days to current status and to prepare a new invoice to the customer with a revised date that agrees with the new category. This will change the required allowance for uncollectible accounts…arrow_forward

- As a bookkeeper of a new start-up company, you are responsible for keeping the chart of accounts up to date. At the end of each year, you analyze the accounts to verify that each account should be active for accumulation of costs, revenues and expenses. In July, the accounts payable clerk has asked you to open an account named “New Expenses”. You know that an account name should be specific and well defined. You feel that the A/P clerk might want to charge some expenses to that account that would not be appropriate. Why do you think the A/P clerk need this “New Expenses” account? Who needs to know this information and what action should you consider?arrow_forwardAs the bookkeeper of a new start-up company, you are responsible for keeping the chart of accounts up to date. At the end of each year, you analyze the accounts to verify that each account should be active for accumulation of costs, revenues, and expenses. In July, the accounts payable clerk has asked you to open an account named New Expenses. You know that an account name should be specific and well defined. You feel that the A/P clerk might want to charge some expenses to that account that would not be appropriate. Why do you think the A/P clerk needs this New Expenses account? Who needs to know this information and what action should you consider?arrow_forwardUsing EXCEL => Prepare the appropriate journal entry for each of the transactions for CampIn Inc. during the first three months of 2021 (see Attached file). Using EXCEL => Post the journal entries to the appropriate “T-Accounts.”arrow_forward

- As the bookkeeper of a new start-up company, you are responsible for keeping the chart of accounts up to date. At the end of each year, you analyze the accounts to verify that each account should be active for acumulation of costs, revenues, and expenses. In July, the accounts payable (A/P) clerk asked you to open an account named New Expenses. You know that an account name should be specific and well defined, and you're afraid the A/P clerk might charge some expenses to the account that are inappropriate. Respond to the following in a minimum of 175 words: *Why do you think the A/P clerk needs the New Expenses account? * Who needs to know this information and what action should you consider?arrow_forwardAs the bookkeeper of a new start-up company, you are responsible for keeping the chart of accounts up to date. At the end of each year, you analyze the accounts to verify that each account should be active for accumulation of costs, revenues, and expenses. In July, the accounts payable (A/P) clerk asked you to open an account named New Expenses. You know that an account name should be specific and well defined, and you're afraid the A/P clerk might charge some expenses to the account that are inappropriate. Why do you think the A/P clerk needs the New Expenses account? Who needs to know this information and what action should you consider?arrow_forwardRusty Spears, CEO of Rusty's Renovations, a custom building and repair company, is preparing documentation for a line of credit request from his commercial banker. Among the required documents is a detailed sales forecast for parts of 2017 and 2018:arrow_forward

- Before you begin this assignment, review the Tying It All Together feature in the chapter. Part of Fry’s Electronics, Inc.'s experience involves providing technical support to its customers. This includes in-home installations of electronics and also computer support at their retail store locations. Requirements Suppose Fry’s Electronics, Inc. provides $10,500 of computer support at the Dallas-Fort Worth store during the month of November. How would Fry's Electronics record this transaction? Assume all customers paid in cash. What financial statement(s) would this transaction affect? Assume Fry’s Electronics, Inc.’s Modesto, California, location received $24,000 for an annual contract to provide computer support to the local city government. How would Fry’s Electronics record this transaction? What financial statement(s) would this transaction affect? What is the difference in how revenue is recorded in requirements 1 and 2? Clearly state when revenue is recorded in each requirement.arrow_forwardPrepare an explanatory memorandum about financial performance and record keeping requirements. The operations manager of Metharom Construction has asked you to prepare an explanatory memorandum for the accounting staff. They have requested that you include the following information: A) a description of a minimum of 5 financial records that the company must maintain B) any three factors while selecting software that could assist with finance management for small business C) list any 5 regulatory requirement for lodgement and payment of statutory obligations D) a set of policies to for Debt recovery procedures (minimum 3) E) explain how financial performance will be monitored (include a minimum of 2 key performance indicators) F) set of minimum 6 written financial procedures for Metharom which will help in financial health check for stakeholders G)This document must then be sent electronically to the Operations Manager (your assessor) as well as submitted in hard copy.arrow_forwardIn the New Company File Assistant, before pressing the Next button in the 'Create your company file' window, Isabella wants to confirm some of the company settings you selected when creating the company file in MYOB. Isabella asks you to select the correct options that appear throughout the New Company File Assistant that correspond to the company settings required for Hi-Fi Way in MYOB: 12 accounting periods and 'Other' as the industry classification of the business June as the conversion month and a financial year starting in January 12 accounting periods and 'Retail Business, Other' as the industry classification of the business January as the conversion month and a financial year ending in Julyarrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,