Concept explainers

Videos

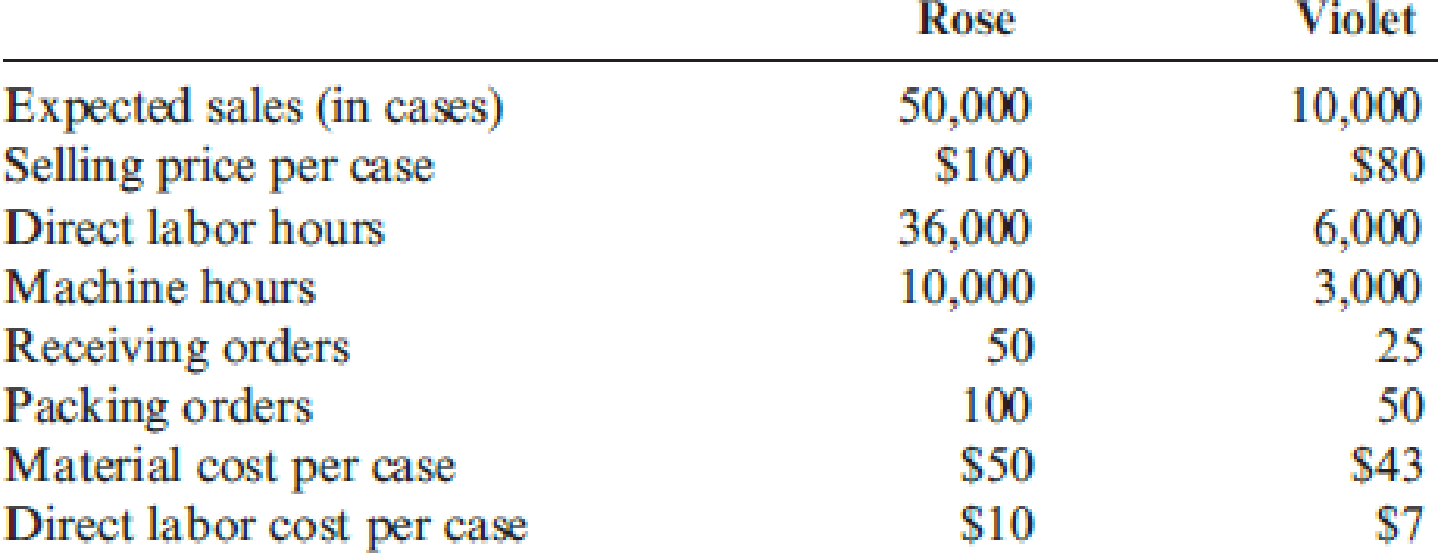

Good Scent, Inc., produces two colognes: Rose and Violet. Of the two, Rose is more popular. Data concerning the two products follow:

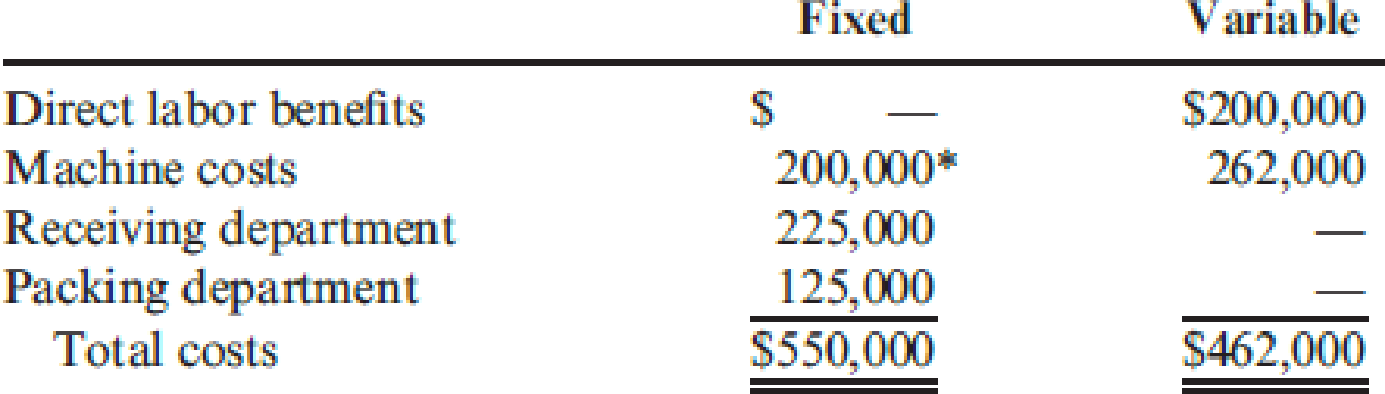

The company uses a conventional costing system and assigns

Required:

- 1. Using the conventional approach, compute the number of cases of Rose and the number of cases of Violet that must be sold for the company to break even.

- 2. Using an activity-based approach, compute the number of cases of each product that must be sold for the company to break even.

1.

Ascertain the break-even point using the conventional approach.

Explanation of Solution

Contribution Margin Ratio: The contribution margin ratio shows the amount of difference in the actual sales value and the variable expenses in percentage. This margin indicates that percentage which is available for sale above the fixed costs and the profit. The formula for variable cost ratio is shown below:

Break-Even Point: The break-even point refers to the point of sales at which the firm neither earns a profit nor suffers a loss. It is also known as the point of sales or sales value at which the firm recovers the entire cost of fixed and variable nature.

Break-Even in sales revenue: The break-even in sales revenue refers to the sales volume required to cover the fixed and variable costs and left out with neither profit nor loss.

Compute the package contribution margin units:

| Input | Price (A) | Unit Variable cost (B) | Unit Contribution margin | Sales Mix (D) |

Package Unit Contribution margin |

| Rose | $100.00 | $67.92 | $32.08 | 5 | $160.40 |

| Violet | $80.00 | $56.60 | $23.40 | 1 | $23.40 |

| Package Total | $183.80 |

Table (1)

Compute the break-even packages:

The number of break-even packages is 2,992.

Compute the break-even for Rose:

The number of break-even for Rose is 14,960.

Compute the break-even for Violet:

The number of break-even for Violet is 2,992.

Working Notes:

Compute the unit variable cost for rose:

The variable cost per unit for rose is $67.92.

Compute the unit variable cost for violet:

The variable cost per unit for violet is $56.60.

2.

Compute the break-even point and the incremental profit using the activity based costing.

Explanation of Solution

Compute the unit-based variable cost per unit:

| Particulars | Rose | Violet |

| Unit-based variable costs: | ||

| Prime costs | $60.00 | $50.00 |

| Benefits | $3.43 | $2.86 |

| Machine costs | $4.03 | $6.05 |

| Total | $67.46 | $58.91 |

| Sales Mix | ||

| Package Cost | $337.30 | $58.91 |

Table (2)

Compute the total package cost:

The total package cost is $396.21 (X1).

Compute the benefits cost per unit for rose:

The benefits cost per unit for rose is $3.43.

Compute the benefits cost per unit for violet:

The benefits cost per unit for violet is $2.86.

Compute the unit machine cost for rose:

The machine cost per unit for rose is $4.03.

Compute the unit machine cost for violet:

The machine cost per unit for violet is $6.05.

Compute the non-unit-based variable overhead cost per unit:

| Particulars | Calculations | Amount ($) |

| Non-unit-based variable costs: | ||

| Receiving (X2) | $3,000 | |

| Packing (X3) | $833.33 | |

Table (2)

Compute the sales and variable cost per unit:

| Particulars | Calculations | Amount ($) |

| Sales | $580.00 | |

| Variable cost | $396.20 | |

| Contribution margin | $183.80 |

Table (2)

CVP analysis:

Let,

X1 = Number of packages

X2 = Number of receiving orders

X3 = Number of packing orders

The number of break-even packages is 2,992.

Compute the break-even for Rose:

The number of break-even for Rose is 14,960.

Compute the break-even for Violet:

The number of break-even for Violet is 2,992.

Thus, the break-even point for Roses and Violets are same under both the requirements.

Want to see more full solutions like this?

Chapter 16 Solutions

EBK CORNERSTONES OF COST MANAGEMENT

- ABC and CVP Analysis: Multiple Products Good Scent, Inc., produces two colognes: Rose and Violet. Of the two, Rose is more popular. Data concerning the two products follow: Expected sales (in cases) Selling price per case. Direct labor hours Machine hours Receiving orders Packing orders Material cost per case $49 Direct labor cost per case $12 The company uses a conventional costing system and assigns overhead costs to products using direct labor hours. Annual overhead costs follow. They are classified as fixed or variable with respect to direct labor hours. Fixed $ Direct labor benefits Machine costs Receiving department Packing department Total costs Rose Violet 51,000 10,200 $100 36,750 9,250 52 98 All depreciation 211,000 212,500 149,000 $572 500 $83 6,400 2,700 24 51 $44 $8 Variable. $215,750 215,750 $431,500arrow_forwardLarsen, Inc., produces two types of electronic parts and has provided the following data: There are four activities: machining, setting up, testing, and purchasing. Required: 1. Calculate the activity consumption ratios for each product. 2. Calculate the consumption ratios for the plantwide rate (direct labor hours). When compared with the activity ratios, what can you say about the relative accuracy of a plantwide rate? Which product is undercosted? 3. What if the machine hours were used for the plantwide rate? Would this remove the cost distortion of a plantwide rate?arrow_forwardPotterii sells its products to large box stores and recently added a retail line of products to sell directly to consumers. These estimates are to be used in determining the overhead allocation rate for ABC: What would be the predetermined rate for each cost pool?arrow_forward

- Cicleta Manufacturing has four activities: receiving materials, assembly, expediting products, and storing goods. Receiving and assembly are necessary activities; expediting and storing goods are unnecessary. The following data pertain to the four activities for the year ending 20x1 (actual price per unit of the activity driver is assumed to be equal to the standard price): Required: 1. Prepare a cost report for the year ending 20x1 that shows value-added costs, non-value-added costs, and total costs for each activity. 2. Explain why expediting products and storing goods are non-value-added activities. 3. What if receiving cost is a step-fixed cost with each step being 1,500 orders whereas assembly cost is a variable cost? What is the implication for reducing the cost of waste for each activity?arrow_forwardChrzan, Incorporated, manufactures and sells two products: Product EO and Product NO. Data concerning the expected production of each product and the expected total direct labor-hours (DLHs) required to produce that output appear below: Product E0 Product Ne Total direct labor-hours Activity Cost Pools Labor-related Production orders Order size The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, and expected activity: Estimated Overhead Cost Multiple Choice $33.94 per MH $54.20 per MH Direct Expected Labor-Hours Production Per Unit 10.1 410 1,550 9.1 $51.98 per MH $21.40 per MH Activity Measures DLHS orders MHs Total Direct Labor- Hours $ 301,890 61,087 585,366 $948,343 The activity rate for the Order Size activity cost pool under activity-based costing is closest to: 4,141 14, 105 18,246 Product E 4,141 850 5,550 Expected Activity Product NO 14, 105 950 5,250 Total 18,246 1,800 10,800arrow_forwardAdams, Inc. has the following cost data for Product X: (Click on the icon to view the data.) Calculate the unit product cost using absorption costing and variable costing when production is 200 units, 500 units, and 1,000 units. Select the labels and enter the amounts to compute the unit product cost using absorption costing. (If an input field is not used in the table, leave the input field empty; do not select a label or enter a zero.) 200 units 1,000 units C 500 units Total unit product cost Total unit product cost Select the labels and enter the amounts to compute the unit product cost using variable costing. (If an input field is not used in the table, leave the input field empty; do not select a label or enter a zero.) 200 units 500 units 1,000 units Data table Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Print Done $35 per unit 55 per unit 9 per unit 10,000 per year - Xarrow_forward

- Windhoek Manufacturers produces two products, Amber and Black. The following cost estimates have been prepared using the traditional absorption costing approach. Selling price per unit Production costs per unit: Material costs Direct labour costs Manufacturing overhead cost Profit per unit Additional information. Estimates sales demand Machine hours per unit Required 1.1 1.2 Amber N$ Amber 69 27 6 12 24 9 000 0.75 Calculate the return per machine hour for each product if through put accounting approach is used. Calculate the profit for the period, using a throughput accounting approach, assuming the company priorities Black Black N$ Black 93 24 15 18 36 12 000 1.20 TIOLE.(arrow_forwardMoistner, Inc., manufactures and sells two products: Product E6 and Product W9. Data concerning the expected production of each product and the expected total direct labor-hours (DLHs) required to produce that output appear below: Expected Production Direct Labor-Hours Per Unit Total Direct Labor-Hours Product E6 700 7.0 4,900 Product W9 100 5.0 500 Total direct labor-hours 5,400 The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, and expected activity: Estimated Expected Activity Activity Cost Pools Activity Measures Overhead Cost Product E6 Product W9 Total Labor-related DLHs $ 233,604 4,900 500 5,400 Machine setups setups 30,942 500 400 900 Order size MHs 712,045 4,200 4,300 8,500 $ 976,591 If the company allocates all of its overhead based on direct labor-hours using its traditional costing method, the overhead assigned to each unit of…arrow_forwardDK manufactures three products, W, X and Y. Each product uses the same materials and the same type of direct labour but in different quantities. The company currently uses a cost-plus basis to determine the selling price of its products. This is based on full cost using an overhead absorption rate per direct labour hour. However, the managing director is concerned that the company may be losing sales because of its approach to setting prices. He thinks that a marginal costing approach may be more appropriate, particularly since the workforce is guaranteed a minimum weekly wage and has a three month notice period.arrow_forward

- Speedy Motors assembles and sells motor vehicles and uses standard costing. Actual data and variable costing and absorption costing income statements relating to April and May 2020 are as follows: (Click the icon to view the data.) (Click the icon to view the variable costing income statements.) (Click the icon to view the absorption costing income statements.) The variable manufacturing costs per unit of Speedy Motors are as follows: (Click the icon to view the variable manufacturing costs per unit.) Read the requirements. Requirement 1. Prepare income statements for Speedy Motors in April and May 2020 under throughput costing. Begin by completing the top portion of the statement, then the bottom portion. (Complete all input fields. Enter a "0" for any zero amounts.) Revenues Direct material cost of goods sold Beginning inventory Direct materials Cost of goods available for sale Deduct ending inventory Total direct material cost of goods sold Manufacturing costs April 2020 6,900,000…arrow_forwardDK manufactures three products, W, X and Y. Each product uses the same materials and the same type of direct labour but in different quantities. The company currently uses a cost plus basis to determine the selling price of its products. This is based on full cost using an overhead absorption rate per direct labour hour. However, the managing director is concerned that the company may be losing sales because of its approach to setting prices. He thinks that a marginal costing approach may be more appropriate, particularly since the workforce is guaranteed a minimum weekly wage and has a three month notice period. The direct costs of the three products are shown below: notice period. product w x y Budgeted annual production (units) 15,000 24,000 20,000 $ per unit $ per unit $ per unit Direct materials 35 40 45 Direct labour ($10 per hour) 40 30 50 In addition to the above direct costs, DK incurs annual indirect production costs of $1,044,000. a)Calculate the…arrow_forwardDK manufactures three products, W, X and Y. Each product uses the same materials and the same type of direct labour but in different quantities. The company currently uses a cost plus basis to determine the selling price of its products. This is based on full cost using an overhead absorption rate per direct labour hour. However, the managing director is concerned that the company may be losing sales because of its approach to setting prices. He thinks that a marginal costing approach may be more appropriate, particularly since the workforce is guaranteed a minimum weekly wage and has a three month notice period. Required: a) Given the managing director’s concern about DK’s approach to setting selling prices, discuss the advantages and disadvantages of marginal cost plus pricing AND total cost-plus pricing. The direct costs of the three products are shown below: Product W X Y Budgeted annual production (units) 15,000 24,000 20,000 $ per unit $ per unit $ per unit Direct materials…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College