Individual Income Taxes

43rd Edition

ISBN: 9780357109731

Author: Hoffman

Publisher: CENGAGE LEARNING - CONSIGNMENT

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 15, Problem 3CPA

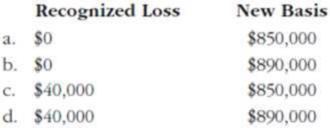

Chad owned an office building that was destroyed in a tornado. The area was declared a Federal disaster area. The adjusted basis of the building at the time was $890,000. After the deductible, Chad received an insurance check for $850,000. He used the $850,000 to purchase a new building that same year. How much is Chad’s recognized loss, and what is his basis in the new building?

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Net income or net loss

Need help with this question solution general accounting

What percentage will opereting cash flow change? Accounting

Chapter 15 Solutions

Individual Income Taxes

Ch. 15 - Prob. 1DQCh. 15 - Prob. 2DQCh. 15 - Prob. 3DQCh. 15 - Prob. 4DQCh. 15 - LO.2 Melissa owns a residential lot in Spring...Ch. 15 - LO.2 Ross would like to dispose of some land he...Ch. 15 - Prob. 7DQCh. 15 - Prob. 8DQCh. 15 - Prob. 9DQCh. 15 - Prob. 10DQ

Ch. 15 - Prob. 11DQCh. 15 - LO.3 Reba, a calendar year taxpayer, owns an...Ch. 15 - Prob. 13DQCh. 15 - Prob. 14DQCh. 15 - Prob. 15DQCh. 15 - Prob. 16CECh. 15 - Prob. 17CECh. 15 - Prob. 18CECh. 15 - Prob. 19CECh. 15 - LO.3 On June 5, 2019, Brown, Inc., a calendar year...Ch. 15 - LO.3 Camilos property, with an adjusted basis of...Ch. 15 - Prob. 22CECh. 15 - Prob. 23CECh. 15 - Prob. 24CECh. 15 - Prob. 25CECh. 15 - Prob. 26CECh. 15 - Prob. 27PCh. 15 - Prob. 28PCh. 15 - Prob. 29PCh. 15 - Prob. 30PCh. 15 - Prob. 31PCh. 15 - Prob. 32PCh. 15 - Prob. 33PCh. 15 - Ed owns investment land with an adjusted basis of...Ch. 15 - Prob. 35PCh. 15 - Prob. 36PCh. 15 - Prob. 37PCh. 15 - Prob. 38PCh. 15 - Prob. 39PCh. 15 - Prob. 40PCh. 15 - LO.3 Howards roadside vegetable stand (adjusted...Ch. 15 - Prob. 42PCh. 15 - Prob. 43PCh. 15 - Prob. 44PCh. 15 - Prob. 45PCh. 15 - Prob. 46PCh. 15 - What are the maximum postponed gain or loss and...Ch. 15 - Prob. 48PCh. 15 - Prob. 49PCh. 15 - Prob. 50PCh. 15 - Prob. 51PCh. 15 - Prob. 52PCh. 15 - Prob. 53PCh. 15 - Prob. 54PCh. 15 - Prob. 55PCh. 15 - Prob. 56PCh. 15 - Devon Bishop, age 45, is single. He lives at 1507...Ch. 15 - Prob. 1RPCh. 15 - Prob. 2RPCh. 15 - Taylor owns a 150-unit motel that was constructed...Ch. 15 - Prob. 6RPCh. 15 - Prob. 1CPACh. 15 - Susie purchased her primary residence on March 15,...Ch. 15 - Chad owned an office building that was destroyed...Ch. 15 - Prob. 4CPACh. 15 - Marsha exchanged land used in her business in...Ch. 15 - Prob. 6CPACh. 15 - Prob. 7CPA

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- provide correct answerarrow_forwardWrite down as many descriptions describing rock and roll that you can. From these descriptions can you come up with s denition of rock and roll? What performers do you recognize? What performers don’t you recognize? What can you say about musical inuence on these current rock musicians? Try to break these inuences into genres and relate them to the rock musicians. What does Mick Jagger say about country artists? What does pioneering mean? What kind of ensembles warrow_forwardRecently, Abercrombie & Fitch has been implementing a turnaround strategy since its sales had been falling for the past few years (11% decrease in 2014, 8% in 2015, and just 3% in 2016.) One part of Abercrombie's new strategy has been to abandon its logo-adorned merchandise, replacing it with a subtler look. Abercrombie wrote down $20.6 million of inventory, including logo-adorned merchandise, during the year ending January 30, 2016. Some of this inventory dated back to late 2013. The write-down was net of the amount it would be able to recover selling the inventory at a discount. The write-down is significant; Abercrombie's reported net income after this write-down was $35.6 million. Interestingly, Abercrombie excluded the inventory write-down from its non-GAAP income measures presented to investors; GAAP earnings were also included in the same report. Question: What impact would the write-down of inventory have had on Abercrombie's expenses, Gross margin, and Net income?arrow_forward

- Recently, Abercrombie & Fitch has been implementing a turnaround strategy since its sales had been falling for the past few years (11% decrease in 2014, 8% in 2015, and just 3% in 2016.) One part of Abercrombie's new strategy has been to abandon its logo-adorned merchandise, replacing it with a subtler look. Abercrombie wrote down $20.6 million of inventory, including logo-adorned merchandise, during the year ending January 30, 2016. Some of this inventory dated back to late 2013. The write-down was net of the amount it would be able to recover selling the inventory at a discount. The write-down is significant; Abercrombie's reported net income after this write-down was $35.6 million. Interestingly, Abercrombie excluded the inventory write-down from its non-GAAP income measures presented to investors; GAAP earnings were also included in the same report. Question: What impact would the write-down of inventory have had on Abercrombie's assets, Liabilities, and Equity?arrow_forwardNeed answer general Accountingarrow_forwardProvide correct answer of this question answer general Accountingarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income Taxes

Accounting

ISBN:9780357109731

Author:Hoffman

Publisher:CENGAGE LEARNING - CONSIGNMENT

Operating Loss Carryback and Carryforward; Author: SuperfastCPA;https://www.youtube.com/watch?v=XiYhgzSGDAk;License: Standard Youtube License