Concept explainers

(1)

Trading securities: These are short-term investments in debt and equity securities with an intention of trading and earning profits due to changes in market prices.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in

stockholders’ equity accounts. - Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

To journalize: The stock investment transactions in the books of Company Z

(1)

Explanation of Solution

Prepare journal entry for the purchase of 4,800 shares of Company AP, at $26 per share, and a brokerage commission of $192.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| February | 14 | Investments–Company AP Stock | 124,992 | ||

| Cash | 124,992 | ||||

| (To record purchase of shares for cash) | |||||

Table (1)

Explanation:

- Investments–Company AP Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company AP’s stock.

Prepare journal entry for the purchase of 2,300 shares of Company

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| April | 1 | Investments–Company AR Stock | 43,792 | ||

| Cash | 43,792 | ||||

| (To record purchase of shares for cash) | |||||

Table (2)

Explanation:

- Investments–Company AR Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company AR’s stock.

Prepare journal entry for sale of 600 shares of Company AP, at $32, with a brokerage of $100.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| June | 1 | Cash | 19,100 | ||

| Gain on Sale of Investments | 3,476 | ||||

| Investments–Company AP Stock | 15,624 | ||||

| (To record sale of shares) | |||||

Table (3)

Explanation:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Loss on Sale of Investments is a loss or expense account. Since losses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Investments–Company AP Stock is an asset account. Since stock investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the realized gain (loss) on sale of stock.

Step 1: Compute cash received from sale proceeds.

Step 2: Compute cost of stock investment sold.

Step 3: Compute realized gain (loss) on sale of stock.

Note: Refer to Steps 1 and 2 for value and computation of cash received and cost of stock investment sold.

Prepare journal entry for the dividend received from Company AP for 4,200 shares.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| June | 27 | Cash | 840 | ||

| Dividend Revenue | 840 | ||||

| (To record receipt of dividend revenue) | |||||

Table (4)

Explanation:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received on Company AP’s stock.

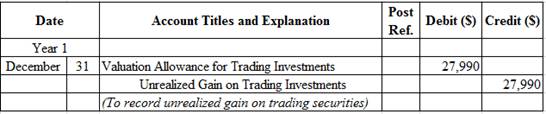

Prepare

Table (5)

Explanation:

- Valuation Allowance for Trading Investments is a contra-asset account. The account is credited because the market price was increased (gain) to $181,150 from the cost of $153,160.

- Unrealized Gain on Trading Investments is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since gain has occurred and increase stockholders’ equity value, and an increase in stockholders’ equity value is debited.

Working Notes:

Compute the unrealized gain (loss) as on December 31.

Step 1: Compute the fair value of the portfolio of the trading investment.

| Security | Number of Shares |

| Fair Market Value | = | Fair Market Value of Investment |

| Company AP | 4,200 shares |

| $33.00 | = | $138,600 |

| Company AR | 2,300 shares |

| 18.50 | = | 42,550 |

| Total | $181,150 | ||||

Table (6)

Step 2: Compute the cost per share of Company AP.

Step 3: Compute the cost per share of Company AR.

Step 4: Compute the cost of the portfolio of the trading investment, as on December 31.

| Security | Number of Shares |

| Cost per Share | = | Cost of Investment |

| Company AP | 4,200 shares |

| $26.04 | = | $109,368 |

| Company AR | 2,300 shares |

| 19.04 | = | 43,792 |

| Total | $153,160 | ||||

Table (7)

Note: Refer to Steps 3 and 4 for cost per share of Company AP and Company AR.

Step 5: Compute the unrealized gain (loss) as on December 31.

| Details | Amount ($) |

| Trading investments at fair value, December 31 (From Table-6) | $181,150 |

| Less: Trading investments at cost, December 31 (From Table-7) | (153,160) |

| Unrealized loss on trading investments | $27,990 |

Table (8)

Prepare journal entry for the purchase of 1,200 shares of Company AT, at $65 per share, and a brokerage commission of $120.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 2 | |||||

| March | 14 | Investments–Company AT Stock | 78,120 | ||

| Cash | 78,120 | ||||

| (To record purchase of shares for cash) | |||||

Table (9)

Explanation:

- Investments–Company AT Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company AT’s stock.

Prepare journal entry for the dividend received from Company AP for 4,200 shares.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 2 | |||||

| June | 26 | Cash | 882 | ||

| Dividend Revenue | 882 | ||||

| (To record receipt of dividend revenue) | |||||

Table (10)

Explanation:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received on Company AP’s stock.

Prepare journal entry for sale of 480 shares of Company AT at $60, with a brokerage of $50.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 2 | |||||

| July | 30 | Cash | 28,750 | ||

| Loss on Sale of Investments | 2,498 | ||||

| Investments–Company AT Stock | 31,248 | ||||

| (To record sale of shares) | |||||

Table (11)

Explanation:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Loss on Sale of Investments is an expense account. Since expenses and losses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Investments–Company AT Stock is an asset account. Since stock investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the realized gain (loss) on sale of stock.

Step 1: Compute cash received from sale proceeds.

Step 2: Compute cost of stock investment sold.

Step 3: Compute realized gain (loss) on sale of stock.

Note: Refer to Steps 1 and 2 for value and computation of cash received and cost of stock investment sold.

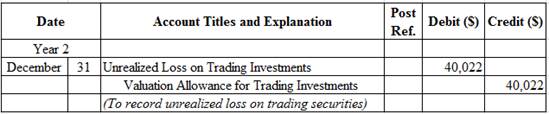

Prepare adjusting entry for valuation of trading securities transaction.

Table (12)

Explanation:

- Unrealized Loss on Trading Investments is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since loss has occurred and losses decrease stockholders’ equity value, and a decrease in stockholders’ equity value is debited.

- Valuation Allowance for Trading Investments is a contra-asset account. The account is credited because the market price was decreased (loss).

Working Notes:

Compute the unrealized gain (loss) as on December 31.

| Details | Amount ($) |

| Unrealized loss as on December 31, Year 2 | $12,032 |

| Add: Unrealized gain as on December 31, Year 1 (From Table-8) | 27,990 |

| Unrealized loss on trading investments | $40,022 |

Table (13)

(2)

To indicate: The presentation of trading investments on the current assets section of the balance sheet

(2)

Explanation of Solution

Balance sheet presentation:

| Company Z | ||

| Balance Sheet (Partial) | ||

| December 31, Year 2 | ||

| Assets | ||

| Current assets: | ||

| Trading investments (at cost) | $200,032 | |

| Less valuation allowance for trading investments | (12,032) | |

| Trading investments (at fair value) | $188,000 | |

Table (14)

(3)

To discuss: The reporting of trading investments on the financial statements

(3)

Explanation of Solution

Unrealized gain or loss is the result of change in trading investments cost and fair values, and reported as Other Revenues (Losses) on the income statement. The unrealized gain will be added to the net income and unrealized loss will be deducted from the net income. In the Year 1, Company Z would report $27,990 of unrealized gain as Other Income on the income statement. In the Year 2, Company Z would report $40,022 of unrealized loss as Other Losses on the income statement.

Want to see more full solutions like this?

Chapter 15 Solutions

CENGAGENOW 6 TERMS ACCESS CARD 27TH ED.

- Forte Inc. produces and sells theater set designs and costumes. The company began operations on January 1, Year 1. The following transactions relate to securities acquired by Forte Inc., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record these transactions. 2. Prepare the investment-related asset and stockholders equity balance sheet presentation for Forte Inc. on December 31, Year 2, assuming that the Retained Earnings balance on December 31, Year 2, is 389,000.arrow_forwardFair value journal entries, trading investmentsThe investments of Charger Inc. include a single investment: 14,500shares of Raiders Inc. common stock purchased on February 24, Year 1,for $38 per share including brokerage commission. These shares werelassified as trading securities. As of the December 31, Year 1, balancesheet date, the share price had increased to $42 per share. a. Journalize the entries to acquire the investment on February 24 andrecord the adjustment to fair value on December 31, Year 1.b. How is the unrealized gain or loss for trading investments reported onthe financial statements?arrow_forwardJournal entries for trading investments Gruden Bancorp Inc. purchased a portfolio of trading securities during 20Y3, its first year of operations. The cost and fair value of this portfolio on December 31, 20Y3, are as follows: Issuing Company Cost Fair Value Griffin Inc. $14,070 $13,230 Luck Company 22,960 21,350 Wilson Company 9,300 9,490 Total $46,330 $44,070 On May 10, 20Y4, Gruden Bancorp Inc. purchased trading securities of Carroll Inc. for $15,610. Journalize the entries to record the following: If an amount box does not require an entry, leave it blank. a. The adjusting entry for the portfolio of trading securities on December 31, 20Y3. 20Y3, Dec. 31 b. The May 10, 20Y4, purchase of Carroll Inc. securities. 20Y4, May 10 c. The adjusting entry for the portfolio of trading securities on December 31, 20Y4. Assume that except for the purchase of Carroll Inc. securities there were no other transactions involving trading securities in 20Y4. In addition, assume that the fair value of…arrow_forward

- Journal entries for trading investments Gruden Bancorp Inc. purchased a portfolio of trading securities during 20Y3, its first year of operations. The cost and fair value of this portfolio on December 31, 20Y3, are as follows: Issuing Company Cost Fair Value Griffin Inc. $40,000 $44,800 Luck Company 37,500 33,750 Wilson Company 40,000 37,000 Total $117,500 $115,550 On May 10, 20Y4, Gruden Bancorp Inc. purchased trading securities of Carroll Inc. for $34,900. Journalize the entries to record the following: If an amount box does not require an entry, leave it blank. a. The adjusting entry for the portfolio of trading securities on December 31, 20Y3. 20Y3, Dec. 31 fill in the blank 0de958062fa6ff5_2 fill in the blank 0de958062fa6ff5_3 fill in the blank 0de958062fa6ff5_5 fill in the blank 0de958062fa6ff5_6 b. The May 10, 20Y4, purchase of Carroll Inc. securities. 20Y4, May 10 fill in the blank…arrow_forwardBalance Sheet Presentation of Available-for-Sale Investments During Year 1, its first year of operations, Galileo Company purchased two available-for-sale investments as follows: Security Shares Purchased Cost Hawking Inc. 760 $34,124 Pavlov Co. 2,060 48,204 Assume that as of December 31, Year 1, the Hawking Inc. stock had a market value of $53 per share and the Pavlov Co. stock had a market value of $42 per share. Galileo Company had net income of $264,300 and paid no dividends for the year ending December 31, Year 1. All of the available-for-sale investments are classified as current assets. a. Prepare the Current Assets section of the balance sheet presentation for the available-for-sale investments. Galileo Company Balance Sheet (selected items) December 31, Year 1 Assets Current Assets: $ $ b. Prepare the Stockholders' Equity section of the balance sheet to reflect the earnings and unrealized gain (loss) for…arrow_forwardFair Value Journal Entries, Available-for-Sale Investments The investments of Steelers Inc. include a single investment: 8,900 shares of Bengals Inc. common stock purchased on September 12, Year 1, for $8 per share including brokerage commission. These shares were classified as available-for-sale securities. As of the December 31, Year 1, balance sheet date, the share price declined to $6 per share. a. Journalize the entries to acquire the investment on September 12 and record the adjustment to fair value on December 31, Year 1. Year 1 Sept. 12 Year 1 Dec. 31 b. How is the unrealized gain or loss for available-for-sale investments disclosed on the financial statements? Unrealized Gain (Loss) on Available-for-Sale Investments is reported in the of thearrow_forward

- Journalizing equity investment transactions; fair value method Seamus Industries Inc. buys and sells investments as part of its ongoing cash management. The following investment transactions were completed during the year: Feb. 24. Purchased 1,000 shares of Tett Co.'s common stock for $85 per share. May 16. Purchased 2,500 shares of Isaacson Co.'s common stock for $35. July 14. Sold 400 shares of Tett Co. stock for $102 per share. Aug. 12. Sold 750 shares of Isaacson Co. stock for $32 per share. Oct. 31. Received dividends of $0.40 per share on Tett Co. stock. Dec. 31. At the end of the accounting period, the fair value of the remaining 600 shares of Tett Co.'s stock was $110 per share. The fair value of the remaining 1,750 shares of Isaacson Co.'s stock was $30 per share. Journalize the entries for these transactions. If an amount box does not require an entry, leave it blank. Feb. 24 May 16 July 14 Aug. 12 Oct. 31 Dec. 31arrow_forwardFair Value Journal Entries, Available-for-Sale Investments The investments of Steelers Inc. include a single investment: 8,100 shares of Bengals Inc. common stock purchased on September 12, Year 1, for $13 per share including brokerage commission. These shares were classified as available-for-sale securities. As of the December 31, Year 1, balance sheet date, the share price declined to $10 per share. CashCash DividendsInterest ReceivableInvestments-Bengals Inc. StockRetained EarningsUnrealized Gain (Loss) on Available-for-Sale InvestmentsValuation Allowance for Available-for-Sale Investme a. Journalize the entries to acquire the investment on September 12 and record the adjustment to fair value on December 31, Year 1. Year 1 Sept. 12 fill in the blank fb2219094fa204f_2fill in the blank fb2219094fa204f_4Year 1 Dec. 31 fill in the blank fb2219094fa204f_6fill in the blank fb2219094fa204f_8b. How is the unrealized gain or loss for available-for-sale investments disclosed on the financial…arrow_forwardBalance Sheet Presentation of Available-for-Sale Investments During Year 1, its first year of operations, Galileo Company purchased two available-for-sale investments as follows: Security Shares Purchased Cost Hawking Inc. 860 $43,602 Pavlov Co. 2,330 61,512 Assume that as of December 31, Year 1, the Hawking Inc. stock had a market value of $60 per share and the Pavlov Co. stock had a market value of $48 per share. Galileo Company had net income of $337,400 and paid no dividends for the year ending December 31, Year 1. All of the available-for-sale investments are classified as current assets. a. Prepare the Current Assets section of the balance sheet presentation for the available-for-sale investments. Galileo Company Balance Sheet (selected items) December 31, Year 1 Assets Current Assets: $fill in the blank 6f30cb02405dfbc_2 Plus Unrealized Gain (Loss) on Available-for-Sale Investments fill in the blank 6f30cb02405dfbc_4 $fill…arrow_forward

- Balance Sheet Presentation of Available-for-Sale Investments During Year 1, its first year of operations, Galileo Company purchased two available-for-sale investments as follows: Security Shares Purchased Cost Hawking Inc. 860 $43,602 Pavlov Co. 2,330 61,512 Assume that as of December 31, Year 1, the Hawking Inc. stock had a market value of $60 per share and the Pavlov Co. stock had a market value of $48 per share. Galileo Company had net income of $337,400 and paid no dividends for the year ending December 31, Year 1. All of the available-for-sale investments are classified as current assets. available for sale investments at cost/available for sale investments at fair value/common stock/retained earning/unrealized gain (loss) on available for sale investments/less retained earning/less unrealized gain (loss) on available for sale /plus retained earnings/plus unrealized gain (loss) on available/plus valuation allowance for available for sale/less unrealized gain…arrow_forwardFair Value Journal Entries, Trading Investments Gruden Bancorp Inc. purchased a portfolio of trading securities during Year 1. The cost and fair value of this portfolio on December 31, Year 1, was as follows: Name Number of Shares Total Cost Total Fair Value Griffin Inc. 1,100 $14,740 $13,860 Luck Company 850 27,880 25,930 Wilson Company 250 7,250 7,400 Total $49,870 $47,190 On May 10, Year 2, Gruden Bancorp Inc. purchased 500 shares of Carroll Inc., at $29 per share plus a $80 brokerage commission. Provide the journal entries to record the following: a. The adjustment of the trading security portfolio to fair value on December 31, Year 1. Year 1, Dec. 31 b. The May 10, Year 2, purchase of Carroll Inc. stock. Year 2, May 10arrow_forwardAssessing Financial Statement Effects of Trading and Available-for-Sale Securities Use the financial statement effects template to record the following four transactions involving investments in marketable securities. Purchased 6,000 common shares of Liu, Inc., at $12.25 cash per share. Received a cash dividend of $1.50 per common share from Liu. Year-end market price of Liu common stock is $11.25 per share. Sold all 6,000 common shares of Liu for $66,300. Use negative signs with answers, when appropriate. Balance Sheet Transaction Cash Asset + Noncash Assets = Liabilities + Contributed Capital + Earned Capital (1) Answer Answer Answer Answer Answer (2) Answer Answer Answer Answer Answer (3) Answer Answer Answer Answer Answer (4) Answer Answer Answer Answer Answer Income Statement Revenue - Expenses = Net Income Answer Answer Answer Answer Answer Answerarrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning