Concept explainers

Videos

Calculation of annual lease payments; residual value

• LO15–2, LO15–6

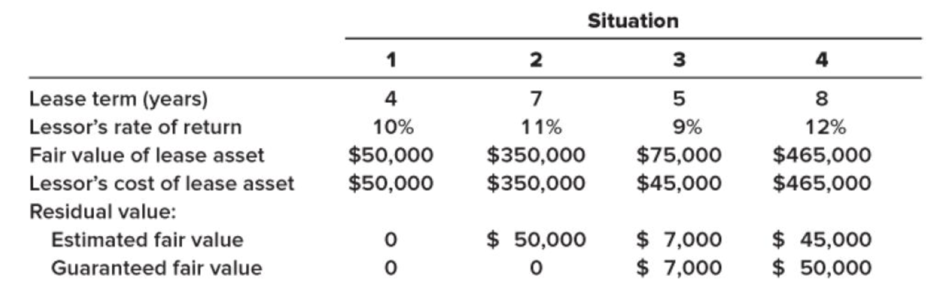

Each of the four independent situations below describes a finance lease in which annual lease payments are payable at the beginning of each year. The lessee is aware of the lessor’s implicit

Required:

For each situation, determine:

a. The amount of the annual lease payments as calculated by the lessor.

b. The amount the lessee would record as a right-of-use asset and a lease liability.

(Situation 1) (a)

Lease

Lease is a contractual agreement whereby the right to use an asset for a particular period of time is provided by the owner of the asset to the user of the asset. The owner, who possesses the asset, is termed as ‘Lessor’ and user, to whom the right is transferred to, is termed as ‘Lessee’.

To Determine: the annual lease payments as calculated by the lessor.

Explanation of Solution

The lease payments at the beginning of each year is calculated by dividing fair value of the leased asset by present value of annuity for 4 years at the rate of 10%.

Therefore, annual lease payment as calculated by lessor is $14,340.

(Situation 1) (b)

Explanation of Solution

The lessor cost of lease asset is reported by the lessee as right-of-use asset$50,000.

Therefore, amount the lessee would record as right-of-use and lease liability is $50,000.

(Situation 2) (a)

Explanation of Solution

Working notes:

Calculate the present value of residual value

Calculate the amount to be recovered through periodic lease payments

| Particulars | Amounts ($) |

| Amount to be recovered (Fair value) | 350,000 |

| Less: Present value of residual value (1) | 24,083 |

| Amount to be recovered through periodic lease payments | 325,917 |

(2)

In case of lessor, even if the residual value is not guaranteed, the lessor is expected to receive. So, the lessor will assess the residual asset as contributing to amount needed to recover its investment causing the lessee’s lease payments to be lower.

Therefore, annual lease payment as calculated by lessor is $62,310.

(Situation 2) (b)

Explanation of Solution

Calculate the lessee would record as right-of-use asset and lease liability

Therefore, amount the lessee would record as right-of-use and lease liability is $325,917.

(Situation 3) (a)

Explanation of Solution

Working notes:

Calculate the present value of residual value

Calculate the amount to be recovered through periodic lease payments

| Particulars | Amounts ($) |

| Amount to be recovered (Fair value) | 75,000 |

| Less: Present value of residual value (4) | 4,550 |

| Amount to be recovered through periodic lease payments | 70,450 |

(5)

In case of lessor, even if the residual value is not guaranteed, the lessor is expected to receive. So, the lessor will assess the residual asset as contributing to amount needed to recover its investment causing the lessee’s lease payments to be lower.

Therefore, annual lease payment as calculated by lessor is $16,617.

(Situation 3) (b)

Explanation of Solution

Calculate the lessee would record as right-of-use asset and lease liability

Therefore, amount the lessee would record as right-of-use and lease liability is $70,450.

(Situation 4) (a)

Explanation of Solution

Working notes:

Calculate the present value of excess guaranteed residual value

Calculate the present value of residual value

Calculate the amount to be recovered through periodic lease payments

| Particulars | Amounts ($) |

| Amount to be recovered (Fair value) | 465,000 |

| Less: Present value of excess guaranteed residual value (7) | 2,019 |

| Less: Present value of residual value (8) | 18,175 |

| Amount to be recovered through periodic lease payments | 444,806 |

(9)

If a lessee guaranteed residual value is expected, the present value of the payments is added to the present value of lease payments which the lessee records as right-of-use of asset and lease liability. In case of a finance lease, the lessor records it as lease receivable.

Therefore, annual lease payment as calculated by lessor is $79,947.

(Situation 4) (b)

Explanation of Solution

Calculate the lessee would record as right-of-use asset and lease liability

Therefore, amount the lessee would record as right-of-use and lease liability is $446,825.

Want to see more full solutions like this?

Chapter 15 Solutions

SPICELAND GEN CMB LL INTRM ACCTG; CNCT

- Part 1: New Lease Accounting – IFRS 16 Leases Effect Analysis. What are the top three industries most affected by IFRS 16 as measured by the present value of future payments for off-balance-sheet leases to total assets? Which leased assets propel them to the top three? Also, discuss the extent that smaller firms would be affected by IFRS 16. Which payments are to be included in the measurement of lease assets and lease liabilities? Also, discuss the pros and cons of excluding the following payments from the measurement. Variable lease payments linked to future use or sales Optional payments relating to lease-extension option when a lessee is not reasonably certain to exercise the option. Discuss the effects of the new accounting on the following items and ratios of lessees. Provide reason(s) behind all effects. EBITDA, operating profit, and profit before tax Operating cash flow, financing cash flow, and total cash flow Debt to equity, current ratio, and return on total assetsarrow_forwardquestion 1: There are nine itsms list under "quantitive disclosure" for the lease. Why aren't short-term lease cost and variable lease cost shown? question 2 : What is the amount cintractual obligations and options that the lessee is reasonably certain to excercise for Operating lease? financing lease?arrow_forward28 Which one of the following is a correct statement of one of the indicators of a finance lease?A. The lease transfers ownership of the property to the lessor.B. The lease contains a purchase option.C. The lease term is for the major part of the economic life of the leased property.D. The minimum lease payments (excluding executory costs) equals or exceeds 90% of the fair value of the leased property.arrow_forward

- A lessee has developed the following information regarding a lease contract, with payments due at the beginning of the period. Use this information to determine the amount at which the lease obligation will initially be recorded. Description Amount Present value Present value of total of annuity due amount Annual lease $4,500 S16.528 S14,258 payment Discount rate 6% Number of periods 4 Purchase option $300 S238 Group of answer choices: 18,000 14,495 16,528 14,258 18,300 16,766arrow_forwardExercise 15-9 (Algo) Lessor calculation of annual lease payments; lessee calculation of asset and liability [LO15-2] Each of the three independent situations below describes a finance lease in which annual lease payments are payable at the beginning of each year. The lessee is aware of the lessor's implicit rate of return. Note: Use tables, Excel, or a financial calculator. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) Situation 1 2 3 Lease term (years) 11 21 4 Lessor's rate of return (known by lessee) 10% 8% 11% Lessee's incremental borrowing rate 11% 9% 10% Fair value of lease asset $800,000 $1,180,000 $385,000 Required: a. & b. Determine the amount of the annual lease payments as calculated by the lessor and the amount the lessee would record as a right-of-use asset and a lease liability, for each of the above situations. Note: Round your answers to the nearest whole dollar.arrow_forwardExercise 15-9 (Algo) Lessor calculation of annual lease payments; lessee calculation of asset and liability [LO15-2] Each of the three independent situations below describes a finance lease in which annual lease payments are payable at the beginning of each year. The lessee is aware of the lessor's implicit rate of return. Note: Use tables, Excel, or a financial calculator. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) Lease term (years) Lessor's rate of return (known by lessee) Lessee's incremental borrowing rate Fair value of lease asset Situation 1 Situation 2 Situation 3 Lease Payments Right-of-use Asset/Lease 1 Payable 10 10% 11% $790,000 Situation 2 20 8% 9% Required: a. & b. Determine the amount of the annual lease payments as calculated by the lessor and the amount the lessee would record as a right-of-use asset and a lease liability, for each of the above situations. Note: Round your answers to the nearest whole dollar. $1,170,000 5 11% 10% $375,000arrow_forward

- 29 Lessors shall recognize assets held under a finance lease in a statement of financial position as a receivable at an amount equal to theA. gross investment in the lease B. net investment in the lease C. gross rentals D. residual value, whether guaranteed or unguaranteedarrow_forwardPart 1: New Lease Accounting –IFRS 16 Leases Effect Analysis. Identify differences between IFRS 16 and U.S. GAAP new lease accounting (ASC Topic 842). Based on these differences, discuss which one (IFRS or U.S. GAAP) you favor and why? Discuss three main features of the two transition methods for lessees under ASC 842 and IFRS 16. Which transition method would investors likely prefer? Why? Which transition method may be preferred by companies? Why?arrow_forward*see attached What is the gross investment in the lease? a. 8,652,705b. 9,052,705c. 6,000,000d. 8,252,705arrow_forward

- Each of the three independent situations below describes a finance lease in which annual lease payments are payable at the end of each year. The lessee is aware of the lessor’s implicit rate of return. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Situation 1 2 3 Lease term (years) 12 20 3 Lessor's rate of return (known by lessee) 10% 8% 11% Lessee's incremental borrowing rate 11% 9% 10% Fair value of lease asset $650,000 $1,005,000 $210,000 Required:a. & b. Determine the amount of the annual lease payments as calculated by the lessor and the amount the lessee would record as a right-of-use asset and a lease liability, for each of the above situations. (Round your answers to the nearest whole dollar.)arrow_forwardWhen a lease qualifies as a finance lease, what amount is initially recorded as the cost of the right-of-use asset? A) The present value of the lease payments B) The sum of the gross (undiscounted) lease payments. O A O B « Previous Next Not saved Submit Quizarrow_forward36. Which of the following would be included in the Lease Receivable account?I. Guaranteed residual value.II. Unguaranteed residual value.III. Executory costsIV. Rental payments. II, III, and IV. I and III only. I and II only. I, II, and IV.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education