INTERMEDIATE ACCOUNTING (LCPO)

10th Edition

ISBN: 9781264473441

Author: SPICELAND

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 15, Problem 15.1E

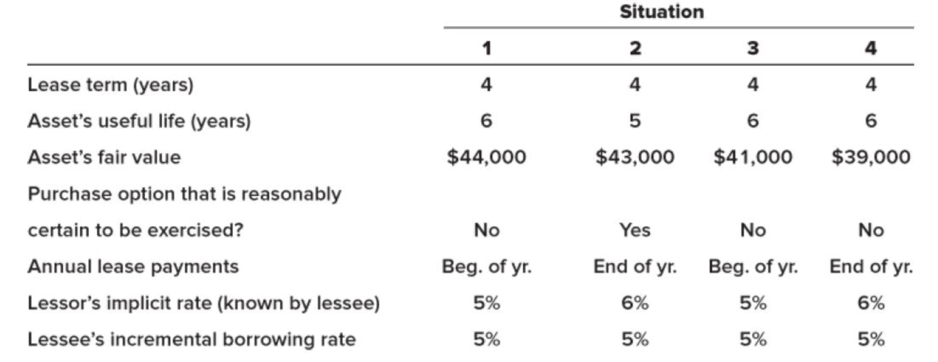

Lease classification

• LO15–1

Each of the four independent situations below describes a lease requiring annual lease payments of $10,000. For each situation, determine the appropriate lease classification by the lessee and indicate why.

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Direct materials price variance

$ 36,000

204,000

The Drysdale, Koufax, and Marichal partnership has the following balance sheet immediately prior to liquidation:

Cash

Noncash assets

Liabilities

Drysdale, loan

$ 50,000

10,000

Total assets

$ 240,000

Drysdale, capital (50%)

Koufax, capital (30%)

Marichal, capital (20%)

Total liabilities and capital

70,000

60,000

50,000

$ 240,000

Required:

a-1. Determine the maximum loss that can be absorbed in Step 1. Then, assuming that this loss has been incurred, determine the

next maximum loss that can be absorbed in Step 2.

a-2. Liquidation expenses are estimated to be $15,000. Prepare a predistribution schedule to guide the distribution of cash.

b. Assume that assets costing $74,000 are sold for $60,000. How is the available cash to be divided?

Complete this question by entering your answers in the tabs below.

Calculate GP ratio round answers to decimal place

Chapter 15 Solutions

INTERMEDIATE ACCOUNTING (LCPO)

Ch. 15 - Prob. 15.2QCh. 15 - Prob. 15.3QCh. 15 - Prob. 15.4QCh. 15 - A lessee should classify a lease transaction as a...Ch. 15 - Lukawitz Industries leased non-specialized...Ch. 15 - In accounting for a finance lease/sales-type...Ch. 15 - What is selling profit on a sales-type lease? How...Ch. 15 - At the beginning of an operating lease, the lessee...Ch. 15 - At the beginning of an operating lease, the lessor...Ch. 15 - In accounting for an operating lease, how are the...

Ch. 15 - Briefly describe the conceptual basis for asset...Ch. 15 - In a financing lease, front loading of lease...Ch. 15 - The discount rate influences virtually every...Ch. 15 - A lease that has a lease term (including any...Ch. 15 - A lease might specify that lease payments may be...Ch. 15 - What is a purchase option? How does it affect...Ch. 15 - A six-year lease can be renewed for two additional...Ch. 15 - Culinary Creations leased kitchen equipment under...Ch. 15 - What situations cause us to remeasure a lease...Ch. 15 - Prob. 15.21QCh. 15 - Compare the way a purchase option that is...Ch. 15 - What nonlease costs might be included as part of...Ch. 15 - The lessors initial direct costs often are...Ch. 15 - When are initial direct costs recognized in an...Ch. 15 - Prob. 15.26QCh. 15 - Prob. 15.27QCh. 15 - Prob. 15.28QCh. 15 - When a company sells an asset and simultaneously...Ch. 15 - Prob. 15.30QCh. 15 - Lease classification LO151 (Note: Brief Exercises...Ch. 15 - Lease classification LO151, LO152 Corinth Co....Ch. 15 - Lessee and lessor; calculate interest;...Ch. 15 - Finance lease; lessee; balance sheet effects ...Ch. 15 - Finance lease; lessee; income statement effects ...Ch. 15 - Sales-type lease; lessor; income statement effects...Ch. 15 - Prob. 15.7BECh. 15 - Operating lease LO154 (Note: Brief Exercises 8...Ch. 15 - Operating lease LO154 At the beginning of its...Ch. 15 - Short-term lease LO155 King Cones leased ice...Ch. 15 - Uncertain lease term LO156 Java Hut leased a...Ch. 15 - Uncertain lease payments LO156 On January 1,...Ch. 15 - Purchase option; lessor; sales-type lease LO152,...Ch. 15 - Residual value; sales-type lease LO152, LO153,...Ch. 15 - Guarantee d residual value LO156 On January 1,...Ch. 15 - Lessors initial direct costs; sales-type lease ...Ch. 15 - Lease classification LO151 Each of the four...Ch. 15 - Prob. 15.9ECh. 15 - Lessor calculation of annual lease payments;...Ch. 15 - Sales-type lease; lessor; income statement effects...Ch. 15 - Calculation of annual lease payments; residual...Ch. 15 - Lease concepts; finance/sales-type leases;...Ch. 15 - Calculation of annual lease payments; purchase...Ch. 15 - Prob. 15.37ECh. 15 - Prob. 15.38ECh. 15 - Prob. 15.39ECh. 15 - Lessors initial direct costs; operating and...Ch. 15 - Research Case 151 FASB codification; locate and...Ch. 15 - Ethics Case 153 Leasehold improvements LO153...Ch. 15 - Communication Case 155 Wheres the gain? Appendix...Ch. 15 - Prob. 15.6DMPCh. 15 - Prob. 1CCTCCh. 15 - Prob. 2CCTC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- What is the gross profit percentage for this periodarrow_forwardThe company's gross margin percentage is ?arrow_forwardProblem 19-13 (Algo) Shoney Video Concepts produces a line of video streaming servers that are linked to personal computers for storing movies. These devices have very fast access and large storage capacity. Shoney is trying to determine a production plan for the next 12 months. The main criterion for this plan is that the employment level is to be held constant over the period. Shoney is continuing in its R&D efforts to develop new applications and prefers not to cause any adverse feelings with the local workforce. For the same reason, all employees should put in full workweeks, even if that is not the lowest-cost alternative. The forecast for the next 12 months is MONTH FORECAST DEMAND January February March April 530 730 830 530 May June 330 230 July 130 August 130 September 230 October 630 730 800 November December Manufacturing cost is $210 per server, equally divided between materials and labor. Inventory storage cost is $4 per unit per month and is assigned based on the ending…arrow_forward

- Compute 007s gross profit percentage and rate of inventory turnover for 2016arrow_forwardHeadland Company pays its office employee payroll weekly. Below is a partial list of employees and their payroll data for August. Because August is their vacation period, vacation pay is also listed. Earnings to Weekly Vacation Pay to Be Employee July 31 Pay Received in August Mark Hamill $5,180 $280 Karen Robbins 4,480 230 $460 Brent Kirk 3,680 190 380 Alec Guinness 8,380 330 Ken Sprouse 8,980 410 820 Assume that the federal income tax withheld is 10% of wages. Union dues withheld are 2% of wages. Vacations are taken the second and third weeks of August by Robbins, Kirk, and Sprouse. The state unemployment tax rate is 2.5% and the federal is 0.8%, both on a $7,000 maximum. The FICA rate is 7.65% on employee and employer on a maximum of $142,800 per employee. In addition, a 1.45% rate is charged both employer and employee for an employee's wages in excess of $142,800. Make the journal entries necessary for each of the four August payrolls. The entries for the payroll and for the…arrow_forwardThe direct materials variance is computed when the materials are purchasedarrow_forward

- Compute the assets turnover ratioarrow_forwardExercise 5-18 (Algo) Calculate receivables ratios (LO5-8) Below are amounts (in millions) from three companies' annual reports. WalCo TarMart Costbet Beginning Accounts Receivable $1,795 6,066 609 Ending Accounts Receivable $2,742 6,594 645 Net Sales $320,427 65,878 66,963 Required: 1. Calculate the receivables turnover ratio and the average collection period for WalCo, TarMart and CostGet 2. Which company appears most efficient in collecting cash from sales? Complete this question by entering your answers in the tabs below. Required 1 Required C Calculate the receivables turnover ratio and the average collection period for WalCo, TarMart and CostGet. (Enter your answers in millions rounded to 1 decimal place.) Receivables Turnover Ratio: WalCo S TarMart. S CostGet S Choose Numerator Choose Numerator "ValCo FarMart CostGet 320,427 $ 65.878 66,963 Choose Denominator Receivables turnover ratio 2,742.0 116.9 times 0 times 0 times Average Collection Period Choose Denominator Average…arrow_forwardWhat is the Whistleblower Protection Act of 1989 (amended in 2011)?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education

Accounting for Finance and Operating Leases | U.S. GAAP CPA Exams; Author: Maxwell CPA Review;https://www.youtube.com/watch?v=iMSaxzIqH9s;License: Standard Youtube License