Videos

Evaluate Performance Evaluation System: Behavioral Issues

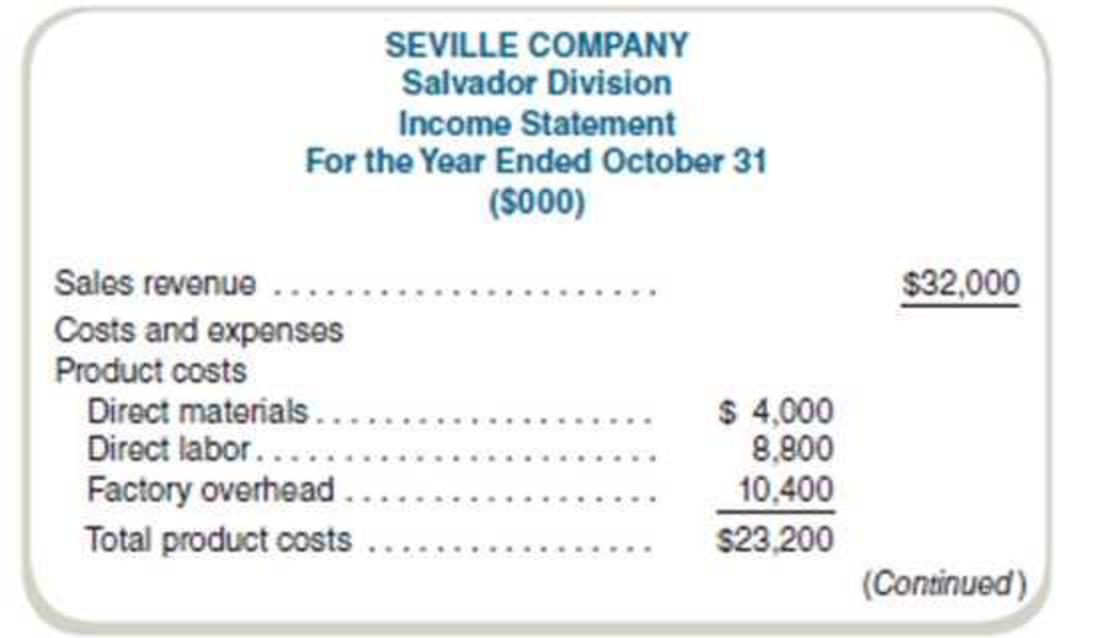

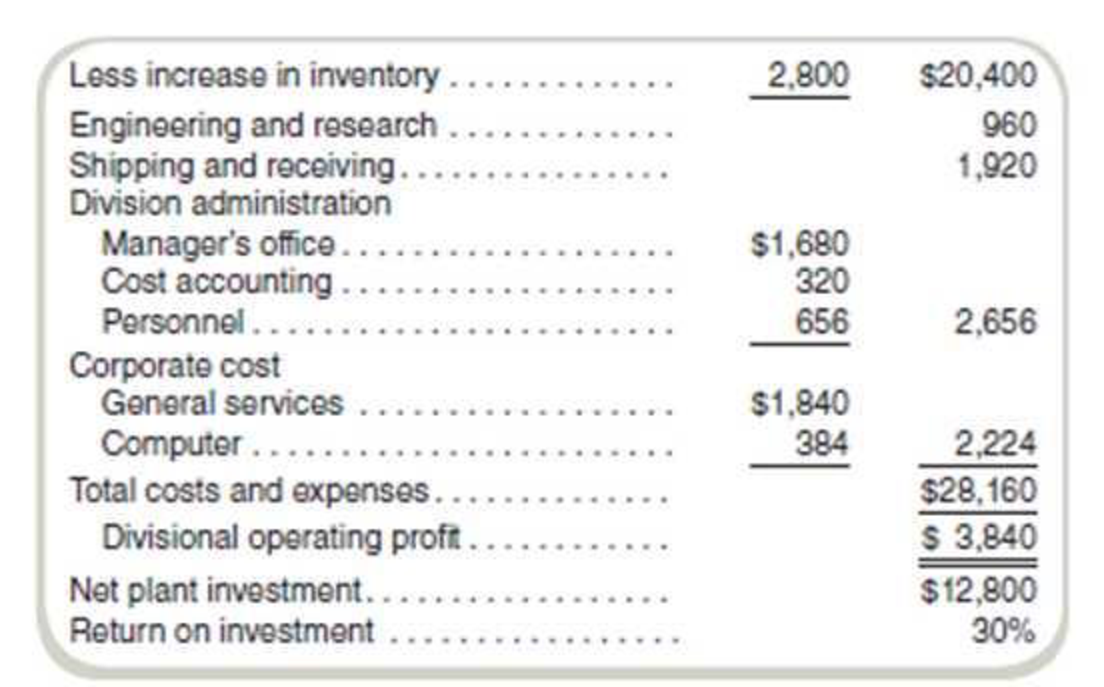

Several years ago, Seville Company acquired Salvador Components. Prior to the acquisition, Salvador manufactured and sold automotive components to third-party customers. Since becoming a division of Seville, Salvador has manufactured components only for products made by Seville’s Luxo Division.

Seville’s corporate management gives the Salvador Division management considerable latitude in running the division’s operations. However, corporate management retains authority for decisions regarding capital investments, product pricing, and production quantities.

Seville has a formal performance evaluation program for all division managements. The evaluation program relies substantially on each division’s

The corporate accounting staff prepares the divisional financial statements. Corporate general services costs are allocated on the basis of sales dollars, and the computer department’s actual costs are apportioned among the divisions on the basis of use. The net divisional investment includes divisional fixed assets at net book value (cost less

Required

- a. Discuss Seville Company’s financial reporting and performance evaluation program as it relates to the responsibilities of Salvador Division.

- b. Based on your response to requirement (a), recommend appropriate revisions of the financial information and reports used to evaluate the performance of Salvador’s divisional management. If revisions are not necessary, explain why.

(CM A adapted)

Want to see the full answer?

Check out a sample textbook solution

Chapter 14 Solutions

FUNDAMENTALS OF COST ACCOUNTING IA

- Phoenix Inc., a cellular communication company, has multiple business units, organized as divisions. Each division’s management is compensated based on the division’s operating income. Division A currently purchases cellular equipment from outside markets and uses it to produce communication systems. Division B produces similar cellular equipment that it sells to outside customers—but not to division A at this time. Division A’s manager approaches division B’s manager with a proposal to buy the equipment from division B. If it produces the cellular equipment that division A desires, division B will incur variable manufacturing costs of $60 per unit. Relevant Information about Division B Sells 90,000 units of equipment to outside customers at $130 per unit Operating capacity is currently 80%; the division can operate at 100% Variable manufacturing costs are $70 per unit Variable marketing costs are $8 per unit Fixed manufacturing costs are $900,000 Income per Unit for Division A…arrow_forwardCorcoran Heavy Industries Company (CHIC) is organized into four divisions, each of which operates in a different industry. The types of customer served and the method used to distribute products differ across all four of these industries. In addition, each division must comply with its own unique set of industry regulations related to issues such as safety and recyclability of materials.Operating profit before depreciation and amortization is the measure of profit regularly used by the chief operating decision maker for evaluating the performance of each of these divisions. In addition, information for each division on capital expenditures and depreciation and amortization is routinely provided by corporate headquarters to the chief operating decision maker. A summary of the information provided to the chief operating decision maker at the end of the current year is as follows:Required I. Prepare a report for CHIC's management evaluating whether the operating segments disclosures…arrow_forwardSimon Forest Corporation operates two divisions, the Timber Division and the Consumer Division. The Timber Division manufactures and sells logs to paper manufacturers. The Consumer Division operates retail lumber mills which sell a variety of products in the do-it-yourself homeowner market. The company is considering disposing of the Consumer Division since it has been consistently unprofitable for a number of years. The income statements for the two divisions for the year ended December 31, 2002 are presented below: Timber Division Consumer Division Total Sales P1,500,000 P500,000 P2,000,000 Cost of goods sold 900,000 350.000 1.250.000 Gross profit Selling & admin expenses 600,000 150,000 750,000 250,000 180,000 430,000 Net income P 350,000 P(30,000) P 320,000 In the Consumer Division, 70% of the cost of goods sold are variable costs and 30% of selling and administrative expenses are variable costs. The management of the company feels it can save P60,000 of fixed cost of goods sold…arrow_forward

- n addition to an incremental analysis, qualitative factors should be included in an business situation analysis. 1. A diversified food company is considering the closing of its condiment division. What qualitative factors should be considered before discontinuing a division or product line? 2. An automobile manufacturer has decided to allow outside suppliers to bid on all parts necessary to make its vehicles. What qualitative factors should be considered by management in deciding whether or not to turn over the production of a part to an outside supplier?arrow_forwardMaxwell Company produces a variety of kitchen appliances, including cooking ranges and dishwashers. Over the past several years, competition has intensified. In order to maintainand perhaps increaseits market share, Maxwells management decided that the overall quality of its products had to be increased. Furthermore, costs needed to be reduced so that the selling prices of its products could be reduced. After some investigation, Maxwell concluded that many of its problems could be traced to the unreliability of the parts that were purchased from outside suppliers. Many of these components failed to work as intended, causing performance problems. Over the years, the company had increased its inspection activity of the final products. If a problem could be detected internally, then it was usually possible to rework the appliance so that the desired performance was achieved. Management also had increased its warranty coverage; warranty work had been increasing over the years. David Haight, president of Maxwell Company, called a meeting with his executive committee. Lee Linsenmeyer, chief engineer; Kit Applegate, controller; and Jeannie Mitchell, purchasing manager, were all in attendance. How to improve the companys competitive position was the meetings topic. The conversation of the meeting was recorded as seen on the following page: DAVID: We need to find a way to improve the quality of our products and at the same time reduce costs. Lee, you said that you have done some research in this area. Would you share your findings? LEE: As you know, a major source of our quality problems relates to the poor quality of the parts we acquire from the outside. We have a lot of different parts, and this adds to the complexity of the problem. What I thought would be helpful would be to redesign our products so that they can use as many interchangeable parts as possible. This will cut down the number of different parts, make it easier to inspect, and cheaper to repair when it comes to warranty work. My engineering staff has already come up with some new designs that will do this for us. JEANNIE: I like this idea. It will simplify the purchasing activity significantly. With fewer parts, I can envision some significant savings for my area. Lee has shown me the designs so I know exactly what parts would be needed. I also have a suggestion. We need to embark on a supplier evaluation program. We have too many suppliers. By reducing the number of different parts, we will need fewer suppliers. And we really dont need to use all the suppliers that produce the parts demanded by the new designs. We should pick suppliers that will work with us and provide the quality of parts that we need. I have done some preliminary research and have identified five suppliers that seem willing to work with us and assure us of the quality we need. Lee may need to send some of his engineers into their plants to make sure that they can do what they are claiming. DAVID: This sounds promising. Kit, can you look over the proposals and their estimates and give us some idea if this approach will save us any money? And if so, how much can we expect to save? KIT: Actually, I am ahead of the game here. Lee and Jeannie have both been in contact with me and have provided me with some estimates on how these actions would affect different activities. I have prepared a handout that includes an activity table revealing what I think are the key activities affected. I have also assembled some tentative information about activity costs. The table gives the current demand and the expected demand after the changes are implemented. With this information, we should be able to assess the expected cost savings. Additionally, the following activity cost data are provided: Purchasing parts: Variable activity cost: 30 per part number; 20 salaried clerks, each earning a 45,000 annual salary. Each clerk is capable of processing orders associated with 100 part numbers. Inspecting parts: Twenty-five inspectors, each earning a salary of 40,000 per year. Each inspector is capable of 2,000 hours of inspection. Reworking products: Variable activity cost: 25 per unit reworked (labor and parts). Warranty: Twenty repair agents, each paid a salary of 35,000 per year. Each repair agent is capable of repairing 500 units per year. Variable activity costs: 15 per product repaired. Required: 1. Compute the total savings possible as reflected by Kits handout. Assume that resource spending is reduced where possible. 2. Explain how redesign and supplier evaluation are linked to the savings computed in Requirement 1. Discuss the importance of recognizing and exploiting internal and external linkages. 3. Identify the organizational and operational activities involved in the strategy being considered by Maxwell Company. What is the relationship between organizational and operational activities?arrow_forwardPosavek is a wholesale supplier of building supplies building contractors, hardware stores, and home-improvement centers in the Boston metropolitan area. Over the years, Posavek has expanded its operations to serve customers across the nation and now employs over 200 people as technical representatives, buyers, warehouse workers, and sales and office staff. Most recently, Posavek has experienced fierce competition from the large online discount stores. In addition, the company is suffering from operational inefficiencies related to its archaic information system. Posavek revenue cycle procedures are described in the following paragraphs. Revenue Cycle Posaveks sales department representatives receive orders via traditional mail, e-mail, telephone, and the occasional walk-in customer. Because Posavek is a wholesaler, the vast majority of its business is conducted on a credit basis. The process begins in the sales department, where the sales clerk enters the customers order into the centralized computer sales order system. The computer and file server are housed in Posaveks small data processing department. If the customer has done business with Posavek in the past, his or her data are already on file. If the customer is a first-time buyer, however, the clerk creates a new record in the customer account file. The system then creates a record of the transaction in the open sales order file. When the order is entered, an electronic copy of it is sent to the customers e-mail address as confirmation. A clerk in the warehouse department periodically reviews the open sales order file from a terminal and prints two copies of a stock release document for each new sale, which he uses to pick the items sold from the shelves. The warehouse clerk sends one copy of the stock release to the sales department and the second copy, along with the goods, to the shipping department. The warehouse clerk then updates the inventory subsidiary file to reflect the items and quantities shipped. Upon receipt of the stock release document, the sales clerk accesses the open sales order file from a terminal, closes the sales order, and files the stock release document in the sales department. The sales order system automatically posts these transactions to the sales, inventory control, and cost-of-goods-sold accounts in the general ledger file. Upon receipt of the goods and the stock release, the shipping department clerk prepares the goods for shipment to the customer. The clerk prepares three copies of the bill of lading. Two of these go with the goods to the carrier and the third, along with the stock release document, is filed in the shipping department. The billing department clerk reviews the closed sales orders from a terminal and prepares two copies of the sales invoice. One copy is mailed to the customer, and the other is filed in the billing department. The clerk then creates a new record in the accounts receivable subsidiary file. The sales order system automatically updates the accounts receivable control account in the general ledger file. CASH RECEIPTS PROCEDURES Mail room clerks open customer cash receipts, reviews the check and remittance advices for completeness, and prepares two copies of a remittance list. One copy is sent with the checks to the cash receipts department. The second copy of the remittance advices are sent to the billing department. When the cash receipts clerk receives the checks and remittance list, he verifies the checks received against those on the remittance list and signs the checks For Deposit Only. Once the checks are endorsed, he records the receipts in the cash receipts journal from his terminal. The clerk then fills out a deposit slip and deposits the checks in the bank. Upon receipt of the remittances, the billing department clerk records the amounts in the accounts receivable subsidiary ledger from the department terminal. The system automatically updates the AR control account in the general ledger Posavek has hired your public accounting firm to review its sales order procedures for internal control compliance and to make recommendations for changes. Required a. Create a data flow diagram of the current system. b. Create a system flowchart of the existing system. c. Analyze the physical internal control weaknesses in the system. d. (Optional) Prepare a system flowchart of a redesigned computer-based system that resolves the control weaknesses that you identified. Explain your solution.arrow_forward

- Trump Forest Corporation operates two divisions, the Timber Division and the Consumer Division. The Timber Division manufactures and sells logs to paper manufacturers. The Consumer Division operates retail lumber mills which sell a variety of products in the do-it-yourself homeowner market. The company is considering disposing of the Consumer Division since it has been consistently unprofitable for a number of years. The income statements for the two divisions for the year ended December 31, 2019 are presented below: Timber Division Consumer Division Total Sales $1,500,000 $500,000 $2,000,000 Cost of goods sold 900,000 350,000…arrow_forwardMaxwell Company produces a variety of kitchen appliances, including cooking ranges and dishwashers. Over the past several years, competition has intensified. In order to maintain—and perhaps increase—its market share, Maxwell’s management decided that the overall quality of its products had to be increased. Furthermore, costs needed to be reduced so that the selling prices of its products could be reduced. After some investigation, Maxwell concluded that many of its problems could be traced to the unreliability of the parts that were purchased from outside suppliers. Many of these components failed to work as intended, causing performance problems. Over the years, the company had increased its inspection activity of the final products. If a problem could be detected internally, then it was usually possible to rework the appliance so that the desired performance was achieved. Management also had increased its warranty coverage; warranty work had been increasing over the years. DAVID…arrow_forwardEmpire Records divides its operations into three divisions. The company CEO noticed that its North American division is under performing and is trying to decide if this division should be eliminated. A recent income statement for its North American division is as follows: Empire Records North American Division Income Statement Revenue Divisions sales commissions Salary of the division president Lease cost for division retail stores Allocation of company-wide legal cost* Net loss *This cost relates to a legal settlement paid by Empire Records during the year. Required: a. Prepare an income statement containing only the relevant information to the segment elimination decision. b. Based on the income statement you prepared in Requirement a, should this division be eliminated? Complete this question by entering your answers in the tabs below. Required A Required B $570,000 (353,000) (25,700) (119,000) (77,000) (4,700) Prepare an income statement containing only the relevant information to…arrow_forward

- Bisbee Health Products invests heavily in research and development (R&D), although it must currently treat its R&D expenditures as expenses for financial accounting purposes. To encourage investment in R&D, Bisbee evaluates its division managers using EVA. The company adjusts accounting income for R&D expenditures by assuming these expenditures create assets with a two-year life. That is, the R&D expenditures are capitalized and then amortized over two years. Western Division of Bisbee shows after-tax income of $8.4 million for year 2. R&D expenditures in year 1 amounted to $3.8 million and in year 2, R&D expenditures were $4.9 million. For purposes of computing EVA, Bisbee assumes all R&D expenditures are made at the beginning of the year. Before adjusting for R&D, Western Division shows assets of $30.6 million at the beginning of year 2 and current liabilities of $680,000. Bisbee computes EVA using divisional investment at the beginning of the year and a 14 percent cost of capital.…arrow_forwardStandard-setting process Canada Printing Group, Inc. (CPGI), has recentlybegun the process of acquiring small to medium-size local and regional printing firms across the country to facilitate its corporate strategy of becoming the low-cost provider of graphic arts and printing services in Canada. To emphasize the importance of cost control, CPGI uses a standard cost system in all of its printing plants. Most of the smaller firms that CPGI has acquired have never used a standard cost system before. Therefore, when CPGI acquires a new printing plant, its first task is to evaluate the operation and set standards for the printing presses. One such recent acquisition was Pierre’s Lithographing of Montreal. Pierre has a five-year-old, 40-inch, four-color press that is in very good condition. Specifications provided by the manufacturer of the press indicate that under ideal conditions, the press should be able to produce 10,000 impressions per hour. CPGI has many similar presses throughout…arrow_forwardGemma Company is a midsize manufacturing company with 120 employees and approximately $45 million in sales. Management has established a set of processes to purchase fixed assets, described in the following paragraphs: When a user department decides to purchase a new fixed asset, the departmental manager prepares an asset request form. When completing the form, the manager must describe the fixed asset, the advantages or efficiencies offered by the asset, and estimates of costs and benefits. The asset request form is forwarded to the director of finance. Personnel in the finance department review estimates of costs and benefits and revise these if necessary. A discounted cash flow analysis is prepared and forwarded to the vice president of operations, who reviews the asset request forms and the discounted cash flow analysis, and then interviews user department managers if he or she feels it is warranted. After this review, she selects assets to purchase until she has exhausted the…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,