a)

Prepare a report for the chair of the allocation committee indicating the extent to which BRC’s financial situation has improved or worsened.

a)

Explanation of Solution

Not-for-profit (NFP) entities: It is an individual or group of people who work together to attain the goals and mission that is something other than making profit for its shareholders or owners. Not-for-profit entities’ success is measured by how much the entity serves to the well-being of public or poor people with the available resource of the entity.

Prepare a report for the chair of the allocation committee indicating the extent to which BRC’s financial situation has improved or worsened:

Report

To: Chair of allocation committee

UW allocation panel

From: Person X,

Financial advisor

Subject: Analysis of the rehabilitative camp funding for fiscal year 2021.

It is recalled to the panel members that it is quite concerned about the financial reserves. It is because the financial reserves are precariously low during the evaluation of the organization for fiscal year 2020. At that time, the financial advisor Person X raised the issue about ability of the organization to continue to sustain its function/program within the budgeted level. Further, he recommended the request of budget from UW might be cut by 50% until the improvement of financial position.

It is also noted from the statement of activities of fiscal year 2019; only 57% of the total expenses were spent for the program/function. The entire panel further decided to send a message about concerns of the organization and request the budget amount from $5,000 to $25,000 to the board. Based on this request the UW board has approved the fund.

During the meeting conducted in the last year, the Chairman and Director of the board promised to take immediate steps to improve the financial condition of the camp. It including more fund-raising activities and if required for reducing the cost, cutting the camp’s support staff.

It is very surprised and pleased by the proof that shows the improvement made in the organizations financial situation. After the inspection of statements and budgets of 2020, it is noted that there is a doubtful reduction of $31,934 in the investments amount. The camp has been carrying this amount (that is restricted for building expansion) for few years. However, in the temporarily restricted net assets, the exact amount has been decreased.

It is to be noted that there was no increase in the building account balance. In building account, the only change is decrease in balance due to depreciation of $7,240. It is the evidence for the money removed from the restricted investments. This money is used to boost the unrestricted financial reserves of the camp.

After identifying the apparent fund transfer, person X contacted director of the camp who provides the details about the donor. For the future building expansion, the donor has contributed $100,000 several years ago. The donor was no longer living and not able to locate the written agreement about this contribution.

Further, these facts have been reported to the board of directors. Directors passed resolution to authorize the use of investment of $37,500 for unrestricted purposes in the fiscal year 2020. Here, it is stated that the additional fund will be transferred in the future years if requirement arises.

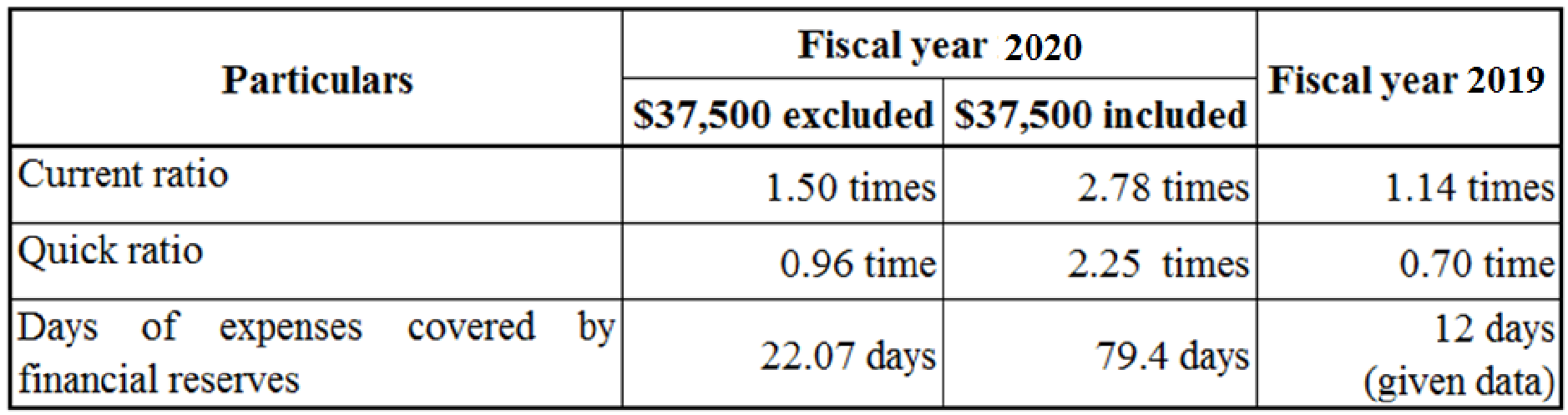

Hence, the panel members would like to see the impact of the transfer of $37,500 in the financial position of the camp. The following are the key calculations including and excluding the amount of $37,500.

Table (1)

This comparison clearly shows the difference between inclusion and exclusion of $37,500 in the assets. Based on this fact, the following recommendation is provided. UW’s attorney should look into the matter why the restricted resources used as unrestricted operation purpose of the camp.

Regards,

Person X,

Financial advisor

Notes for the above table:

a. Calculate current ratio:

It is given that the current asset is $43,589 and current liability is $29,141 for the fiscal year 2020. The current ratio is calculated by dividing the current assets by the current liabilities.

Hence, the current ratio exclusion of $37,500 is 1.50 times.

If add the amount of $37,500, the ratio will be:

Hence, the current ratio inclusion of $37,500 is 2.78 times.

Now, calculate current ratio for the fiscal year 2019:

It is given that the current asset is $46,368 and current liability is $40,786 for the fiscal year 2019.

Hence, current ratio for the year 2019 is 1.14 times.

b. Calculate quick ratio:

It is calculated by dividing the difference between the current assets and prepaid expenses by the current liabilities. It is given the prepaid expenses of 2020 is 15,559 and 2019 is $17,748.

Hence, the quick ratio exclusion of $37,500 is 0.96 times.

If add the amount of $37,500, the ratio will be:

Hence, the quick ratio inclusion of $37,500 is 2.25 times.

Now, calculate quick ratio for the fiscal year 2019:

It is given that the current asset is $46,368 and current liability is $40,786 for the fiscal year 2019.

Hence, the quick ratio for 2019 is 0.70 times.

c. Calculate days of expenses covered by financial reserves:

It is calculated by dividing the difference between the current assets and current liability by the total expenses. It is given that the total expenses are $238,932.

Hence, the quick ratio (exclusion of $37,500) is 22.07 days.

Now, calculated quick ratio for inclusion of $37,500:

Hence, the quick ratio (inclusion of $37,500) is 79.4 days.

b)

Explain the reaction of financial advisor to the board of director’s decision to use, for operating purposes, the $100,000 temporarily restricted net assets provided by a donor for building expansion.

b)

Explanation of Solution

Using the restricted fund of the donor contributed for the future building expansion as an unrestricted fund for the operation is not an ethical activity. There is a transfer of funds from one account to another without any approvals. This is a questionable activity. If it is identified that the Chairman and the board of directors had illegally transferred the restricted fund to operation activities, legal charges should have filed against them.

c)

Identify the amount of UW funds would the financial advisor recommend be allocated to the BRC for the fiscal year 2021.

c)

Explanation of Solution

The donor’s restricted fund contributed for the future building expansion should be allocated if there is any requirement for the expansion of the building. Otherwise, this fund should be restricted further and must not be allocated for operating purposes. It is illegal to use restricted funds for operation purposes.

The restricted fund balance should be audited every year-end. If the fund is spent for particular purpose it should be verified whether fund is used for donor’s mentioned contributed purpose. Otherwise, the fund should be recovered and it must be added to the restricted fund balance.

Want to see more full solutions like this?

Chapter 14 Solutions

ACCT GOV.+NFP ENTITIES LOOSELEAF W/CONN.

- For each of the following events or transactions, identity the fund that will be affected. JA city government pays the final contract retained percentage for JA county government establishes an investment pool to manage the A County government receives a large contribution specifying that income from the contribution be distributed each year to the county zoo. The principal is to remain intact indefinitely A county government levies real property taxes on behalf of the county and its municipalities JA central purchasing department was established to handle all the Paid the interest of general bonds Collections the pension of administrative employees of governmenal entity A Permanent Funds B. Internal Services Funds C. Debt Services Funds D Pension Trust Funds E Capital Proyect Funds F General Funds G. Trust Fundsarrow_forwardFor each of the following events or transactions, prepare the necessacry journal entries and identify the fund or funds that will be affected. 1. A governmental unit collects fees totaling $4,500 at the municipal pool. The fees are charged to recover costs of pool operation and maintenance 2. A county government that serves as a tax collection agency for all towns and cities located within the county collects county sales taxes totaling $125,000 for the month. 3. A $1,000,000 bond offering was issued, with a premium of $50,000, to subsidize the construction of a city visitor center. 4. A town receives a donation of $50,000 in bonds. The bonds should be held indefinitely, but bond income is to be donated to the local zoo. The zoo is associated with the town. 5. A central printing shop is established with a $150,000 nonreciprocal transfer from the general fund. 6. A $1,000,000 revenue bond offering was issued at par by a fund that provides water and sewer services to…arrow_forwardRequired information [The following information applies to the questions displayed below.] The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2024, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals Debits Adjustments: $ 29,400 53,000 VILLAGE OF SEASIDE PINES ENTERPRISE FUND Reconciliation of Operating Income to Net Cash Provided by Operating Activities For the year ended December 31, 2024 722,000 98,000 504,000 51,000 17,700 40,900 19,700 $ 1,535,700 Credits $ 112,000 32,600 51,000…arrow_forward

- For each of the following events or transactions, prepare the necessacry journal entries and identify the fund or funds that will be affected. 1. A governmental unit collects fees totaling $4,500 at the municipal pool. The fees are charged to recover costs of pool operation and maintenance 2. A county government that serves as a tax collection agency for all towns and cities located within the county collects county sales taxes totaling $125,000 for the month. 3. A $1,000,000 bond offering was issued, with a premium of $50,000, to subsidize the construction of a city visitor center. 4. A town receives a donation of $50,000 in bonds. The bonds should be held indefinitely, but bond income is to be donated to the local zoo. The zoo is associated with the town. 5. A central printing shop is established with a $150,000 nonreciprocal transfer from the general fund. 6. A $1,000,000 revenue bond offering was issued at par by a fund that provides water and sewer services to…arrow_forward! Required information [The following information applies to the questions displayed below.] The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2024, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals Required A Required B Complete this question by entering your answers in the tabs below. Required C VILLAGE OF SEASIDE PINES ENTERPRISE FUND Statement of Net Position December 31, 2024 Net Position: Net Investment in Capital Assets Unrestricted Total Net Position Debits Required: a.…arrow_forward[The following information applies to the questions displayed below.]The Township of Thomasville’s General Fund has the following net resources at year end: $69,000 of prepaid insurance $410,000 rainy day fund approved by the township governing board with specific conditions for its use $1,800 of supplies inventory $60,000 state grant for snow removal $150,000 contractual obligations for the purchase of equipment Outstanding encumbrance of $105,000 for the purchase of furniture & fixtures (assume no contractual obligation) Total Fund Balance is $1,010,500 What would be the total Nonspendable fund balance? Multiple Choice $70,800 $150,000 $69,000 $410,500 What would be the total Restricted fund balance? Multiple Choice $60,000 $150,000 $479,000 $410,000arrow_forward

- [The following information applies to the questions displayed below.]The Township of Thomasville’s General Fund has the following net resources at year end: $69,000 of prepaid insurance $410,000 rainy day fund approved by the township governing board with specific conditions for its use $1,800 of supplies inventory $60,000 state grant for snow removal $150,000 contractual obligations for the purchase of equipment Outstanding encumbrance of $105,000 for the purchase of furniture & fixtures (assume no contractual obligation) Total Fund Balance is $1,010,500 What would be the total Committed fund balance? Multiple Choice $410,000 $210,000 $560,000 $562,500 What would be the total Assigned fund balance? Multiple Choice $129,000 $165,000 $315,000 $105,000arrow_forward- Prepare journal entries in the Capital Projects Fund to record the following transactions related to the construction of a building by the Village of Navajo Falls. (Note that only Capital Projects Fund journal entries are required.) The Village adopts a formal budget and uses encumbrance accounting. a. The Village Council adopts a capital budget at the beginning of the year. To finance construction of the building, the Village will transfer $3 million from its General Fund and apply for a state grant of $1 million. It appropriates $4 million for construction. b. The General Fund transfers $3 million to the Capital Projects Fund for the new project. c. The state approves Navajo Falls's application for a $1 million construction grant and simultaneously sends a check to the Village. The grant is expenditure driven and thus requires that Navajo Falls incur qualifying expenditures. d. Navajo Falls awards a construction contract in the amount of $3.4 million. e. The…arrow_forward2. The City of Katerah maintains its books and records in a manner that facilitates the preparation of fund financial statements. Prepare all necessary journal entries to record the city’s revenues from the following transactions for the year ended December 31, 2017. a.) On January 15, the city received notification that it had been awarded a $300,000 federal grant to assist in the operation of its “Meals on Wheels” program. The federal government expects to send the cash in about three months. This is not a reimbursement type grant and all eligibility requirements have been met. b.) In February the city spent $31,000 on “Meals on Wheels.” c.) In March, fines of $1,800 were issued for parking tickets. Payment must be made within 30 days, when the city has an enforceable legal claim to the amounts. d.) In April, the city received the $300,000 grant from the federal government. e.) In April, the city received $1,200 cash in payment of parking tickets issued in March. In addition, $100 of…arrow_forward

- The following events relate to Habitat for Humanity International's activities. If appropriate, assume a discount rate of 3 percent per annum. Expenditures for house building activities are categorized as program expense. Need Part b. answer. 6. A donor contributes $15,000 in cash and signs an agreement to contribute $15,000 at the beginning of each of the next four years, to support specific Habitat for Humanity projects. a. Contribution received now Amount $ 15,000✔ Classification: Net assets without donor restrictions Amount $ x Classification: Net assets with donor restrictions Recorded? Yes b. Contributions received the next four years Recorded? Yes ◆arrow_forwardUrban Hospice (UH) is a not-for-profit organization. It receives some funding from the government, but most of its funding comes from donations and bequests. It uses the deferral method to account for contributions and an encumbrance system to control expenditures. For simplicity, UH accounts for all of its activities through an operations fund. UH has provided the following selected transactions for the current year: a. At the beginning of the year, UH unexpectedly received $1,000,000 from the government to purchase three monitoring machines. UH immediately purchased the machines. Since UH purchased the machines as soon as the funds were received, it did not prepare a purchase order for them. At the end of the year, UH took depreciation of $200,000 on the machines. b. UH's annual Christmas fundraising gala generated $3,011,000 in cash and $820,000 in pledges. Based on previous years' experiences, UH estimates that 85 percent of the pledges will be collected in the first three months…arrow_forward4. The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2020, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund. Accounts payable Accounts receivable Accrued interest payable Accumulated depreciation Administrative and selling expenses Allowance for uncollectible accounts Capital assets Cash Charges for sales and services Cost of sales and services Depreciation expense Due from General Fund Interest expense Interest revenue Transfer in from General Fund Bank note payable Supplies inventory Totals Debits $32,000 47,000 712,000 89,000 479,000 45,000 17,000 40,000 18,000 $1,479,000 Credits $ 96,000 28,000 45,000 12,000 550,000 4,000 119,000 625,000 $1,479,000 Required: a. Prepare the closing entries for December 31. b. Prepare the Statement of Revenues, Expenses, and Changes in Fund Net Position for the year ended December 31. c. Prepare the Net Position section of the…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education