Cornerstones of Cost Management (Cornerstones Series)

4th Edition

ISBN: 9781305970663

Author: Don R. Hansen, Maryanne M. Mowen

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 13, Problem 25P

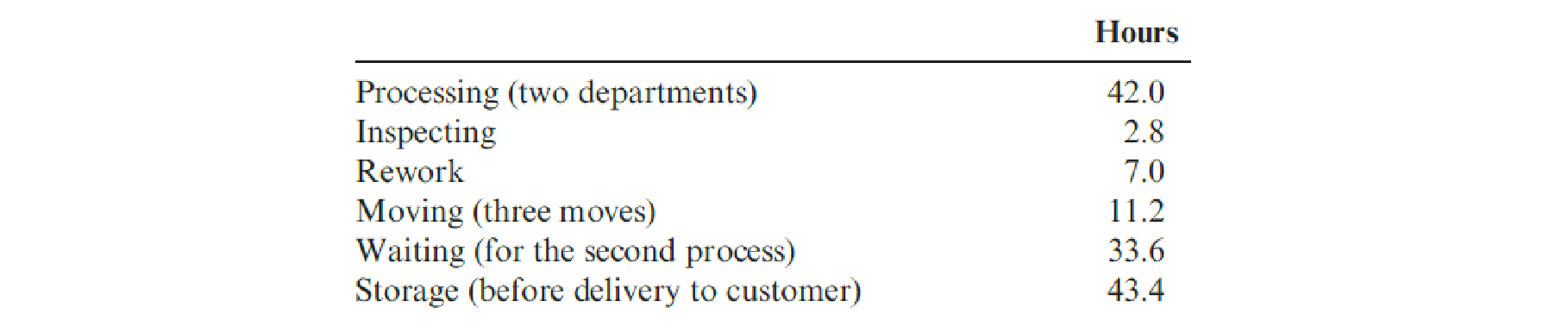

Auflegger, Inc., manufactures a product that experiences the following activities (and times):

Required:

- 1. Compute the MCE for this product.

- 2. A study lists the following root causes of the inefficiencies: poor quality components from suppliers, lack of skilled workers, and plant layout. Suggest a possible cost reduction strategy, expressed as a series of if-then statements that will reduce MCE and lower costs. Finally, prepare a strategy map that illustrates the causal paths. In preparing the map, use only three perspectives: learning and growth, process, and financial.

- 3. Is MCE a lag or a lead measure? If and when MCE acts as a lag measure, what lead measures would affect it?

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

ABC systems get more accurate as more activities are identified and analyzed. Critique the following statement: “A company should look to break its production process into as many activities as possible in order to determine the most accurate unit costs possible”. Why do you agree or disagree with that statement? Give several reasons.

a) CVP analysis help managers to take better decision. Justify with real life scenario. (b)Paste Corporation has established new plant for the production of new product called “Diazinon”. There are two different manufacturing methods available to produce Diazinon. Either by using a process or an order base method. The assembling technique won't influence the quality or deals of the item. The evaluated manufacturing expenses of the two strategies are as per the following:

Process base Order base

Variable manufacturing cost per unit..................... Rs14.00 Rs.17.60

Fixed manufacturing cost per year ......................Rs. 2,440,000 Rs. 1,320,000

The organization's statistical surveying office has suggested an initial selling cost of Rs.35 per unit for Diazinon. The yearly fixed selling and admin costs…

Can you provide samples/examples of tasks for developing the costing and profitability model for a new product? Should include the following:

o A table showing the list of the parameters used in your model

o A breakdown of the expected production costs and profitability

o Calculation of the NPV of expected sales/ profitability

o A sensitivity analysis that accounts for changes in any three (3) parameters of your model.

o At least two trade-off rules you developed for your product development

Chapter 13 Solutions

Cornerstones of Cost Management (Cornerstones Series)

Ch. 13 - Describe a strategic-based responsibility...Ch. 13 - What is a Balanced Scorecard?Ch. 13 - What is meant by balanced measures?Ch. 13 - Prob. 4DQCh. 13 - Prob. 5DQCh. 13 - What are stretch targets? What is their strategic...Ch. 13 - Prob. 7DQCh. 13 - What are the three strategic themes of the...Ch. 13 - Prob. 9DQCh. 13 - Explain what is meant by the long wave and the...

Ch. 13 - Prob. 11DQCh. 13 - Prob. 12DQCh. 13 - What is a testable strategy?Ch. 13 - Prob. 14DQCh. 13 - Prob. 15DQCh. 13 - Norton Company has the following data for one of...Ch. 13 - Craig, Inc., has provided the following...Ch. 13 - Prob. 3CECh. 13 - The following comment was made by the CEO of a...Ch. 13 - Prob. 5ECh. 13 - Prob. 6ECh. 13 - Consider the following list of scorecard measures:...Ch. 13 - Hatch Manufacturing produces multiple machine...Ch. 13 - Computador has a manufacturing plant in Des Moines...Ch. 13 - Refer to Exercise 13.9. Assume that the company...Ch. 13 - The following if-then statements were taken from a...Ch. 13 - Consider the following quality improvement...Ch. 13 - Bannister Company, an electronics firm, buys...Ch. 13 - Prob. 14ECh. 13 - In a balanced scorecard, a key strategic if-then...Ch. 13 - Which of the following objectives would be...Ch. 13 - A manufacturing cell produces 40 units in five...Ch. 13 - Which of the following objectives would likely be...Ch. 13 - Which of the following objectives would likely be...Ch. 13 - Carson Wellington, president of Mallory Plastics,...Ch. 13 - At the end of 20x1, Mejorar Company implemented a...Ch. 13 - Refer to the data in Problem 13.21. 1. Express...Ch. 13 - The following strategic objectives have been...Ch. 13 - Lander Parts, Inc., produces various automobile...Ch. 13 - Auflegger, Inc., manufactures a product that...Ch. 13 - Prob. 26PCh. 13 - At the beginning of the last quarter of 20x1,...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- The following series of statements or phrases are associated with product life-cycle viewpoints. Identify whether each one is associated with the marketing, production, or customer viewpoint. Where possible, identify the particular characteristic being described. If the statement or phrase fits more than one viewpoint, label it as interactive. Explain the interaction. a. Sales are increasing at an increasing rate. b. The cost of maintaining the product after it is purchased. c. The product is losing market acceptance and sales are beginning to decrease. d. A design is chosen to minimize post-purchase costs. e. Ninety percent or more of the costs are committed during the development stage. f. The length of time that the product serves the needs of a customer. g. All the costs associated with a product for its entire life cycle. h. The time in which a product generates revenue for a company. i. Profits tend to reach peak levels during this stage. j. Customers have the lowest price sensitivity during this stage. k. Describes the general sales pattern of a product as it passes through distinct life-cycle stages. l. The concern is with product performance and price. m. Actions taken so that life-cycle profits are maximized. n. Emphasizes internal activities that are needed to develop, produce, market, and service products.arrow_forwardRelyaTech Corporation manufactures a number of products at its highly automated factory. The products are very popular, with demand far exceeding the factory's capacity. To maximize profit, management should rank products based on their selling price gross margin contribution margin per unit of the constrained resource contribution marginarrow_forwardWhich of the following statements is false? (You may select more than one answer.)a. Activity-based costing systems usually shift costs from low-volume products tohigh-volume products.b. Benchmarking can be used to identify activities with the greatest potential forimprovement.c. Activity-based costing is most valuable to companies that manufacture products thatare similar in terms of their volume of production, batch size, and complexity.d. Activity-based costing systems are based on the assumption that the costs included ineach activity cost pool are strictly proportional to the cost pool’s activity measure.arrow_forward

- Question 2 A seminar was recently attended by the Managing Director of XYZ Manufacturing Company Limited located at Sheffield. The focus of the seminar was "optimising scarce resources utility in a manufacturing setting with particular reference to linear programming". On his return to his base, he called for a meeting with the Management to share his experience from the seminar and the impact this will have on the decision by the Board to produce two major products in the years ahead. A group of external research experts had previously been commissioned and the following represents information from the research carried out by them The expected products are "Best" and "Smart" with expected costs statistics as follows: Best £ £ Smart (3kg@£50/kg) Material costs (5kg@£50/kg) 250 150 Labour costs Machinery time 30 (4 hours @£15/Hr) 60 (4 hours @£10/hr) 40 (2hours @£15/Hr) (5hours@£10/Hr) Other Processing Time 50 The applicable pricing policy is based on total cost of production plus 20%…arrow_forwardPrepare a report from Mary Jane to Don explaining how these changes will affect Mirabel’s overall cost structure. For those changes that are controllable, make a recommendation considering the uncontrollable cost changes. Be certain to consider not only the company’s break-even point, but also the desired margin of safety.arrow_forward1) Which of the following is a reason that has accelerated the demand for refinements to the costing system? A) The declining demand for customized products has led managers to decrease the variety of products and services their companies offer. B) The use of product and process technology has led to an increase in indirect costs and a decrease in direct costs. C) The increased of automated processes has led to the increase in direct manufacturing cost leading to a decrease in breakeven point. D) The increasing competition in product markets has led to an increase in contribution margin resulting in a decrease of breakeven point.arrow_forward

- You have been asked by management to classify the costs associated with the start-up of this new product line. Using the cost information provided below, classify each cost under the appropriate heading according to the chart provided below. Note that some costs may be classified under more than one heading. For example, a cost may be a fixed cost and a period cost. Name of cost Variable Cost Fixed Cost Direct Materials Direct Labor Factory Overhead Period Cost Prime Cost Conversion Cost Carlson “New Product” Cost Information Cost Amount Cost Type Depreciation on Building (annual) $ 10,000 Direct Labor Cost (per unit) $ 75 Direct Materials Cost (per unit) $ 60 Factory Utilities (per unit) $ 8 Indirect Materials (per unit) $ 4 Interest on Investments (annual) $3,000 Machinery Rental (monthly) $ 6,000 Marketing (annual) $ 35,000 Rent from Tenant (annual) $40,000…arrow_forwardShatta movement LTD produces a single product. The company's directors want to explore new markets, and they require an accurate analysis of the firm's cost structure for both forecasting and pricing purpose. An attemp to provide this analysis from the aggregation of individual cost has produced a poor correspondence between actual and predicted cost. You are an accountant employee by Shatta Movement Ltd, and you have been asked to provide a statistical approach to the problem. The financial director has given you the following data: Period output (unit) average unit cost (GHS) July August September October November December 9,000 14,000 11,000 8,000 6,000 12,000 12.8 13 11.4 12 13 11.7 You obtain the following further information: 1. The cost from which the averages have been computed consist of the firm's entire cost for the relevant month. 2. Fixed coat can be assumed to be unaffected by seasonal factors except for harmattan heating. In July and August a…arrow_forwardClarke, Inc. manufactures door panels. Suppose Clarke, Inc. is considering spending the following amounts on a new total quality management (TQM) program: View the spending amounts. Clarke, Inc. expects the new program would save costs through the following: View the savings amounts. Requirements 1. Classify each cost as a prevention cost, an appraisal cost, an internal failure cost, or an external failure cost. 2. Should Clarke, Inc. implement the new quality program? Give your reason. Requirement 1. Classify each cost as a prevention cost, an appraisal cost, an internal failure cost, or an external failure cost. Type of Cost Strength-testing one item from each batch of panels Training employees in TQM Training suppliers in TQM Identifying suppliers who commit to on-time delivery of perfect-quality materials Lost profits from lost sales due to disappointed customers Rework and spoilage Inspection of raw materials Warranty costs Savings Avoid lost profits from lost sales due to…arrow_forward

- Because of high production-changeover time and costs, a director of manufacturing must convince management that a proposed manufacturing method reduces costs before the new method can be implemented. The current production method operates with a mean cost of $220 per hour. A research study will measure the cost of the new method over a sample production period. Develop the null and alternative hypotheses most appropriate for this study. Comment on the conclusion when H0 cannot be rejected. Comment on the conclusion when H0 can be rejected.arrow_forwardThe management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forwardContinuous improvement is the governing principle of a lean accounting system. Following are several performance measures. Some of these measures would be associated with a traditional standard-costing accounting system, and some would be associated with a lean accounting system. a. Materials price variances b. Cycle time c. Comparison of actual product costs with target costs d. Materials quantity or efficiency variances e. Comparison of actual product costs over time (trend reports) f. Comparison of actual overhead costs, item by item, with the corresponding budgeted costs g. Comparison of product costs with competitors product costs h. Percentage of on-time deliveries i. First-time through j. Reports of value- and non-value-added costs k. Labor efficiency variances l. Days of inventory m. Downtime n. Manufacturing cycle efficiency (MCE) o. Unused (available) capacity variance p. Labor rate variance q. Using a sister plants best practices as a performance standard Required: 1. Classify each measure as lean or traditional (standard costing). If traditional, discuss the measures limitations for a lean environment. If it is a lean measure, describe how the measure supports the objectives of lean manufacturing. 2. Classify the measures into operational (nonfinancial) and financial categories. Explain why operational measures are better for control at the shop level (production floor) than financial measures. Should any financial measures be used at the operational level? 3. Suggest some additional measures that you would like to see added to the list that would be supportive of lean objectives.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...

Statistics

ISBN:9781305627734

Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. Anderson

Publisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

Excel Applications for Accounting Principles

Accounting

ISBN:9781111581565

Author:Gaylord N. Smith

Publisher:Cengage Learning

Relevant Costing Explained; Author: Kaplan UK;https://www.youtube.com/watch?v=hnsh3hlJAkI;License: Standard Youtube License