Videos

Effect of Convertible Bonds on Earnings per Share

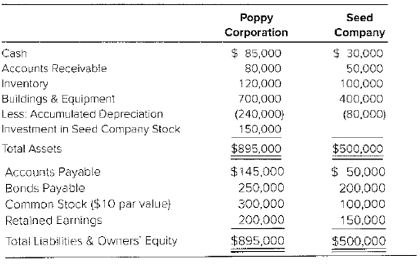

Poppy Corporation owns 60 percent of Seed Company’s common shares. Balance sheet data for the companies on December 31, 20X2, are as follows:

The bonds of Poppy Corporal ion and Seed Company pay annual interest of 8 percent and 10 percent, respectively. Poppy’s bonds are not convertible. Seeds bonds can be converted into 10,000 shares of its company stock any time after January 1, 20X1. An income tax rate of 40 percent is applicable to both companies. Seed reports net income of $30,000 for 20X2 and pays dividend of $15,000. Poppy reports income from its separate operations of $45,000 and pays dividends of $25,000.

Required

Compute basic and diluted EPS for the consolidated entity for 20X2.

Want to see the full answer?

Check out a sample textbook solution

Chapter 10 Solutions

Advanced Financial Accounting

- 1. On January 1, 20x1, an entity issues bonds with face amount of P5,000,000 for P5,200,000. The bonds mature on December 31, 20x3 and pay annual interest of 12%. The bonds can be converted into 10,000 ordinary shares of the entity with par value per share of P200. On January 1, 20x1, the bonds are selling at 101 without the conversion feature. The effective interest rate on the bonds is 11.59%. All of the bonds are converted into ordinary shares on January 1, 20x3. Requirement: Provide the entries to record the following: a.) issuance of the convertible bonds. b.) conversion of the bonds.arrow_forward10. Float Corporation had the following transactions pertaining to debt investments. Jan. 1 Purchased 100 8%, $1,000 Qaiz Co. bonds for $100,000 cash plus brokerage fees of $1,800. Interest is payable semiannually on July 1 and January 1. Received semiannual interest on Qaiz Co. bonds. Sold 60 Qaiz Co. bonds for $68,000 less $1,000 brokerage fees. July 1 July 1 Required: a) Journalize the transactions. b) Prepare the adjusting entry for the accrual of interest at December 31.arrow_forwardMae Jong Corp. issues $1,000,000 of 10% bonds payable which may be converted into 10,000 shares of $2 par value ordinary shares. The market rate of interest on similar bonds is 12%. Interest is payable annually on December 31, and the bonds were issued for total proceeds of $1,000,000. In accounting for these bonds, Mae Jong Corp. will: a. first assign a value to the equity component, then determine the liability component. b. assign no value to the equity component since the conversion privilege is not separable from the bond. c. first assign a value to the liability component based on the face amount of the bond. d. use the “with-and-without” method to value the compound instrument.arrow_forward

- On June 30, 2019, King Company had outstanding 9%, P5,000,000 face value bonds maturing on June 30, 2024. Interest is payable semiannually every June 30 and December 31. On June 30, 2019, after amortization was recorded for the period, the unamortized bond premium and bond issue cost were P30, 000 and P50, 000, respectively. On that date, King Company acquired all its outstanding bonds on the open market at 98 and retired them. On June 30, 2019, what amount should King Company recognize as gain before tax on redemption of bonds?arrow_forwardOn January 1, Year 1, Grow Company purchased P1,000,000 12% bonds of Glow Company for P1,063,394, a price that yields 10%. Interest on these bonds is payable every December 31. The bonds mature on December 31, Year 4. On April 1, Year 3, to pay a maturing obligation, Grow sold P600,000 face value bonds at 101 plus accrued interest. Market value of the bonds on different dates is as follows: December 31, Year 1 108 December 31, Year 2 106 December 31, Year 3 104 Required: Assume that the bonds were classified as debt investments at fair value through profit or loss. a) How much is interest income for the year ended December 31, Year 1? b) What amount of gain or loss should Grow report on the sale of the bond investments on April 1, Year 3? c) At what amount should the bond investments be shown on December 31, Year 2 and…arrow_forwardOn January 1, Cee Company's ordinary share capital amounted to P1,000,000, with P10 par value. On April 1, 2019, the entity issued P5,000,000, 10% bonds with a face value of P1,000. The bonds were converted on October 1, 2019 and 20 ordinary shares were issued in exchange for each bond. Net income was P10,000,000. The income tax rate is 30%. Requirement: 1. What is the amount of basic earnings per share? 2. What is is the amount of diluted earnings per share?arrow_forward

- On January 1, 20x1, Eduard Co. acquired 12%, P4,000,000 bonds for P4,198,948. The principal is due on December 31, 20x3 but interest is made annually starting December 31, 20x1. The effective interest rate on the bonds is 10%.13. How much is the interest income recognized in 20x1?a. 419,895b. 413,884c. 407,273d. 480,00014. How much is the carrying amount of the investment on December 31, 20x1?a. 4,198,948b. 4,138,843c. 4,072,727d. 4,000,000arrow_forwardAir Supply issued $6 million of 9%, 10-year convertible bonds at 101. The bonds are convertible into 24,000 shares of common stock. Bonds that are similar in all respects except that they are nonconvertible, currently are selling at 99 (that is, 99% of face amount). What amount should Air Supply record as equity and how much as a liability when the bonds are issued?arrow_forwardTrear Company has $80,000, 10%, 12 year convertible bonds outstanding. These bonds were sold at face value and pay semiannual interest on June 30 and December 31 of each year. The bonds are convertible into 40 shares of $5 par value common stock for each $1,000 par value bond. On December 31 after the bond interest has been paid, $20,000 par value bonds are converted. The market value of Trear's common stock was $38 per share. Instructions: prepare the necessary journal entry to record the conversion.arrow_forward

- On January 1, 2018, Gless Textiles issued $12 million of 9%, 10-year convertible bonds at 101. The bonds payinterest on June 30 and December 31. Each $1,000 bond is convertible into 40 shares of Gless’s no par commonstock. Bonds that are similar in all respects, except that they are nonconvertible, currently are selling at 99 (that is,99% of face amount). Century Services purchased 10% of the issue as an investment.Required:1. Prepare the journal entries for the issuance of the bonds by Gless and the purchase of the bond investment byCentury.2. Prepare the journal entries for the June 30, 2022, interest payment by both Gless and Century assuming bothuse the straight-line method.3. On July 1, 2023, when Gless’s common stock had a market price of $33 per share, Century converted thebonds it held. Prepare the journal entries by both Gless and Century for the conversion of the bonds (bookvalue method).arrow_forwardOn August 1 of the current year, Fleetwood Company purchased 5,000 , P1,000 , 12% bonds on Ritchie Company at 104 plus accrued interest . The bonds pay interest semiannually on May 1 and November 1. On December 1 of the current year, Fleetwood sold 2,000 of the bonds at 102 plus accrued interest. What is the gain or loss on sale of investment? indicate if gain or lossarrow_forwardThe following information relates to the debt securities investments of Sunland Company. 1. On February 1, the company purchased 10% bonds of Gibbons Co. having a par value of $324,000 at 100 plus accrued interest. Interest is payable April 1 and October 1. 2. On April 1, semiannual interest is received. 3. On July 1, 9% bonds of Sampson, Inc. were purchased. These bonds with a par value of $186,000 were purchased at 100 plus accrued interest. Interest dates are June 1 and December 1. 4. On September 1, bonds with a par value of $60,000, purchased on February 1, are sold at 99 plus accrued interest. 5. On October 1, semiannual interest is received. 6. On December 1, semiannual interest is received. 7. On December 31, the fair value of the bonds purchased February 1 and July 1 are 95 and 93, respectively. (a)Prepare any journal entries you consider necessary, including year-end entries (December 31), assuming these are available-for-sale securities.…arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning