Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

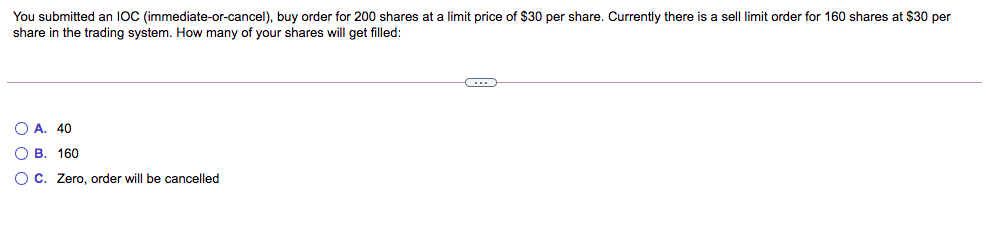

Transcribed Image Text:You submitted an 1OC (immediate-or-cancel), buy order for 200 shares at a limit price of $30 per share. Currently there is a sell limit order for 160 shares at $30 per

share in the trading system. How many of your shares will get filled:

O A. 40

O B. 160

O C. Zero, order will be cancelled

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Dhote 0e Librem. Close Save What is the rate of return when 30 shares of Stock A, purchased for $20/share, are sold for $720? The commission on the sale is $6. Rate of Return = [ ? ] % Give your answer as a percent rounded to the nearest tenth. Enter DAcellus Corporafion. All Rights Reserved.arrow_forwardYou buy a share of Stock A (today) at a price of $50 a share. You intend to hold it for four months. Having bought the share, you would like to protect your downside while participating completely on the upside. Specifically, you would like to ensure that your investment does not fall below $50. Both a call and a put are available (on Stock A) with an exercise price of $50. The options are European and expire in four months. a) What strategy would you employ to meet your objectives? b) Use a table to show the total payoff on your overall strategy (or portfolio) at the end of your investment horizon (in four months). c) Draw the total payoff diagram for your overall strategy (or portfolio) at the end of your investment horizon (in four months). Label your axes and mark them with appropriate values where necessary.arrow_forwardYou would like to be holding a protective put position on the stock of XYZ Company to lock in a guaranteed minimum value of $240 at year-end. XYZ currently sells for $240. Over the next year, the stock price will either increase by 7% or decrease by 7%. The T-bill rate is 3%. Unfortunately, no put options are traded on XYZ Company. Required: a. How much would it cost to purchase if the desired put option were traded? (Do not round intermediate calculations. Round your answer to 2 decimal places.) b. What would be the cost of the protective put portfolio? (Do not round intermediate calculations. Round your answer to 2 decimal places.)arrow_forward

- Please solve the problem max in 30-60 minutes. Please no reject thank u 2. The Charter Company currently owns preferred stock with dividends paid of IDR 1300. If it is estimated that the shares can be sold at a market price of IDR 8000. Determine the cost of preferred stock (KP).arrow_forwardThis is my assignmentarrow_forwardWellington Jumbo Crab’s stock currently sells for $100 per share. Last week the firm issued rights to raise new equity. To purchase a new share, a stockholder must remit $20 and three rights. What is the price of one right? Group of answer choices $60 $40 $20 $80arrow_forward

- You started with a market price of $30 and 10,000 shares. Calculate number of shares after the split and the per share price: a. 2 for 7 split b. 3 for 2 split c. 2 for 5 split d. 3 for 1 splitarrow_forwardam. 106.arrow_forwardConsider the following limit order book. Limit buy order: Price Size 84.77 200 84.76 100 84.75 400 Limit Sell Order Price Size 84.79 100 84.80 300 85.70 700 If you submitted a market sell order for 400 shares, how much would you receive?arrow_forward

- I don’t understandarrow_forwardIBM stock is currently trading at $100 per share. An investor purchases one Put option contra on IBM with a $100 strike and at a price of $3.00 per contract. Each options contract represer an interest in 100 underlying shares of stock. For each of the following scenarios determine i 7. the option is in the money, at the money, or out of the money. Show your work. A. When the option expires, IBM is trading at $98 B. When the option expires, IBM is trading at $90 C. When the option expires, IBM is trading at $97arrow_forwardYou buy 1 put contract with a strike price of $60 on a stock which you own 100 shares. What are the expiration total values for this position (100 stock shares plus 1 put contract) for prices of $50 and $60 if the put premium is $1.80?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education