Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

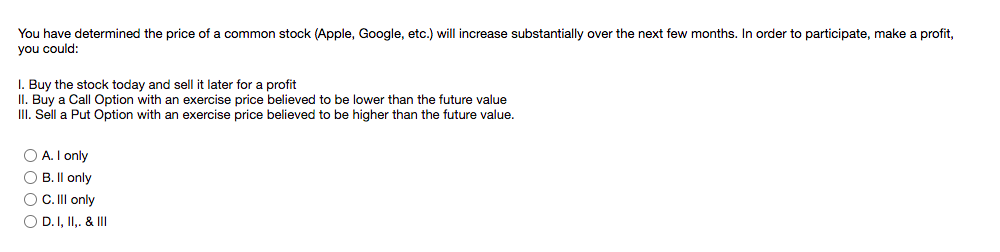

Transcribed Image Text:You have determined the price of a common stock (Apple, Google, etc.) will increase substantially over the next few months. In order to participate, make a profit,

you could:

I. Buy the stock today and sell it later for a profit

II. Buy a Call Option with an exercise price believed to be lower than the future value

III. Sell a Put Option with an exercise price believed to be higher than the future value.

O A. I only

O B. Il only

O C.Il only

O D.I, II. & III

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- In follow an Ito process with >0, a stock is worth $80 today, if the price of an option that pays the holder $2 exactly the first time the stock price reaches $200, what is the price of an option? Show all calculation.arrow_forwardExplain well all point of question with proper answer.arrow_forwardWhich of the following is TRUE? a. A bull market is where stocks, on average, are expected to go up in the near future. b. A bull market is the primary market where IPO's are introduced. c. A bull market is a situation where the price of stock in that market has been rising over a fairly long period of time d. A bull market is a market where there are more buyers than sellers, there have been more purchases of stock than sales of stock and a lot of stock is traded every day.arrow_forward

- You have written a call option on Walmart common stock. The option has an exercise price of $81, and Walmart’s stock currently trades at $79. The option premium is $1.60 per contract. a. How much of the option premium is due to intrinsic value versus time value? b. What is your net profit if Walmart’s stock price decreases to $77 and stays there until the option expires? c. What is your net profit on the option if Walmart’s stock price increases to $87 at expiration of the option and the option holder exercises the option?arrow_forwardSuppose you own a put option on Apple stock with a strike price of $150. Suppose it is the expiration date of the option and the current stock price of Apple is $75. What payoff will you receive from making an optimal exercise decision on your option? 1. -$75 2. $0 3. $75arrow_forwardanswer the questions as soon as possiblearrow_forward

- Suppose that a European call option to buy a share for $ 90.00 costs a . Under what circumstances will the SELLER of the option make a profit ? \$4.00 and is held until maturity . ( DRAW the GRAPH to show ALL answers ) b . when will the option be exercised ( at what price , show on graph ) ? c . What is the Maximum profit for SELLER and at what stock price ? d . What is the Maximum loss for SELLER and at what stock price ? e . What will be profit / loss for SELLER if St is 150 ?arrow_forwardOptions2. Construct profit diagrams at expiration time to show what position in META puts, calls and/or underlying stock best expresses the investor’s objectives described below. META currently sells for $210 so that profit diagrams between $150 and $250 in $10 increments are appropriate. Assume that at-the-money puts and calls currently cost$30 each. The call with strike $190 costs $40 and the call with strike $230 costs $20. (a) An investor wants to benefit from META price drops but does not want to lose more than $30 on the investment. (b) An investor wants to have a positive payoff if the upcoming META earnings announcement is close to market expectations—meaning that the price will not move by more than $20 dollars.arrow_forwardCovered Calls Please help me.arrow_forward

- please give me the correct answer fully DO NOT GIVE ME THE WRONG ANSWER ANSWER EACH COLUMNarrow_forwardSuppose that call options on XYZ stock with time to expiration 3 months and strike price $90 are selling at an implied volatility of 30% ExxonMobil stock price is $90 per share, and the risk free rate is 4%. Required: a1 If you believe the true volatility of the stock is 32%, would you want to buy or sell call options? a2-Now you want to hedge your option position against changes in the stock price. How many shares of stock will you hold for each option contract purchased or sold?arrow_forwardWhat is the bond, bond valuation, and interest rates of CVS in 2020?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education