FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

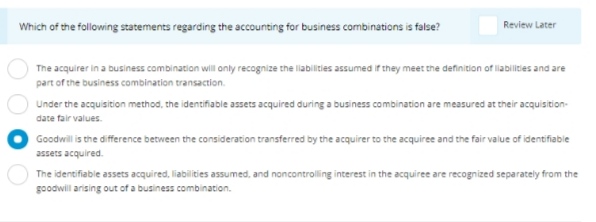

Transcribed Image Text:Which of the following statements regarding the accounting for business combinations is false?

Review Later

The acquirer in a business combination will anly recognize the labilities assumed if they meet the definition of liabilities and are

part of the business combination transaction.

Under the acquisition method, the identifiable assets acquired during a business combination are measured at their acquisition-

date fair values.

Goodwill is the difference between the consideration transferred by the acquirer to the acquiree and the fair value of identifiable

assets acquired.

The identifiable assets acquired, liabilities assumed, and noncontrolling interest in the acquiree are recognized separately from the

goodwill arising out of a business combination.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Statement I: For each business combination, an acquiree is always identified.Statement II: The acquisition date is the date where the acquiree obtains control over the acquirer. a. True, False b. True, True c. False, True d. False, Falsearrow_forwardWhat is a good response to? The unrealized intercompany profits can assuredly have an impact on the consolidated financial statements, as true profits and losses will not be recognized until inventory is sold to an unrelated entity. Prior to this third-party sale the intercompany profit or loss in unrealized and must be removed from the reports consolidation to avoid overstating the consolidated net income (Hoyle, Schaefer, & Doupnik, 2024). It is also important to determine if the inventory sale was upstream or downstream, as the considerations will vary based on the sale in relation to the parent company. For an upstream sale (subsidiary to parent company) any unrealized profit or loss can be partially allocated to non-controlling interests assuming such entities exist, and once the inventory has been resold the recognized revenue is subsequently split accordingly. During a downstream sale (parent to subsidiary company) the unrealized revenue is allocated to the parent company,…arrow_forwardWhen an entity uses the fair value model, changes in the fair values of investment property are recognized in profit or loss directly in equity recognized in other comprehensive income not recognizedarrow_forward

- 1) Merchandise invested by an entity under a joint operation agreement should include an entry of a)Debit to Joint Operation under the books of the Joint Operators other than the party who invested b)Credit to merchandise inventory of the Joint Operator who contributed merchandise c)Credit to merchandise Inventory of all the Joint Operators d)Credit to Joint Operation under the books of the party investing the merchandise 2) The interest of the retiring or withdrawing partner is usually measured by his capital balance before his retirement or withdrawal adjusted by the following adjustments except a)profit or loss after the date of the partner’s withdrawal or retirement b)changes in the valuation of all assets and liabilities c)errors in net income in prior years d)profit or loss from the operation from the last closing date of the date of his retirement or withdrawal 3)In case of admission of a partner, the first adjustment that need to be prepared is a) The…arrow_forwardAt acquisition date the net assests of the acquired subsidairy are included in the consolidated financial statement at their acquisition date fair value. However most of the parent assets and liabilities are measured on an historical cost basis . Is this Consistent ? Explain.arrow_forwardDuring the measurement period, which of the following may affect the amount ofgoodwill from business combination? A.New information regarding estimates in the contingent consideration that are not existing atthe date of acquisitionB.Nothing can affect the amount of goodwill.C.New information regarding estimates in the contingent consideration that are existing at thedate of acquisition.D.New information regarding estimates in the contingent considerationarrow_forward

- When the parent's Investment in S account is eliminated in the consolidation process, what replaces this item on the consolidated financial statements? A) The acquisition-date fair values of S's net assets, adjusted for any post-acquisition amortization of Differential. B) The acquisition-date book values of S's net assets, adjusted for any post-acquisition amortization of Differential. C) The book value of S's net assets and S's beginning retained earnings only. D) Only the new goodwill generated from the transaction.arrow_forward16.Explain the process of accounting for mergers and acquisitions. How are the assets and liabilities of the acquired company recorded on the balance sheet of the acquiring company? Discuss the treatment of goodwill and any adjustments that might be necessary post-acquisition. Provide an example of a hypothetical merger and the journal entries that would be recorded.arrow_forwardWhich of the following is/are true regarding goodwill achieved through acquisition as part of business combination? Where the acquirer was able to purchase the business at a discount, the excess of the market capitalization over the consideration transferred will be recognized in profit or loss. The acquirer shall recognize goodwill as of the acquisition date measured as the excess of the aggregate of the consideration transferred over the net of the fair values of all the assets acquired and the liabilities assumed Group of answer choices Both statements are true. None of these statements are true. 2 only. 1 only.arrow_forward

- In an acquisition where control is achieved and the fair value of the consideration transferred is less the fair value of the net assets of the acquired entity, Assuming both entities continue to operate separately, the investment account will be: Select one: O a. Debited by the fair value of the net assets of the acquired entity on acquisition date Ob. Debited by the fair value of the consideration transferred minus the stock issuance costs O c. Debited by the fair value of the consideration transferred on acquisition date O d. Debited by the book value of net assets of the acquired entity on acquisition datearrow_forwardIf a seller makes an intra-entity sale of a depreciable asset at a price above book value, the seller’s beginning Retained Earnings is reduced when preparing each subsequent consolidation. Why does the amount of the adjustment change from year to year?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education