ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

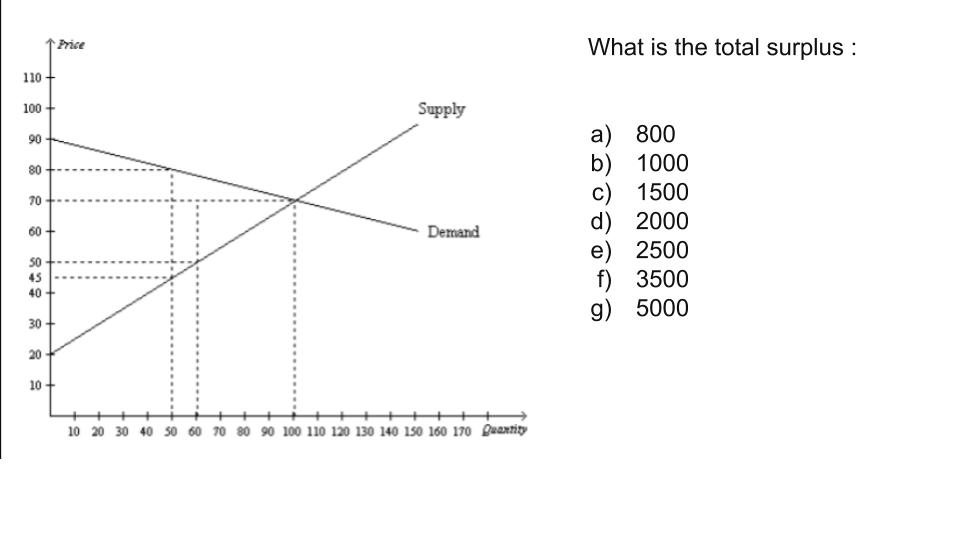

Transcribed Image Text:What is the total surplus :

Price

110 -

Supply

100

a) 800

b) 1000

c) 1500

d) 2000

e) 2500

f) 3500

g) 5000

90

80

70

60-

Demand

50

45

40 +

30

20

10

++++++

10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 160 170 Duantity

Expert Solution

arrow_forward

Step 1

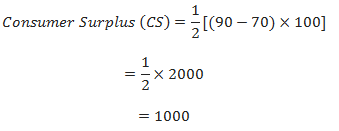

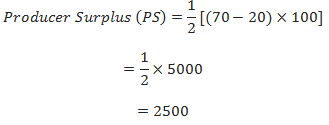

The total surplus in a market is a measure of the total wellbeing of all participants in a market. It is the sum of consumer surplus and producer surplus.

Total Surplus = Consumer Surplus + Producer Surplus

Consumer Surplus is the difference between its Willingness to pay for that product and the products Market Price.

Producer surplus is the difference between its Willingness to sell that product for and the products Market Price.

arrow_forward

Step 2

Consumer surplus can be determined by

Producer surplus can be determined by

Step by stepSolved in 3 steps with 3 images

Knowledge Booster

Similar questions

- Listen | $60 Price 40 20 20 --- Supply Demand 0 50 100 150 200 Quantity What is the equilibrium price and quantity for this market: A) P=60, Q=100 B) P=20, Q=100 C) P=40, Q=200 OD) P=40, Q=150 4Л 6 quare in unitially tv 80 BE F3 Ơ F4 오 ત્ર F5 ৫ ها F6 8 F7 t #4 % do 5 DII F8 * 7 8 > 6 & 8 F9 F10arrow_forwardimg' (a If po increases, what happens to the demand and supply of public transportation (shifts left/shifts right/doesn’t change) What happens to the equilibrium quantity and price for public transportation? (increase/decrease) (b)At a given price p, as oil becomes more expensive (po increases), does the (own) price elasticity of demand for public transportation increase / decrease / stay the same? (c) Calculate the cross-price elasticity of public transportation demand with respect to the oil price po, at the point p = 1 and po = 2. Are the two goods (public transportation and oil) substitutes or complements, or unrelated?arrow_forwardGive correct typing answer with explanationarrow_forward

- 9. When the demand curve shifts, the change in equilibrium price will be larger the moreelastic the supply curve.(a) True(b) Falsearrow_forwardA B|C|DE| F GH $40 $35 $30 $25 $20 $15 $10 $5 $0 0 5 10 15 20 25 30 35 40 40 175 300 375 400 375 300 175 0 (b) Calculate the price elasticity of demand between each set of points on the demand curve (i.e., between A and B, B and C, C and D, D and E, etc.) Point on Demand Curve: Price (P): Quantity Demanded (Qo): TR=PXQ Iarrow_forwardThe market for burritos in a college town is shown to the right. At a price of $7, how much excess demand is there? A. 0; there is excess supply at $7. B. 20 units C. 30 units D. 10 units C… Price 16- 14- 12- 10- 8- 6- 4- 2- 0 0 20 40 60 80 Quantity 100 S D 120 140 160arrow_forward

- Please let me know seftuon A) if the input price would rise or fallarrow_forward13. The table below gives part of the supply schedule for personal computers in the United States. Price Quantity Supplied before tech change Quantity Supplied after tech $1,100 $900 12,000 8,000 change 13,000 9,000 a) Calculate the price elasticity of supply when price rises from $900 to $1,100 using the arc elasticity formula (the midpoint method). b) Now suppose that technology changes such that at every price, 1000 more computers are supplied. Now, as prices rise from $900 to $1,100, is the elasticity of supply smaller than, larger than, or equal to the elasticity in part a)? c) Does the change in b) change the slope of the supply curve? Are slope and elasticity the same thing? Explain.arrow_forwardSOME S&D PROBLEMS 1. A. Find Pe and Qe Price per unit (dollar 8 8 2 2 2 2 2 2 2 2 100 90 80 70 60 50 40 30 20 10 0 200 400 600 Quantity B. What is the effect of a ceiling price of $40? 800 Do 1,000arrow_forward

- Please helparrow_forwardNonearrow_forwardThe table below shows the total demand and supply for bushels of wheat per month. Demand Price per bushel ($) Supply (*000) (*000) 85 3.40 72 80 3.70 73 75 4.00 75 70 4.30 77 65 4.60 79 60 4.90 81 Required: (i) Explain what is the situation that arises when the product price is $3.40 and $4.90?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education