Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

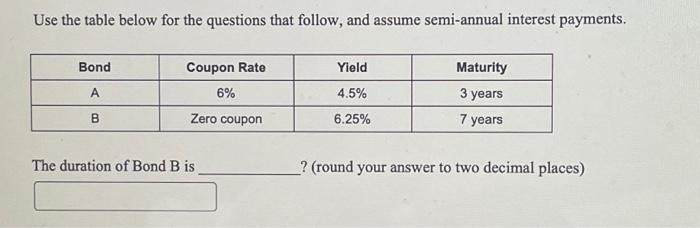

Transcribed Image Text:Use the table below for the questions that follow, and assume semi-annual interest payments.

Bond

A

B

Coupon Rate

6%

Zero coupon

The duration of Bond B is

Yield

4.5%

6.25%

Maturity

3 years

7 years

? (round your answer to two decimal places)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Suppose that the term structure of interest rates is: t 0.5 1 1.5 2 r 1% 1.2% 1.4% 1.8% Interest rates are annual interest rates that are semi-annually compounded. 1. Calculate the price and modified duration of a 1-year bond with a 6% coupon rate, with coupons paid semi-annually. The bond has a face value of 100.0 2. Calculate the price and modified duration of a 2-year bond with a 10% coupon rate, with coupons paid semi-annually. The bond has a face value of 100.0 3. Compare your results from 1 and 2 above. Which bond is more sensitive to changes in interest rates?arrow_forwardSuppose that the current 6-month, 1-year, 1.5-year and 2-year interest rates are 2.2%,3%, 3.5% and 3.75%, respectively. a) Calculate the prices of a 1-year and 2-year Treasury bonds. In each case, assumethe face value of £100 and the coupon rate of 5% per annum and that coupons arepaid semi-annually. Assume continuous compounding. Compare the obtainedresults. Are they consistent with your expectations? b) Calculate the par yield on the 1-year bond with semi-annual couponsarrow_forwardInterest premium. Estimate the default premium and the maturity premium given the following three investment opportunities: a Treasury bill with a current interest rate of 3.25%; a Treasury bond with a twenty-year maturity and a current interest rate of 4.5%; and a AAA, corporate bond with a twenty-year maturity and an interest rate of 9%. What is the default premium? % (Round to two decimal places.)arrow_forward

- Please show detailed steps and correctarrow_forwardneed help with finding the current yield and capital gains yield for bond p and bond d, thank youarrow_forwardConsider a bond with maturity 2 year, 100 face value, coupon 3.60%, and yield 7.20%. Compute a dollar duration numerically using a dy =0.001%, Report you result with two digits decimal accuracy and the correct sign. Example:-185.95 Blank Excel Worksheet Your Answer: Answerarrow_forward

- 3. Suppose that you observe the following two bonds being traded, both of which pay coupons annually and have a $100 face value: Bond Coupon Maturity Rate A B 6% 2% 30 years 30 years Price $147.13 $64.47 If the Law of One Price holds, what is the price of a 30-year Annuity that pays $8 per year starting at t = 1?arrow_forwardces You find a bond with 25 years until maturity that has a coupon rate of 8 percent and a yield to maturity of 9 percent. What is the Macaulay duration? The modified duration? Note: Do not round intermediate calculations. Round your answers to 3 decimal places. Macaulay Modified Duration years yearsarrow_forwardCompute the price of a 5.9 percent coupon bond with 15 years left to maturity and a market interest rate of 9.6 percent. (Assume interest payments are semiannual.) (Do not round intermediate calculations. Round your final answer to 2 decimal places.) Is this a discount or premium bond? premium bond discount bondarrow_forward

- What is the price of the bond that has a coupon rate of 5.6%, a yield to maturity of 6.3%, a face value of $1000, and 25 years to maturity? The coupon payments are annual. Enter your response below. Enter your answer to rounded 2 DECIMAL PLACES.arrow_forwardassume the interest rate on a 1-year t bond is currently 7% and the rate on a 2-year bond is 9%. If the maturity risk premium is .5% what is a reasonable forecast of the rate on a 1 year T bond next year. Round to 2 decimals placesarrow_forwardPLEASE GIVE ME THE RIGHT ANSWERSarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education