ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

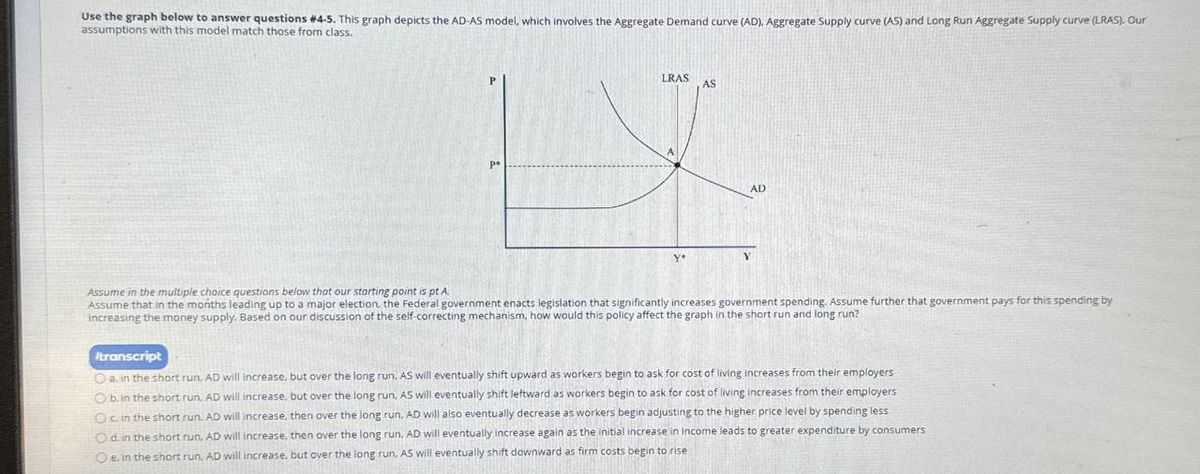

Transcribed Image Text:Use the graph below to answer questions #4-5. This graph depicts the AD-AS model, which involves the Aggregate Demand curve (AD), Aggregate Supply curve (AS) and Long Run Aggregate Supply curve (LRAS). Our

assumptions with this model match those from class.

LRAS

AS

AD

Assume in the multiple choice questions below that our starting point is pt A.

Assume that in the months leading up to a major election, the Federal government enacts legislation that significantly increases government spending. Assume further that government pays for this spending by

increasing the money supply. Based on our discussion of the self-correcting mechanism, how would this policy affect the graph in the short run and long run?

Itranscript

Oa. in the short run, AD will increase, but over the long run, AS will eventually shift upward as workers begin to ask for cost of living increases from their employers

Ob. in the short run, AD will increase, but over the long run. AS will eventually shift leftward as workers begin to ask for cost of living increases from their employers

Oc in the short run. AD will increase, then over the long run, AD will also eventually decrease as workers begin adjusting to the higher price level by spending less

Od. in the short run, AD will increase, then over the long run, AD will eventually increase again as the initial increase in Income leads to greater expenditure by consumers

Oe. in the short run, AD will increase, but over the long run, AS will eventually shift downward as firm costs begin to rise

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- Suppose the aggregate price level has decreased, but workers did not notice this initially. Suppose the supply curve of labor initially looked as follows. According to our self-correcting model, once workers notice that the aggregate price level has decreased, Group of answer choices a) the SL curve will increase (shift right). b) none of the other options. c) the SL curve will decrease (shift left). d) nothing will happen to the Supply of Labor (SL) curve. e) the equilibrium wage level, W, will rise.arrow_forwardPrinciples of Macroeconomics: ECO252 Recalling Classical, Keynesian, and now Supply-side economics. How would you describe each school? Keeping in mind each school's belief in the role of government in the economy and how economies adjust back to their ideal output yields full employment.arrow_forwardBetween 2007 and 2009, the United States experienced a severe financial crisis and economic downturn commonly known as the Great Recession. Starting in 2006, housing values fell 30%, causing losses in mortgage-backed securities for families and financial institutions. The recession was marked by a drop in aggregate demand that caused a decline in GDP and an increase in unemployment. Attached is an example of an aggregate demand and aggregate supply (AD/AS) model that illustrates the general trends of the U.S. economy during the Great Recession. How did the AD/AS equilibrium change over time? Support your claims by referring to your AD/AS model. Select an economic factor (GDP, unemployment, price level) and explain what impact any shifts in AD or AS (or both) had on your chosen factor. Please tailor the answer according the AD/AS model in layman's termsarrow_forward

- QUESTION 2 Consider the aggregate supply-aggregate demand (AD-AS) model that we saw in class. Assume that prices are fixed in the short run and are fully flexible in the long run. The initial full-employment level of output is y- g00 and the initial price level is p= 100: The aggregate demand curve is given by y= 1500 - 6P: Scenario 1, long run: A reduction in personal income taxes shifts the demand curve to y=1530 – 6P. In the long run, the output is and the price level is Note: Type in your answer rounded to two decimal places, i.e., your answer must be of the form "999.99". I will not be able to fix correct answers that were entered incorrectly, such as "999.999" or "999,99" or "999". In case the last digit in the correct answer is zero, e.g., "999.90" or "999.00", Blackboard may automatically delete it and you should not do anything about it. In case of percentages, do not type in the percentage symbol "%".arrow_forwardOn the graph, label your starting AD line as AD 2019. Draw a new AD line showing the change to AD due to the pandemic. Label your starting SRAS line as SRAS 2019. Draw a new SRAS line showing the change to supply due to the pandemic.Label the new short-run equilibrium RGDP and Price Level. Does output (i.e. RGDP) increase or decrease in your model? Does the price level increase or decrease in your model? According to the AD-AS model when RGDP falls the unemployment rises and vice versa. Does your graph indicate an increase or decrease in the unemployment ratearrow_forwardSuppose that the coronavirus pandemic (COVID 19) in 2020 has resulted in a leftward shift of the aggregate demand curve (it has also shifted the short-run aggregate supply to the left, but let’s ignore this effect here for simplification). A. Use the aggregate-demand/aggregate-supply model to show the effects on output and the price level/inflation in both the short run and long run (assume that the short-run aggregate supply curve is upward sloping). B. Show the adjustment process of the economy from the short run to the long run. C. What is the effect on unemployment in short run and long run? D. Can policymakers use monetary policy (and/or fiscal policy) to accommodate this shock? Describe what happens to the economy in response to this policy action.arrow_forward

- The graph below presents the Short Run Aggregate Supply Curve and the Aggregate Demand Curve for Sanaton in 2001. Based on this graph, answer the questions: What is equilibrium output (Real GDP)? What is equilibrium price level?arrow_forwardWhat happened first was a major policy-induced supply shock. The lockdown forced firms in several directly affected sectors, from restaurants to hotels to airlines, to halt (or at least to drastically decrease) supply. In contrast to other supply shocks analyzed earlier in the book, many firms had no choice other than to stop or decrease production. As a result of sharply lower output, and thus lower income, and of increased uncertainty, this shock had a major effect on demand, not just in the sectors directly affected by the lockdown, but also in the non-affected sectors. Thus, the outcome was a combination of a supply shock and a sharp demand response. In that context, the role of macroeconomic policy was twofold. First: While it could not do much to increase output in the affected sectors, it needed to protect the firms in those sectors from going bankrupt and the workers who lost work from going hungry. Second: It needed to limit the effect of lower demand in the non-affected…arrow_forward31) Use the dynamic model of aggregate demand and supply to illustrate a situation where aggregate demand and short-run aggregate supply are both increasing from year 1 to year 2, resulting in a higher price level and higher level of real GDP at macroeconomic equilibrium in year 2. 32) Hurricane Katrina resulted in a decline in oil production infrastructure along the gulf coast. As a result there was an unexpected decline in oil and natural gas supplies in 2005. Suppose that this caused an increase in the price level and a decline in real GDP in 2006. Also assume that potential real GDP continued to grow due to other factors. You can assume the aggregate demand curve did not change. Show the macroeconomic equilibrium for 2005 and 2006 using the dynamic aggregate supply and aggregate demand model. 1arrow_forward

- can you expand on the question and provide a demand and supply diagram relating to the topic "disequilibrium"arrow_forwardQUESTION 4 Consider the aggregate supply-aggregate demand (AD-AS) model that we saw in class. Assume that prices are fixed in the short run and are fully flexible in the long run. The initial full-employment level of output is y-900 and the initial price level is P= 100. The aggregate demand curve is given by y=1500 – 6P. %3D Scenario 2, long run: A major earthquake destroys a part of the economy's capital stock and reduces the full-employment level of output shifts to y = 880: In the long run, the output is and the price level is Note: Type in your answer rounded to two decimal places, i.e., your answer must be of the form "999.99". I will not be able to fix correct answers that were entered incorrectly, such as "999.999" or "999,99" or "999". In case the last digit in the correct answer is zero, e.g., "999.90" or "999.00", Blackboard may automatically delete it and you should not do anything about it. In case of percentages, do not type in the percentage symbol "%".arrow_forwardSuppose that the aggregate demand and aggregate supply schedules for a hypothetical economy are as shown in the following table Amount of Price Level Amount of Real GDP (Price Index) Real GDP Demanded, Supplied, Billions Billions $100 300 $450 200 250 400 300 200 300 400 150 200 500 100 100 a. Use the data above to graph the agregate demand and aggregate supply curves. What are the…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education