ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

Use the following data to analyze the condition when the product proce is set at $32

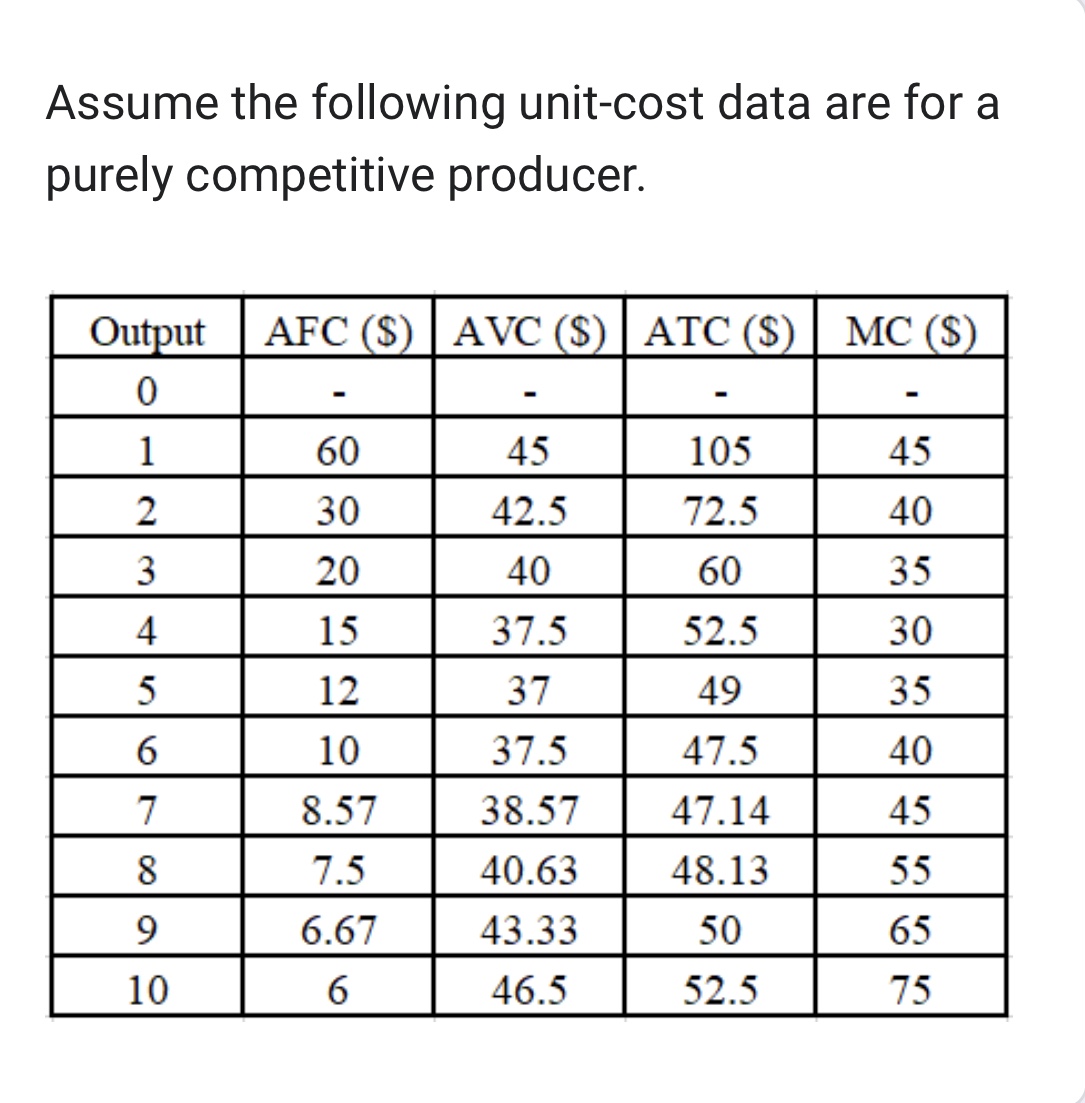

Assume the following unit cost data are for a purely competitive producer. See table below:

Required:

A. What will be the

B. How much would be the economic profit that the firm will realize per unit of output?

C. How much would be the product

Transcribed Image Text:Assume the following unit-cost data are for a

purely competitive producer.

Output AFC (S) AVC (S) ATC ($) MC ($)

0

1

2

3

4

5

6

7

8

9

10

-

60

30

20

15

12

10

8.57

7.5

6.67

6

-

45

42.5

40

37.5

37

37.5

38.57

40.63

43.33

46.5

-

105

72.5

60

52.5

49

47.5

47.14

48.13

50

52.5

45

40

35

30

35

40

45

55

65

75

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 5 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 20) - Google Chrome "mod/quiz/attempt.php?attempt%3=1579003&cmid%3812962&page%3D2 em (Academic 20- MC ATC AVC 16 4. 5 10 15 20 25 30 35 40 45 50 Quantity (units per day) The above figure shows the cost curves for a perfectly competitive firm. If all firms in the market have th same cost curves and the price equals $16 per unit Select one: O a. over time, the price will fall as new firms enter the market. O b. over time, firms will leave this market. O c. the market is in its long-run equilibrium. O d. the firm is making zero economic profit. o search hp Price and cost (dollars per unit)arrow_forwardMr DIY is a new small scale palm oil supplier. There are many small scale palm oil suppliers in the market. The price of oil palm is solely determined by the market demand and supply. Describe the perfectly competitive market of this industry. As Mr DIY is a new firm in the market, his firm is facing a problem of revenue lesser than the total variable costs. Illustrate the situation with an appropriate diagram(s). Evaluate the situation of this firm and provide one suggestion for the firm to sustain in the long run.arrow_forwardA company that manufactures tablet computers determines that the fixed costs for producing the tablet computers are $45,000. The variable costs for producing each tablet computer are $75. The company decides to sell each tablet computer for $250. Part A: Write the cost and revenue equations if the company produces and sells a tablet computers.arrow_forward

- A firm has fixed costs of $40 and variable costs as indicated in the table below. For each level of output (total product) calculate total cost, average fixed cost, average variable cost, average total cost and marginal cost. Write your response in the table provided. b) Discuss why a firm in perfect competition will not charge a price above or below the market price.arrow_forwardThe following cost data is for a firm which is selling in a perfectly competitive market: Average fixed Average variable Average total Total Marginal cost S17 product cost S100.00 50.00 33.33 25.00 20.00 cost $17.00 cost $117.00 66.00 47.33 39.25 34.00 2 16.00 15 3 4 15.00 14.25 14.00 14.00 15.71 17.50 13 12 13 16.67 14.29 12.50 11.11 10.00 9.09 7.33 30.67 30.00 14 26 30 35 7 8. 9. 10 11 30.00 30.55 31.60 33.09 35.00 19.44 21.60 41 24.00 48 12 26.67 56 Refer to the data above. If there were 600 identical firms in this industry and total or market demand is as shown below, equilibrium price will be: Quantity demanded 3,000 6,000 9,000 11,000 14,000 19,500 Price $50 42 36 32 20 13 $36arrow_forwardps ndar 2 You're running a small firm, and you have an estimate of both your cost function and your demand curve. Your cost function is TC-791-11q+5g 2. while your inverse demand curve is P-870-0.4q, where P is the price of one unit of your output and q is the quantity of units produced and sold If you wanted to maximize profit. what quantity would you produce? Please round your answer to the nearest whole number (ie, no decimal places) Type your answer...arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education