Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

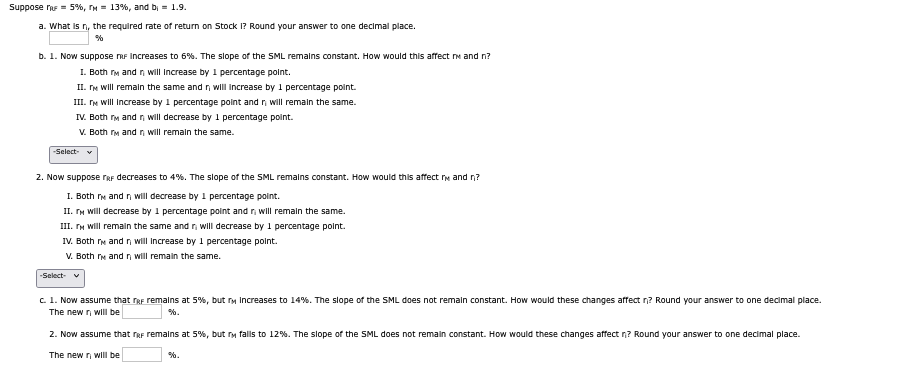

Transcribed Image Text:Suppose 5%, TH 13%, and b₁ = 1.9.

a. What is n, the required rate of return on Stock I? Round your answer to one decimal place.

%

b. 1. Now suppose mr increases to 6%. The slope of the SML remains constant. How would this affect and n?

1. Both г and will increase by 1 percentage point.

II. г will remain the same and n will increase by 1 percentage point.

III. will increase by 1 percentage point and n will remain the same.

IV. Both г and n will decrease by 1 percentage point.

-Select-

V. Both г and will remain the same.

2. Now suppose гRF decreases to 4%. The slope of the SML remains constant. How would this affect and n?

I. Both and will decrease by 1 percentage point.

II. г will decrease by 1 percentage point and r, will remain the same.

III. г will remain the same and r will decrease by 1 percentage point.

IV. Both г and n will increase by 1 percentage point.

-Select-

V. Both г and will remain the same.

c. 1. Now assume that RF remains at 5%, but г increases to 14%. The slope of the SML does not remain constant. How would these changes affect r? Round your answer to one decimal place.

The new r will be

%.

2. Now assume that RF remains at 5%, but г falls to 12%. The slope of the SML does not remain constant. How would these changes affect ? Round your answer to one decimal place.

The new r will be

%.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Similar questions

- Suppose rRF = 4%, rM = 11%, and bi = 1.5. What is ri, the required rate of return on Stock i? Round your answer to two decimal places. % 1. Now suppose rRF increases to 5%. The slope of the SML remains constant. How would this affect rM and ri? Both rM and ri will decrease by 1%. Both rM and ri will remain the same. Both rM and ri will increase by 1%. rM will remain the same and ri will increase by 1%. rM will increase by 1% and ri will remain the same.arrow_forwardConsider the following returns and states of the economy for TZ.Com.: Economy Probability Return Weak 40% 1% Normal 50% 8% Strong 10% 39% What is the standard deviation of TZ's returns? SET YOUR CALCULATOR TO FOUR DECIMAL PLACES AND ROUND TO 2 DECIMAL PLACES AT THE END. DO NOT ENTER THE %. FOR EXAMPLE, IF YOUR ANSWER IS 7.70% ENTER IT AS 7.70.arrow_forwardRequired Rate of Return Suppose rRF = 3%, rM = 8%, and rA = 7%. Calculate Stock A's beta. Round your answer to one decimal place. If Stock A's beta were 1.1, then what would be A's new required rate of return? Round your answer to one decimal place. %arrow_forward

- 37. An analyst developed the following probability distribution of the rate of return for a common stock: Rate of return Scenario Recession -0.05 0.10 0.25 What's the standard deviation of the rate of return? Show your calculations. n k=ZkP |o= i=1 A. 0.0549. B. 0.0649. Normal Boom . 0.0749. D. 0.0849 E. 0.0949. 건 Probability 0.20 0.60 0.20 i-1 (k₂ − Ê)² P₂.arrow_forwardConsider the rate of return of stocks ABC and XYZ. Year rABC rXYZ 1 22 % 34 % 2 12 12 3 14 18 4 7 0 5 1 −8 1. If you were equally likely to earn a return of 22%, 12%, 14%, 7%, or 1%, in each year (these are the five annual returns for stock ABC), what would be your expected rate of return? (Do not round intermediate calculations.) 2. What if the five possible outcomes were those of stock XYZ? 3. Given your answers to (d) and (e), which measure of average return, arithmetic or geometric, appears more useful for predicting future performance? A. Arithmetic B. Geometricarrow_forwardAssume that the risk-free rate is 2.5% and the required return on the market is 12%. What is the required rate of return on a stock with a beta of 2? Round your answer to two decimal places.arrow_forward

- You are given the following expected returns for a share under various scenarios. Scenario Probability Expected returnBoom16 % 34.6%Normal41 % 4.4% Recession 43% - 5.2% Calculate the expected return as a percent. Please enter the number as a percentage without the % sign (as you do for the interest rate in the calculator). For example, if your answer is 7.89%, then simply answer "7.89".arrow_forwardSuppose your expectations regarding the stock market are as follows: State of the Economy Boom Normal growth Recession Probability 0.3 0.6 0.1 Mean Standard deviation HPR 24.90 % % 41% 24 E (r) E-1P(s)r (s) Var (r) = o² = s-1p(s)[r (s) - E(r)]² SD (r) = o = √Var (r) Required: Use above equations to compute the mean and standard deviation of the HPR on stocks. (Do not round intermediate calculation Round your answers to 2 decimal places.) -18 Karrow_forwardConsider the following returns and states of the economy for TZ.Com.: Economy ProbabilityReturn Weak 15% Normal 50% Strong 35% -9% 2% 6% What is the standard deviation of TZ's returns? SET YOUR CALCULATOR TO FOUR DECIMAL PLACES AND ROUND TO 2 DECIMAL PLACES AT THE END. DO NOT ENTER THE %. FOR EXAMPLE, IF YOUR ANSWER IS 7.7011% ENTER IT AS 7.70.arrow_forward

- Assignant. How to use real Dato to draw the Efficient Frontier? Step: Choose 2 Stocks collect Date for 1 year (daily) Prices Colorlate Returns (daily returns) Pt+1 - Pt Pt R 7,41 STEP 2 6 。Comporte the Expected Return for each stock E(R) = Average Return = Σ Ri - • Compte Risk (6;) => √2 (2:-R)2 R mpute the CORR between the 2 stocks Compute Comply for cov) forarrow_forwardIf D0 = $2.00, g (which is constant) = 5.0%, and P0 = $40, then what is the stock’s expected dividend yield for the coming year?arrow_forwardSuppose TRF = 4%, TM = 9%, and b = 1.1. a. What is n, the required rate of return on Stock i? Round your answer to one decimal place. % b. 1. Now suppose rar increases to 5%. The slope of the SML remains constant. How would this affect ry and n? I. ry will increase by 1 percentage point and n will remain the same. II. Both ry and r, will decrease by 1 percentage point. III. Both rm and r, will remain the same.. IV. Both r and r, will increase by 1 percentage point. V. r will remain the same and r, will increase by 1 percentage point. -Select- v 2. Now suppose rar decreases to 3%. The slope of the SML remains constant. How would this affect ry and n? I. TM will decrease by 1 percentage point and n will remain the same. II. rs will remain the same and n will decrease by 1 percentage point. III. Both ry and r, will increase by 1 percentage point. IV. Both ry and r, will remain the same. V. Both ry and r, will decrease by 1 percentage point. Selectarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education