ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

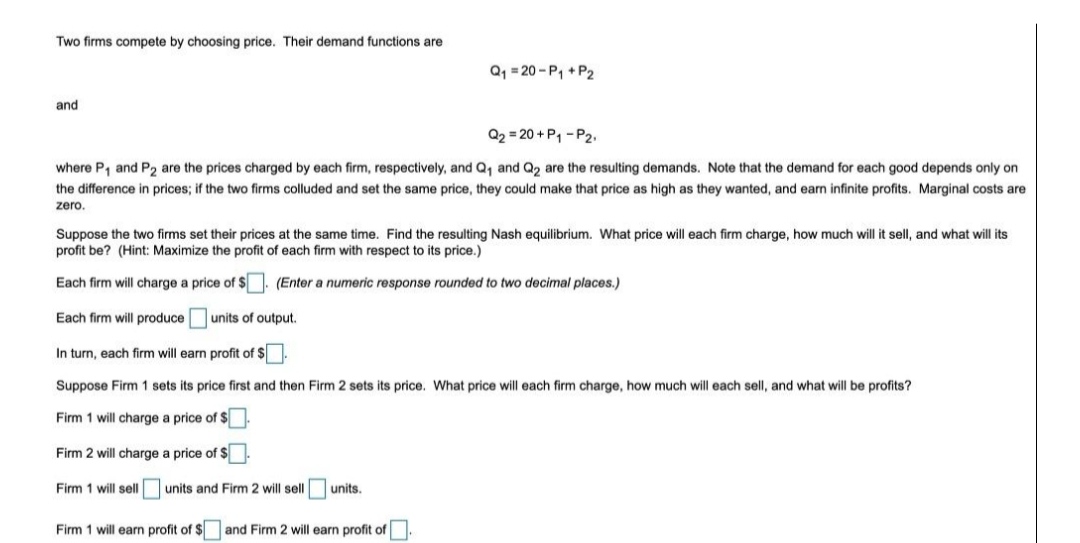

Transcribed Image Text:Two firms compete by choosing price. Their demand functions are

Q, = 20 - P, +P2

and

Q2 = 20 + P1 - P2.

where P, and P2 are the prices charged by each firm, respectively, and Q, and Q2 are the resulting demands. Note that the demand for each good depends only on

the difference in prices; if the two firms colluded and set the same price, they could make that price as high as they wanted, and earn infinite profits. Marginal costs are

zero.

Suppose the two firms set their prices at the same time. Find the resulting Nash equilibrium. What price will each firm charge, how much will it sell, and what will its

profit be? (Hint: Maximize the profit of each firm with respect to its price.)

Each firm will charge a price of $ (Enter a numeric response rounded to two decimal places.)

Each firm will produce

units of output.

In turn, each firm will earn profit of $

Suppose Firm 1 sets its price first and then Firm 2 sets its price, What price will each firm charge, how much will each sell, and what will be profits?

Firm 1 will charge a price of $

Firm 2 will charge a price of $

Firm 1 will sell O units and Firm 2 will sell units.

Firm 1 will earn profit of $ and Firm 2 will earn profit of.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 12 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Two firms produce and sell differentiated products that are substitutes for each other. Their demand curves are Firm 1: Q₁ = 40-3P₁+ P₂ Firm 2: Q₂ = 40-3P 2+ P1 Both firms have constant marginal costs of $2.30 per unit. Both firms set their own price and take their competitor's price as fixed. Use Nash equilibrium concept to determine the equilibrium set of prices. Since the firms are identical, they will set the same prices and produce the same quantities. In equilibrium, each firm will charge a price of $ and produce units of output. (Enter your responses rounded to two decimal places.) Each firm will earn a profit of $. (Enter your response rounded to two decimal places.)arrow_forwardFirm 1 and firm 2 are Bertrand duopoloists. Firm 1 has a marginal cost of $6.00 per unit, and firm 2 has a marginal cost of $8.01 per unit. The demand for their product is p=23.00−Q, where Q is the total quantity demanded. How much does each firm sell in equilibrium? Assume that prices can only be set to the nearest cent, firms split the market if they set the same price, and there are no fixed costs. Firm 1 production:______ Firm 2 production:______ What are the profits for each firm in equilibrium? Firm 1 profit: $______ Firm 2 profit: $______arrow_forwardQUESTION 14 Consider the following simultaneous move game between two firms. Each firm can charge either a low or a high price. The numbers represent the profit of each firm at each period. Firm 1 High Price Low Price r≥ 40% r≥ 20% Firm 2 High Price Low Price 30,30 0,55 r≥ 50% full cooperation cannot be achieved in this game. Or≤ 20% 55,0 This game is repeated infinity times, and at each period both players must choose their actions simultaneously. In this case, cooperation at the high price will be possible if the interest rate, r, is r≤ 50% r≤ 40% The players are deciding whether or not to cooperate - specifically, whether or not to follow this cooperation strategy: "Each player will play 'high price' as long as no one has played 'low price' before. If someone has played 'low price' before, then each player will play 'low price' forever." 25, 25arrow_forward

- Consider two firms, referred to as firms 1 and 2, who compete in a market by choosing quantities produced and face the following inverse demand: P(Q) 10-20 Each firm has a marginal cost of production of $4.00. Suppose these firms collude by agreeing to produce quantities to maximize their joint profits. Firm 1 sticks to the agreement, but firm 2 does not. If firm 2 can secretly change its produced quantity, how much would it produce?arrow_forwardSee image for questions partsarrow_forwardTwo firms sell substitutable products; the market price is: P = 90-Q, where Q Q₁ + Q2 is the total market quantity, which consists of Q1₁ (the quantity produced by Firm 1) and Q2 (the quantity produced by Firm 2). The firms choose their quantities simultaneously. Firm 1's costs are C₁ 6Q₁ + Q². Firm 2's costs are C₂ = Q². = O Which is the payoff function for Firm 2? O π₂ = 90Q₂ - 2 Which is the best response function for Firm 1? O π₂ = 90Q₂ - Q²². πT2 π₂ = 45 - Q² Q₁ Q₂₁ 2 O π₂ = 45 - 1²/20₁². Q₁ Q₁ 3 = 16. ²/Q²-Q₁2. = 32- 2- 1/1/202₂. 3 Q₁ = 45. Q1 = 40 + ²/Q₂₁ 2.2. = 10- -arrow_forward

- Suppose the airline industry consisted of only two firms: American and Texas Air Corp. Let the two firms have identical cost functions, C(q) = 28q. Assume that the demand curve for the industry is given by P = 100 - Q and that each firm expects the other to behave as a Cournot competitor. Calculate the Cournot-Nash equilibrium for each firm, assuming that each chooses the output level that maximizes its profits when taking its rival's output as given. What are the profits of each firm? (Round all quantities and dollar amounts to two decimal places.) When competing, each firm will produce units of output.arrow_forwardConsider a duopoly with homogenous goods where Firm 1 has the following production function: Q1 = F1(L,K) = L1/2 K1/2, where Q and K are measured in units and L in hours. Firm 2 uses labour and capital as well but has a different production function, given by Q2 = F2(L,K) = L1/3 K2/3. You may assume that the market for labour and capital is perfectly competitive and the current wage rate is £40 and the rental rate on capital is £10. Both firms sell their products on the same market with inverse demand function P = 52 – (Q1 + Q2), where P is measured in pound sterling. Which production function(s) exhibit(s) decreasing returns to scale? Suppose Firm 1 wishes to produce 6 units. What is the cost minimising input mix for Firm 1? Suppose Firm 2 wishes to produce 4 units. What is the cost minimising input mix for Firm 2? Assume both firms now have the option to produce either 4 units or 6 units. We will consider the situation where both firms simultaneously, but independently,…arrow_forwardConsider two oligopolists, each choosing between a “high” and a “low” level of production. Given their choices of how much to produce, their profits will be as follows: Explain how firm B will reason that it makes sense to produce the high amount, regardless of what firm A chooses. Then explain how firm A will reason that it makes sense to produce the high amount, regardless of what firm B chooses. How might collusion assist the two firms in this case?arrow_forward

- A homogenous-good duopoly faces an inverse market demand function of p = 150 − Q. Assume that both firms face the same constant marginal cost, MC1 = MC2 = 30. Calculate the output of each firm, the market output, and the market price in a Nash-Cournot equilibrium Re-solve part (a) assuming that the marginal cost of firm 1 falls to MC1 =20 Explain what will happen to each firm’s output, the market output, and the market price if the two firms can collude (e.g., form a cartel)arrow_forwardConsider a duopoly where firms compete in prices and firms do not have any capacity constraints. Market demand is P(Q)=45-4Q, and each firm faces a marginal cost of $9 per unit. How much is each firm's total variable cost if firms equally divide the market at Nash equilibrium?arrow_forwardSuppose two firms, A and B, have a cost function of ?(??) = 30??, for ? = ?, ?. The inverse demand for the market is given by ? = 120 − ?, where Q represents the total quantity in the market, ? = ?? + ??. 1. Solve for the firms’ outputs in a Nash Equilibrium of the Cournot Model. 2. Let Firm A be the first mover, and Firm B be the second mover. Solve for the firms’ outputs in a SPNE of the Stackelberg Model.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education