ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

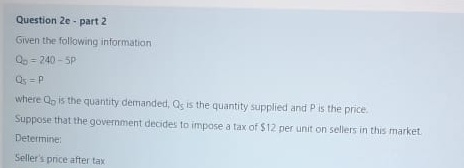

Transcribed Image Text:Question 2e - part 2

Given the following information

Q = 240 - 5P

Qs = P

where Q, is the quantity demanded, Qs is the quantity supplied and Pis the price.

Suppose that the government decides to impose a tax of $12 per unit on sellers in this market.

Determine:

Seller's pnice after tax

Expert Solution

arrow_forward

Step 1

After the imposition of tax price paid by consumer increases whereas price received by producer decreases.

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The demand for wine in town A is actually pA=40−1/2qA; NOT 12qA. Coudl you please let me know how that changes the asnwer?arrow_forwardThe following figure illustrates the demand and supply curves for a good. Price (5) 888 60 40 0 5 10 20 30 Supply Demand Quantity (unit) Refer to the figure above. Which of the following is likely to happen if a price control of $80 is imposed in the market? O There will be a shortage of 25 units in the market. O There will be a surplus of 10 units in the market. O There will be a surplus of 25 units in the market. O There will be a shortage of 10 units in the market.arrow_forwardTax exludes total surplus is 42017arrow_forward

- Can you explain this pleasearrow_forwardH B G 1 hour 30 minutes 45 minutes 15 minutes S D 12 Quantity 2 10 If buyers in this market have to wait in line to purchase this good after a $1 price ceiling is imposed, each buyer purchases only one unit of the good, and buyers in the market value their time at $8 per hour, how long will the line have to be to clear the market?arrow_forwardon Consider the market for tablets depicted below (think iPad or Microsoft Surface). If a price ceiling is adopted at $600, then there will be a shortage of units. P $800 $600 0 75 100 125 S₁ D₁arrow_forward

- Price of Gasoline P3 P₂ P₁ 0 9₂ 9₂ 52 D S₁ Price Ceiling Quantity of Gasoline Refer to the figure above. With a price ceiling present in this market, what will happen when the supply curve for gasoline shifts from S₁ to S₂? The market price will stay at P₁ due to the price ceiling. A shortage will occur at the price ceiling of P2. The price will increase to P3. A surplus will occur at the new market price of P₂.arrow_forwardPlease give me detail answerarrow_forwardDefine consumer and producer surplus and give a geometric interpretation of each.arrow_forward

- e inverse supply function for pizza is: PS = 4 + QS The inverse demand function for pizza is: PD = 10 - QD The price paid by consumers after the government introduces a $2 tax on production is: (Hint: it would be a mistake to do 'Equilibrium Price + $2')arrow_forwardComsumer Surplus Study The goal of this assignment is to apply Calculus to analyze consumer and producer surplus. This activity is based off the economical principles discussed in Section 3.1 of "Principle of Economics" and Section 7 of Chapter 3 in the Business Calculus book. The table below shows how supply and demand of gasoliine vary depending on the price: Price ($/gal) Demand (million of gal.) Supply (million of gal.) 753 513 550 1.2 700 1.4 640 600 1.6 580 639 1.8 543 660 2.2 450 680 2.4 430 700 2.6 420 720 2.8 390 735 3. 367 763 Note: there is some randomization in the above data to account for price fluctuations. Make sure to check that you input the correct data in your device. Perform the following work • Assume that Supply has a quadratic relationship with the price. Find this relationship (the help buttons contain an article to compute trend-lines in Excel): S(p) = Round your answer to 3 decimal places %3D • Assume that the Demand has a quadratic relationship with the…arrow_forwardS 10 - 12 15 Refer to the figure 3.9. A surplus will exist when the price equals $10. the price equals $6. the price is between $0 and $6. quantity demanded equals 15. 8. 6, 2.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education