ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

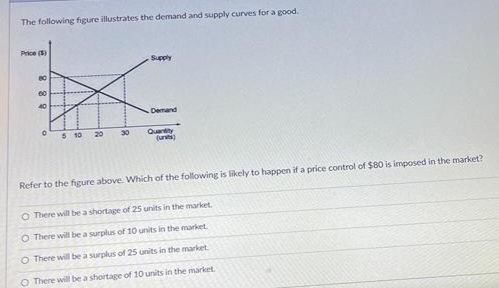

Transcribed Image Text:The following figure illustrates the demand and supply curves for a good.

Price (5)

888

60

40

0

5 10 20

30

Supply

Demand

Quantity

(unit)

Refer to the figure above. Which of the following is likely to happen if a price control of $80 is imposed in the market?

O There will be a shortage of 25 units in the market.

O There will be a surplus of 10 units in the market.

O There will be a surplus of 25 units in the market.

O There will be a shortage of 10 units in the market.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Suppose the supply of apples in a competitive market decreases due to unfavorable weather conditions. As a result, there will be A. a surplus of apples at the existing actual price as the supply curve shifts to the rightB. a shortage of apples at the existing actual price as the supply curve shifts to the leftC. upward pressure on price that will move it to a new equilibrium that is above the initial equilibrium price and elimination of a shortage as the quantity moves to equilibriumD. downward pressure on price as a shortage is eliminated.E. B and C, onlyarrow_forwardf3. Subject Economicsarrow_forwardNot sure what is true or falsearrow_forward

- When a shortage of a good is present due to a price ceiling, the amount supplied will be greater than the amount demanded. the quality of the good will generally improve. O non-price factors, such as discrimination or waiting in line, will play a greater role in the allocation of the good. O the demand for the product will increase and, thereby, eliminate the shortage.arrow_forward12 . Problems and Applications Q10 A market is described by the following supply and demand curves: QSQS = = 3P3P QDQD = = 400−P400−P The equilibrium price is and the equilibrium quantity is . Suppose the government imposes a price ceiling of $80. This price ceiling is , and the market price will be . The quantity supplied will be , and the quantity demanded will be . Therefore, a price ceiling of $80 will result in . Suppose the government imposes a price floor of $80. This price floor is , and the market price will be . The quantity supplied will be and the quantity demanded will be . Therefore, a price floor of $80 will result in . Instead of a price control, the government levies a tax on producers of $40. As a result, the new supply curve is: QSQS = = 3(P−40)3P−40 With this tax, the market price will be , the quantity supplied will be , and the quantity demanded will be . The passage…arrow_forwardRefer to the table above. If demand increased by 4 units at each price , what would the new equilibrium price and quantity be?arrow_forward

- The following graph displays four demand curves (LL, MM, NN, and OO) that intersect at point A. PRICE (Dollars per unit) 200 180 160 140 120 100 80 60 40 20 0 L 0 20 Statement 40 M N B cxx DE ++ x A + O 60 80 100 120 140 QUANTITY (Units) N M Between points A and D, curve NN is elastic. 160 180 200 Using the graph, complete the table that follows by indicating whether each statement is true or false. ? Between points A and B, curve LL is perfectly elastic. Curve NN is less elastic between points A and D than curve MM is between points A and C. True False O O O O Oarrow_forward(Ref: Demand for Apples) The following figure is the demand for apples. 3 2 F I A 1 1 B 1 C D 1 T 1 1 I OB OF+G OE+F+G B+E 1 + 2 E Demand for Apples F G 3 Reference: (Ref: Demand for Apples) 4 H I 10 6 1 7 D (Re Demand for Apples) Suppose you are considering lower the price from $3 to $2. If you do this, which areas on the graph represent the QUANTITY EFFECT? 8arrow_forward33arrow_forward

- Price $2.00 $2.50 $3.00 $3.50 O surplus; increase surplus; decrease Quantity Demanded O shortage; increase O shortage; decrease 3,300 2,800 2,300 1,800 Quantity Supplied Using the table above, if the price is $2.50 the market is experiencing a pressure for the price to 300 800 1,300 1,800 and there isarrow_forwardprovide analysis & computationarrow_forward2arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education