ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:топороту

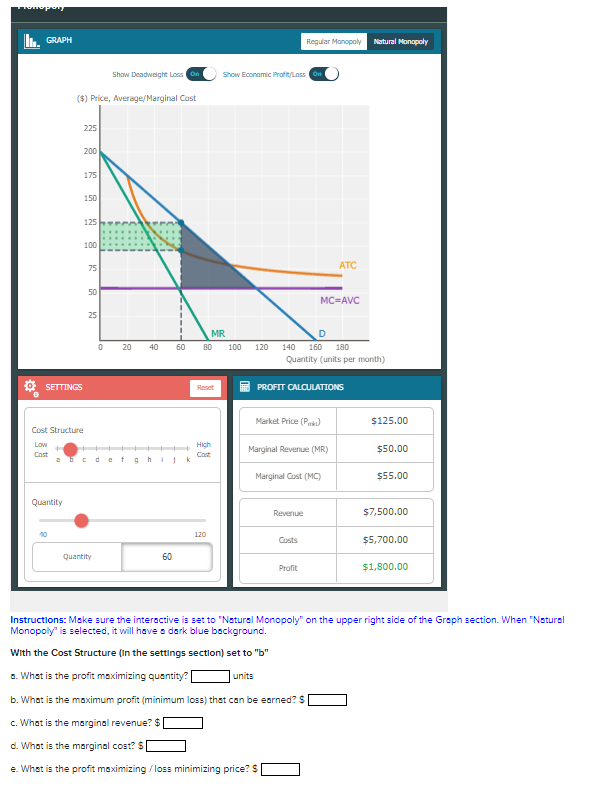

II. GRAPH

Regular Monopoly

Natural Monopoly

Show Deadweight Loss On

Show Economic Profit/Loss On

($) Price, Average/Marginal Cost

གླུ ིི⪜ཞྲི་ཤཱ ཎྜ R R གླུ

225

200

175

150

125

100

SETTINGS

ATC

MC=AVC

MR

D

0

20

40

60

80

100

120

140 160 180

Quantity (units per month)

Reset

PROFIT CALCULATIONS

Market Price (P)

$125.00

Cost Structure

Low

Cost

High

Cost

Marginal Revenue (MR)

$50.00

b C

d с t

9

h

1

k

Marginal Cost (MC)

$55.00

Quantity

10

Quantity

60

Revenue

$7,500.00

120

Costs

$5,700.00

Profit

$1,800.00

Instructions: Make sure the interactive is set to "Natural Monopoly" on the upper right side of the Graph section. When "Natural

Monopoly" is selected, it will have a dark blue background.

With the Cost Structure (in the settings section) set to "b"

a. What is the profit maximizing quantity?

units

b. What is the maximum profit (minimum loss) that can be earned? $

c. What is the marginal revenue? $

d. What is the marginal cost? $

e. What is the profit maximizing / loss minimizing price? $

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- Don't answer by pen paper and don't use chatgpt otherwise we will give dounvotearrow_forwardWhich of the following are characteristics of a monopoly A. Set their own price B. Many buyers and sellers C. Declining long-run average total cost D. Free entry and exitarrow_forwardTyped plz and Asap thanksarrow_forward

- 1. For a price searching firm it's marginal revenue curve (a). Is below it's marginal cost curve (b). Must be vertical (c). Must be horizontal (d). Is below it's a demand curve 2. The most common source of illegal Monopoly today is (a). Predatory pricing (b). Intellectual property rights (c). Royal edict (d). Natural monopoly 3. The market demand is given by p= 420-0.05Q, vrp is the price of the good and Q is the quantity demanded at that price. The monopolist marginal revenue function in this market is (a). MR= 210-0.05Q (b). MR= 420-0.05Q (c). MR= 420- 0.025Q (d). MR= 420-0.1Q 4. In the monopolized ( profit maximizing) market equilibrium p> MC( the price exceeds the marginal cost) this implies that (a). The consumer surplus is equal to the producer surplus (b). The total value of the good is maximized (c). The equilibrium is Marshall inefficient (d). The market price is equal to the market quantity 5. The market demand is given Q= 440-40P, where P is the price of the good…arrow_forward1. How much total revenue does the monopoly firmmake? 2. How much total cost does the monopoly firm incur? 3. How much total profit does the firm make?arrow_forwardplease answer in text form and in proper format answer with must explanation , calculation for each part and steps clearlyarrow_forward

- Price (dollars per jacket) 888888 180 160 140 120 100 60 40 20 0 80 160 MC profit; $13,000 profit; $7,200 Oloss; $8,000 In the figure above, Gap's economic loss: $13,000 ATC The figure shows the demand curve for Gap jackets (D), and Gap's marginal revenue curve (MR), marginal cost curve (MC), and average total cost curve (ATC). MR 240 320 400 Quantity (jackets per day)arrow_forwardQUESTION 30 50 45 40 35 30 25 20 15 10 5 5 a monopoly firm 10 . 15 MR 20 25 MC 30. If this firm maximizes short-term profit, what is the maximum total profit it can earn? a) $126 b) $27 c) $378 d) $9 e) $140 30 ATC DALLA D AVC 35arrow_forwardTC 50 TR 40 30 20 10 10 15 20 25 30 Quantity (units per day) 34) The figure above shows a monopoly's total revenue and total cost curves. The monopoly's economic profit is positive if it produces between A) 0 and 20 units. B) 5 and 20 units. C) 0 and 15 units. D) 0 and 5 units. Total revenue and total cost (dollars per day)arrow_forward

- Question Maxin Suppose a monopolist could charge a different price to every customer based on how much he or she were willing and able to pay (versus charging the same price to all their customers). How would this affect the monopolist's profits? Why? Description Answer eacho Use the editor to format your answer 10 Rointsarrow_forwardDollars ✔ 5,000 0 MC D ATC AVC MR 50 Number of gold hula hoops Figure 10.4 Q Refer to Figure 10.4. The Exclusive Gift Company has a monopoly over the sale of gold hula hoops. This company is currently selling 50 gold hula hoops at a price of $5,000. You are hired as an economic consultant to this company. You should advise this monopolist to shut down in the short run and exit the industry in the long run. O produce in the short run but exit the industry in the long run if conditions do not change. produce in the short run and expand capacity in the long run. shut down in the short run but expand capacity in the long run if conditions do not change.arrow_forwardNote:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education