ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

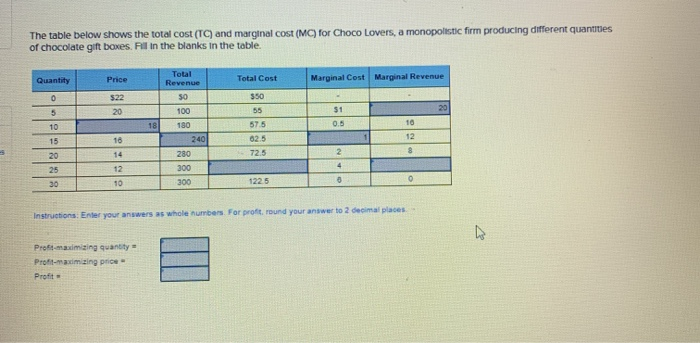

Transcribed Image Text:The table below shows the total cost (TC) and marginal cost (MC) for Choco Lovers, a monopolistic firm producing different quantities

of chocolate gift boxes. Fill in the blanks in the table.

Quantity

0

5

10

15

20

25

30

Price

$22

20

16

14

12

10

Profit

Profit-maximizing quantity

Profit-maximizing price

18

Total

Revenue

50

100

180

240

280

300

300

Total Cost

$50

55

57.5

62.5

72.5

122.5

Marginal Cost Marginal Revenue

$1

0.5

2

4

6

1

10

12

8

Instructions: Enter your answers as whole numbers. For profit, round your answer to 2 decimal places.

0

20

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Beatrice's Birthday Cakes operates in a monopolistically competitive market, so it is one bakery among many in the market for birthday cakes. The following table presents cost and revenue data for birthday cakes at Beatrice's. Quantity Produced (Units) 0 1 2 3 4 5 6 7 8 Costs Total Cost (Dollar 25 28 32 37 43 50 58 67 77 Marginal Quantity Cost (Dollars) (Units) Demanded 0 1 2 3 4 5 6 7 8 Revenues Price (Dollars per unit) 60 54 48 42 36 30 24 18 12 Total Marginal Revenue Revenue (Dollars) (Dollars) Refer to Table 16-4. What is the profit-maximizing output for Beatrice's Birthday Cakes? O a. 6 cakes Ob. 3 cakesarrow_forwardThe accompanying graph depicts average total cost (ATC) marginal cost (MC), marginal revenue (M), and demand (D) 50 facing a monopolistically competitive firm MC 45 Place point A at the firm's profit maximizing price and quantity 40 35 What is the firm's total cost? ATC 30 25 total cost: 20 15 What is the firm's total revenue? 10 5 total revenue: $ MR 0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95100 Quantity What is the firm's total profit? profit: $ Price and Cost ($)arrow_forwardPrice $1.40 $1.00 $0.95 $0.85 $0.60 MR MC ATC D 0 300 500 900 1000 Quantity The monopolistically competitive firm represented in the graph above is in: long-run equilibrium because economic profits are zero at the profit-maximizing output level. short-run equilibrium because price exceeds average total cost at the profit-maximizing output level. both short-run and long-run equilibrium because price exceeds average total cost at the profit-maximizing output level. O both short-run and long-run equilibrium because price equals marginal cost at the profit-maximizing output level.arrow_forward

- A small, local restaurant in St. Augustine, FL, serves scrambled eggs for breakfast. The market for breakfast scrambled eggs is monopolistically competitive. The following graph shows the demand, MR, MC, and ATC curve of this local restaurant. Use the graph to answer questions 3 to 7. Price (P) per plate $10 7 5 3 2 0 MC MR 50 80 100 ATC Number of plates of scrambled eggs served per day (Q)arrow_forwardQ. 2arrow_forwardIf a manufacturer of road bikes operates is a monopolistically competitive market, what does it mean about the products offered by itself and its competitors? Manufacturers offer an array of products that are distinctly similar in a particular way. Manufacturers offer an array of products that are virtually identical on the competition spectrum. Manufacturers offer an array of products that are at opposite ends of the competition spectrum. Manufacturers offer an array of products that are distinctly different in a particular way.arrow_forward

- Answer the next question based on the demand and cost schedules for a monopolistically competitive firm given in the table below. Price $20 18 16 14 12 10 Quantity Demanded 1 2 3 4 5 6 Total Cost $10 20 29 36 40 42 Output 2 4 6 1 3 5 At the profit-maximizing level of output, marginal revenue isarrow_forwarddo fast.arrow_forwardQuestion 19 of 20 > O Macmillan Learning The accompanying graph depicts average total cost (ATC), marginal cost (MC), marginal revenue (M), and demand (D) facing a monopolistically competitive firm. Place point A at the firm's profit maximizing price and quantity. What is the firm's total cost? total cost: $ What is the firm's total revenue? total revenue: $ What is the firm's total profit? profit: $ Price and Cost ($) 50 45 40 35 30 25 20 15 10 5 MR MC ATC D 0 0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95100 Quantityarrow_forward

- botharrow_forwardAnswer all four questions! Is a monopolistically competitive firm productively efficient? How can you tell? Offer one reason why a monopolistically competitive firm might be productively inefficient. Is it allocatively efficient? How can you tell? Offer one reason why a monopolistically competitive firm might be allocatively inefficient.arrow_forwardSuppose the tattoo shop market in Richmond is monopolistically competitive. Consider the market from the perspective of one tattoo parlor, Roses & Thorns. Suppose there were positive economic profits in the market and an additional two tattoo parlors enter the market. What happens to the demand curve for Roses & Thorns tattoos shifts up shifts down stays the samearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education