Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

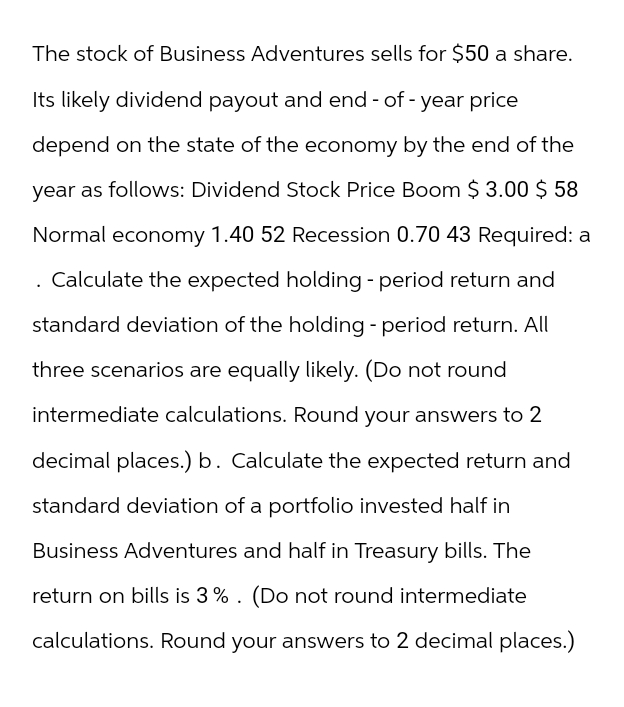

Transcribed Image Text:The stock of Business Adventures sells for $50 a share.

Its likely dividend payout and end-of-year price

depend on the state of the economy by the end of the

year as follows: Dividend Stock Price Boom $ 3.00 $ 58

Normal economy 1.40 52 Recession 0.70 43 Required: a

Calculate the expected holding - period return and

standard deviation of the holding - period return. All

three scenarios are equally likely. (Do not round

intermediate calculations. Round your answers to 2

decimal places.) b. Calculate the expected return and

standard deviation of a portfolio invested half in

Business Adventures and half in Treasury bills. The

return on bills is 3%. (Do not round intermediate

calculations. Round your answers to 2 decimal places.)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- The stock of Business Adventures sells for $65 a share. Its likely dividend payout and end-of-year price depend on the state of the economy by the end of the year as follows: Boom Normal economy Recession Expected return Standard deviation Dividend $2.40 1.60 0.85 Required: a. Calculate the expected holding-period return and standard deviation of the holding-period return. All three scenarios are equally likely. (Do not round intermediate calculations. Round your answers to 2 decimal places.) Expected return Standard deviation Stock Price $73 66 57 % % b. Calculate the expected return and standard deviation of a portfolio invested half in Business Adventures and half in Treasury bills. The return on bills is 3%. (Do not round intermediate calculations. Round your answers to 2 decimal places.) %arrow_forwardThe stock of Business Adventures sells for $30 a share. Its likely dividend payout and end-of-year price depend on the state of the economy by the end of the year as follows: Boom Normal economy Recession Dividend $ 2.00 1.40 0.50 Required: a. Calculate the expected holding-period return and standard deviation of the holding-period return. All three scenarios are equally likely. (Do not round intermediate calculations. Round your answers to 2 decimal places.) Expected return Standard deviation Answer is complete and correct. Stock Price $ 40 34 25 14.33 22.60 Expected return Standard deviation b. Calculate the expected return and standard deviation of a portfolio invested half in Business Adventures and half in Treasury bills. The return on bills is 5%. (Do not round intermediate calculations. Round your answers to 2 decimal places.) % % Answer is complete but not entirely correct. 8.75 11.30 % %arrow_forwardThe stock of Business Adventures sells for $40 a share. Its likely dividend payout and end-of-year price depend on the state of the economy by the end of the year as follows: Boom Normal economy Recession Expected return Standard deviation Dividend $2.00 1.00 0.50 a. Calculate the expected holding-period return and standard deviation of the holding-period return. All three scenarios are equally likely. (Do not round intermediate calculations. Round your answers to 2 decimal places.) Stock Price $50 43 34 Expected return Standard deviation % % b. Calculate the expected return and standard deviation of a portfolio invested half in Business Adventures and half in Treasury bills. The return on bills is 4%. (Do not round intermediate calculations. Round your answers to 2 decimal places.) % %arrow_forward

- Suppose you observe the following situation: Probability of Rate of Return if State Occurs State of Economy Recession Normal Irrational exuberance State 0.25 0.55 0.20 Stock A -0.14 0.07 0.42 Stock B -0.12 0.07 0.22 a. Calculate the expected return on each stock. (Round the final answers to 2 decimal places.) Expected Return Stock A Stock B % % b. Assuming the capital asset pricing model holds and stock A's beta is greater than stock B's beta by 0.55, what is the expected market risk premium? (Do not round intermediate calculations. Round the final answer to 2 decimal places.) Expected market risk premium %arrow_forwardSuppose your expectations regarding the stock price are as follows: State of the Market Probability Ending Price HPR (includingdividends) Boom 0.30 $ 140 53.5 % Normal growth 0.28 110 17.5 Recession 0.42 80 −12.0 Use the equations E(r)=Σsp(s)r(s)E(r)=Σsp(s)r(s) and σ2=Σsp(s) [r(s)−E(r)]2σ2=Σsp(s) [r(s)−E(r)]2 to compute the mean and standard deviation of the HPR on stocks. (Do not round intermediate calculations. Round your answers to 2 decimal places.)arrow_forwardSuppose your expectations regarding the stock price are as follows: State of the Market Boom Normal growth Recession Probability Ending Price 0.21 $ 140 0.30 110 0.49 80 Use the equations E (r) = Ep (s) r(s) and o² = Ep (s) [r(s) - E(r)]² to compute the mean and standard deviation of the HPR on S S HPR (including dividends) 50.5% 18.0 -12.5 stocks. Note: Do not round intermediate calculations. Round your answers to 2 decimal places. Mean Standard deviation Answer is complete but not entirely correct. 13.65 % 20.48 %arrow_forward

- Suppose you observe the following situation: Probability of State 0.35 0.40 0.25 State of Economy Recession Normal Irrational exuberance Stock A Stock B Expected Return Rate of Return if State Occurs Stock B % Stock A a. Calculate the expected return on each stock. (Round the final answers to 2 decimal places.) -0.11 0.10 0.45 -0.09 0.10 0.25 b. Assuming the capital asset pricing model holds and stock A's beta is greater than stock B's beta by 0.65, what is the expected market risk premium? (Do not round intermediate calculations. Round the final answer to 2 decimal places.) Expected market risk premiumarrow_forwardSuppose your expectations regarding the stock price are as follows: State of the Market Probability Ending Price HPR (including dividends) Boom 0.35 $140 44.5% Normal growth 0.30 110 14.0 Recession 0.35 80 -16.5 Use the following equations to compute the mean and standard deviation of the HPR on stocks:arrow_forwardScenario Analysis. The common stock of Escapist sells for $25 a share and offers the following payoffs next year: Probability Dividend Stock Price Boom .3 $0 $18 Normal economy Recession .5 1 26 .2 3 34 Calculate the expected return and standard deviation of Escapist. Then calculate the expected return and standard deviation of a portfolio half invested in Escapist and half in Leaning Tower of Pita (from portfolio standard deviation is lower than either stock's. Explain why this happens. (LO3) problem 14). Show that thearrow_forward

- Suppose your expectations regarding the stock price are as follows: HPR (including dividends) State of the Market Boom Normal growth Recession Probability Ending Price 0.35 0.30 0.35 Mean Standard deviation Use the equations E (r) = Ep (s) r(s) and o² = Ep (s) [r(s) – E(r)]² to compute the mean and standard deviation of the HPR S S on stocks. Note: Do not round intermediate calculations. Round your answers to 2 decimal places. do do $ 140 110 80 % 44.5% 14.0 -16.5 %arrow_forward(Expected return and standard deviation) What is the expected return and standard devia- tion of the return for the next year on a stock that is selling for $30 now and has probabil- ities of 0.2, 0.6, and 0.2 of selling one year from now at $24, $33, and $39, respectively? Assume that no dividends will be paid on the stock during the next year and ignore taxes?arrow_forward6. The stock of Business Adventures sells for $40 a share. Its likely dividend payout and end-of-year price depend on the state of the economy by the end of the year as follows: (LO 5-2) Boom Normal economy Recession Dividend $2.00 1.00 0.50 Stock Price $50 43 34 a. Calculate the expected holding-period return and standard deviation of the holding-period return. All three scenarios are equally likely. b. Calculate the expected return and standard deviation of a portfolio invested half in Business Adventures and half in Treasury bills. The return on bills is 4%.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education