ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

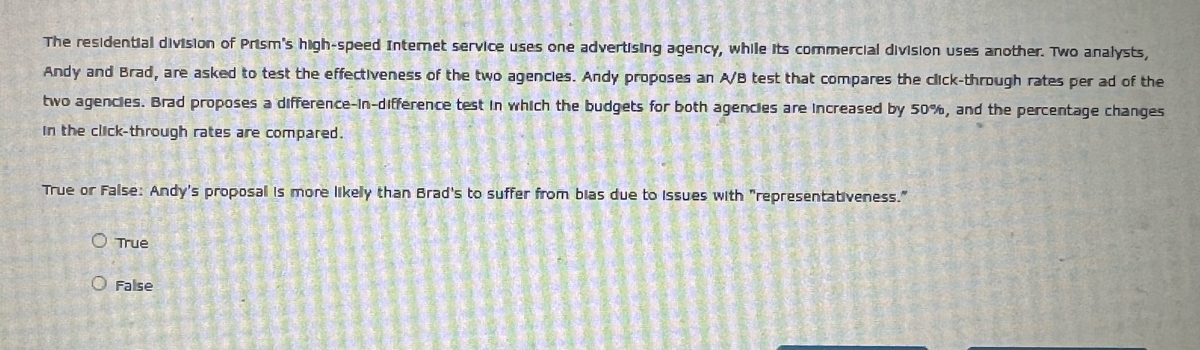

Transcribed Image Text:The residential division of Prism's high-speed Internet service uses one advertising agency, while its commercial division uses another. Two analysts,

Andy and Brad, are asked to test the effectiveness of the two agencies. Andy proposes an A/B test that compares the click-through rates per ad of the

two agendles. Brad proposes a difference-In-difference test in which the budgets for both agencies are increased by 50%, and the percentage changes

in the click-through rates are compared.

True or False: Andy's proposal is more likely than Brad's to suffer from blas due to issues with "representativeness."

True

False

2017-

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- I need solution to only part b)arrow_forwardProblem 2. (SW 12.8.) Consider a product market with a supply function Q₁ =B₁ + B₁P₁ + už, a demand function Q 7o+u, and an equilibrium condition Q = Q, where u and u are mutually independent i.i.d. random variables, both with a mean of 0. = (a) Show that P; and us are correlated. (b) Show that the OLS estimator of 3₁ is inconsistent. Hint: The standard strategy for showing inconsistency: first, argue that ₁ will Var(P) converge in large samples to Co(P), second, use OLS calculations to show that Cov(Q³,P) # B₁. Var(P) (c) How would you estimate Bo, B₁, and %0?arrow_forwardFour companies (Firm 1, 2, 3 and 4) are producing a product for the market. Each company will decide the number of products produced. You are given that • . Each firm can choose its qi. Given the quantites produced by four companies (denoted by 91, 92, 93, 94 respectively), the market price of the product is P = 400 - 91-92-93 - 94. Cost of producing one product is 20 (*Note: So the total cost for producing qi units of product is 20qi. Firm 1 and Firm 2 will first decide the quantities produced simultaneously at the beginning. After knowing 91 and 92, Firm 3 and Firm 4 will decide the quantities produced simultaneously. (a) State the strategic profiles of each firm. (b) Find all possible subgame perfect equilibrium for this games. Provide full justification to your answer.arrow_forward

- Next Friday, you plan to sell cakes at a bake sale to raise money for your school. You plan to charge $30 per cake, and you anticipate that you will sell 10 cakes. You can either purchase cakes to sell or bake them yourself. If you purchase the cakes, they will cost $25 each. If you bake your own cakes, your cost depends upon the number of cakes you bake, as shown in the table below. Number of cakes you bake Total cost of baked cakes ($) 0 0 1 10 2 22 3 36 4 52 5 70 6 90 7 112 8 136 9 162 10 190 a) How many cakes should you bake? How many cakes should you purchase? Bake ___ cake(s) and purchase ___ cake(s). b) Given your answer to part a, how much in total will the 10 cakes cost you? $ c) How much would it have cost you to bake all 10 cakes? $ d) How much would it have cost you to purchase all 10 cakes? $arrow_forwardWhat is the approximate value of Annie’s brand/store compared to Sam’s for an otherwise equal apple tree? What is the estimate for market share for Annie if she sells Gal Apple Trees at $15.95 vs. Sam selling golden Delicious trees at $24.95.?arrow_forwardThe Red Lobster (RL) restaurant chain has been using two seafood vendors for lobster: Cape Cod Fisheries (CCF) and Maine's Best. Lobsters from CCF averaged $2.20/pound last year while Maine's Best averaged $3.33/lb. While quality has been good from both vendors, CCF continually delivers late and RL has to pay the dock employees overtime to accept deliveries. Last year's overtime costs were $50,000. RL purchased a total of 100,000 lbs. last year from CCF. Calculate the Supplier Performance Index (SPI) for CCF. А.) 2.20 B.) Not enough info available С.) 1.23 D.) 1.33 Е.) 1.05arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education