ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

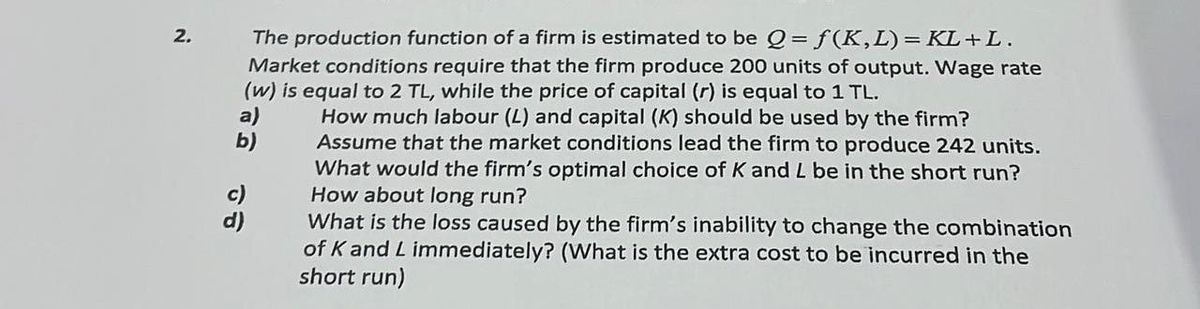

Transcribed Image Text:2.

The production function of a firm is estimated to be Q=f(K, L) = KL+ L.

Market conditions require that the firm produce 200 units of output. Wage rate

(w) is equal to 2 TL, while the price of capital (r) is equal to 1 TL.

How much labour (L) and capital (K) should be used by the firm?

Assume that the market conditions lead the firm to produce 242 units.

What would the firm's optimal choice of K and L be in the short run?

How about long run?

What is the loss caused by the firm's inability to change the combination

of K and L immediately? (What is the extra cost to be incurred in the

short run)

a)

b)

c)

d)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 5 steps with 9 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A firm faces a production function with inputs capital (K) and labor (L): F(K, L) = K¹/² L¹/4 The amount of capital used for production is determined at the beginning of the year. The prices of K and L are v and w respectively.arrow_forwardc) Give a formal definition of increasing, decreasing, and constant returns to sale, and determine if the production function above exhibits increasing, decreasing or constant returns to scale. (d) Derive the firm’s contingent labor demand function (e) Derive the firm’s unconditional labor demand function (f) Derive the profit function of the firmarrow_forwardProduction function is Z = 2L+10K where Z represents the amount of output produced, L = labour hired, and K = units of capital hired. The wage rate per unit of labour is $10 and the rental rate per unit of capital is $20. For 200 units what will be the minimum total cost of production?arrow_forward

- If a firm has the production function q = f(L, K) = L + 2K, then its technology exhibits: constant returns to scale increasing returns to scale None of the above. decreasing returns to scale increasing marginal productarrow_forwardCatalina Films produces video shorts using digital editing equipment (K) and editors (L). The firm has the production function Q(K, L)=KxL, where Q is the hours of edited footage. The wage is $25, and the rental rate of capital is $50. The firm wants to produce 3,000 units of output at the lowest possible cost.a) Find the marginal product of each input.b) Determine whether the production function exhibits diminishing marginal product to each input.c) Find the marginal rate of technical substitution(MRTSLK)d) How does MRTSLK change as more L, is used holding output constant.e) Find the least costly combination of labor and capital to produce 3000 unitsarrow_forwardAll of these statements about the production function are true EXCEPT a) the curve features 3 distinct regions: increasing returns to scale, constant returns to scale, and diminishing returns to scale. b)the curve's shape matches and its description of the interaction between the graph's axes represents the law of diminishing returns c) it can be applied to many economic markets d) one variation is used to show the difference between firm and market specific riskarrow_forward

- Consider the production function: Y = z.f(K,N,L) where Y is output, z is a parameter capturing technology, K is capital, N is labour and L is the area of land.arrow_forwardA firm’s short-run production function is in the form of q = aLK +(bL^2)K −(cL^3)K , wherea, b, c > 0 are parameters. K is a constant. (a) Derive the marginal product of labor.(b) Find the level of L, expressed in terms of the parameters, at which the law ofdiminishing marginal product kicks in.arrow_forwardA firm’s production function is - y = f(X1, X2)= X11/2 + X1X2 , Where X1≥0, X2≥0 1. Find its returns to scale when X1=1, and X2=1arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education