ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

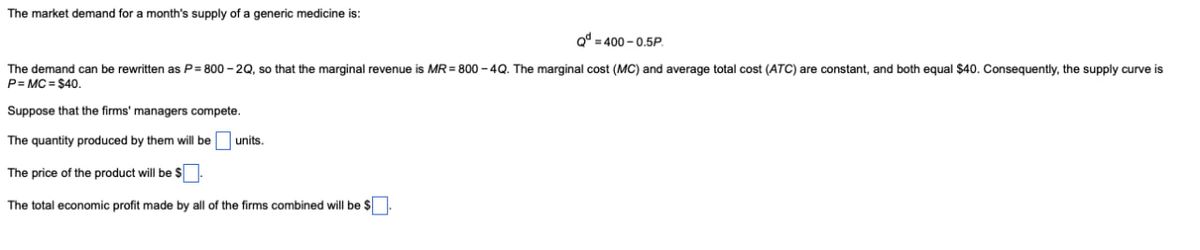

Transcribed Image Text:The market demand for a month's supply of a generic medicine is:

Q = 400-0.5P.

The demand can be rewritten as P= 800-2Q, so that the marginal revenue is MR = 800-4Q. The marginal cost (MC) and average total cost (ATC) are constant, and both equal $40. Consequently, the supply curve is

P=MC = $40.

Suppose that the firms' managers compete.

The quantity produced by them will be ☐ units.

The price of the product will be $

The total economic profit made by all of the firms combined will be $

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Similar questions

- Consider the following problem: Demand: q = 100-p Retailer: marginal cost of selling r = 10 per unit Manufacturer: marginal cost of producing = 40 per unit Neither firm faces any competitor Suppose now that the retailer and the manufacturer are separate firms. Write down the profit function of the manufacturer if it sells to the retailer at w. You solved for the quantity the manufacturer will sell a minute ago, so you can use that in the profit function, and then you will have a profit function for the manufacturer that does not have p, but only has w in it. Solve for the optimal w for the manufacturer to charge and calculate the quantitysold under that w.arrow_forwardThe Broadway show Hamilton is coming to perform for one night. There are two types of consumers interested in the show- current students and rich alumni. The demand curve for the student market is Q= 300-0.4P with marginal revenue MR= 750-5Q. The demand curve for the alumni market segment is Q=600-0.1P with marginal revenue MR=6000-20Q. If the two types of consumers are in the market, the MR=1800-4Q. The cost function is C(Q)=200Q and the marginal cost of serving either customer is MC=200. 1. Assume the show knows there are different types of consumers but can not tell the difference so they must sell tickets at a single price. At what price do all consumers enter the market? What profit-maximizing price and quantity are the tickets sold at?arrow_forwardCareRight Medical Company has invented and received a patent for a new drug to treat a rare and fatal disease. It charges $5,000 for a year’s supply of the drug. Critics claim that this amount is excessive, as it does not cost that much to produce. They believe the company is taking advantage of sick people. CareRight responds that they are losing money on this drug. The critics are right: It does not cost CareRight $5,000 to produce a year’s supply for one person. However, CareRight’s statement is also correct in that they are losing money on the drug. How can both statements be true? Consider the different types of costs in your answer.arrow_forward

- Imagine that the cell-phone market is made up of one large firm that leads the industry and sets its own price first, while smaller firms in the industry follow. There are 20 such smaller firms, each with a supply function of q; = 67.50 + for i = 1,2, ..., 20 firms, while pis the per-unit price. Total market demand for cell phones is given by the function Q = 6, 700.00 – p. If the cost function for the leading firm is CL(qL) = 109L, calculate the following values: %3D Leading firm's production: q1 = (Round to two decimals if necessary.) Total follower firm production: qF = (Round to two decimals if necessary.) Equilibrium price: p = $ (Round to two decimals if necessary.)arrow_forwardAVAC is the only pharmaceutical firm producing a Vaccine. The Demand Curve for its product is Qd = 250 – 50 P where P is Price and Q are packs of vaccines in ‘000 Total Cost Function estimated by the firm is TC = 15 + 0.5Q where Q is monthly output. What is the market structure of AVAC? State its characteristics. To maximize profit, What will be the optimum price and how many packs of Vaccine should the firm produce and sell per month? If this number of packs is produced and sold, what will be the firm’s monthly profit? Using available information, draw AVAC’s demand, marginal revenue and marginal cost curves in a graph and clearly label thefirm’s profit maximizing price, quantity and profit. Do you observe any welfare loss? If so, also indicate and label the area on the graph. Assume all other pharmaceutical firms in the market start producing the Vaccine and the market becomes competitive. What will be the impact on…arrow_forwardAssume that you are an economic consultant. The firm that hired you has provided the information below. The firm is a price searcher and wants to maximize its profit (or minimize its loss). InformationPrice: $4Elasticity of demand at price of $4 is Ed=-1Quantity of output: 2000Total variable cost: 4000Average fixed cost: 1Marginal cost is constant and equal to the average variable cost: MC=ACV=2. Which of the following answers correctly describes this case? a) The firm is maximizing profits at the current price of $4.b) The firm should increase price and reduce quantity produced.c) None of the other answersd) Firm should reduce price and increase quantity produced.arrow_forward

- A new restaurant – Uovo – has just opened in West L.A. It is serving the upscale market, with truly outstanding pasta that is flown in overnight from Bologna, Italy. Uovo offers a fixed-price menu with appetizer, three dishes of pasta, and a delicious tiramisu for dessert. The restaurant faces the following demand function: Q = 600 - 4P where Q is the number of guests per day. The marginal cost is constant at $50 per customer (including expenses for ingredients and personnel). The restaurant is paying a rent of $2,000 per day. What is the profit-maximizing number of guests that Uovo should serve each day, and what price should Uovo charge to maximize profit? What is the elasticity of demand at the optimal price and quantity? Is demand elastic or inelastic at this point? From what we learned in class, does it make sense for the restaurant to operate in this area of the demand curve (elastic/inelastic part)? What is the profit of the restaurant at the optimal price and quantity, and what…arrow_forwardThe Broadway show Hamilton is coming to perform for one night. There are two types of consumers interested in the show- current students and rich alumni. The demand curve for the student market is Q= 300-0.4P with marginal revenue MR= 750-5Q. The demand curve for the alumni market segment is Q=600-0.1P with marginal revenue MR=6000-20Q. If the two types of consumers are in the market, the MR=1800-4Q. The cost function is C(Q)=200Q and the marginal cost of serving either customer is MC=200. 2. How much total consumer surplus is generated?arrow_forwardA store estimates is customer inverse demand is P= 6.1 - 2.6Q, and the marginal cost of each rental is $0.48. If they use block pricing, what should the price be for the entire package?arrow_forward

- *1 A small village has only one Italian restaurant. The daily demand for dinners in this restaurant is P=120-2Q, where P is the price in £ and Q is the number of dinners. It has a fixed cost of £300 and a marginal cost of £10 for the first 15 dinners. If it wants to produce more than 15 dinners, it must pay overtime wages to its workers, with the marginal cost rising to £20. What is the maximum amount of profit the restaurant can earn? Illustrate your answer on a diagram.arrow_forwardSuppose a competitive market with the inverse demand p=100–2q. The pre-innovation marginal cost is constant at 60. A process innovation reduces the marginal cost to 28. A) Show this is a non-drastic innovation. B) Determine the minimal reduction in marginal cost for the innovation to be drastic.arrow_forwardA city has two newspapers. Demand for either paper depends on its own price and the price of its rival. Demand functions for papers A and B respectively, measured in tens of thousands of subscriptions, are 21-2Pa + Pb and 21 + Pa-2Pb The marginal cost of printing and distributing an extra paper just equals the extra advertising revenue one gets from another reader, so each paper treats marginal costs as zero. Each paper maximizes its revenue assuming that the other's price is independent of its own choice of price. If the papers enter a joint operating agreement where they set prices to maximize total revenue, by how much will newspaper prices rise? (a) 3 (b) 2 (c) 0 (d) 3.5 (e) 2.5arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education