ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:Home - » Students

MyLab Economics Homework -

P Do Homework - 2-1 MyEconLab: x

+

Ô https://www.mathxl.com/Student/PlayerHomework.aspx?homeworkld=59...

...

Navy Federal Credit.

Walt Disney World...

* Google Hangouts

>

Other favorites

Cruises & Vacations...

IMDB - Movies, TV.

MBA-502-Q3789 Economics for Business 21TW3

Amy McAllister & 02/22/21 2:01 PM

Homework: 2-1 MyEconLab: Module Two Homework

Save

Score: 0 of 2 pts

25 of 25 (16 complete)

HW Score: 55.9%, 36.33 of 65 pts

Concept Question 5.13

Question Help

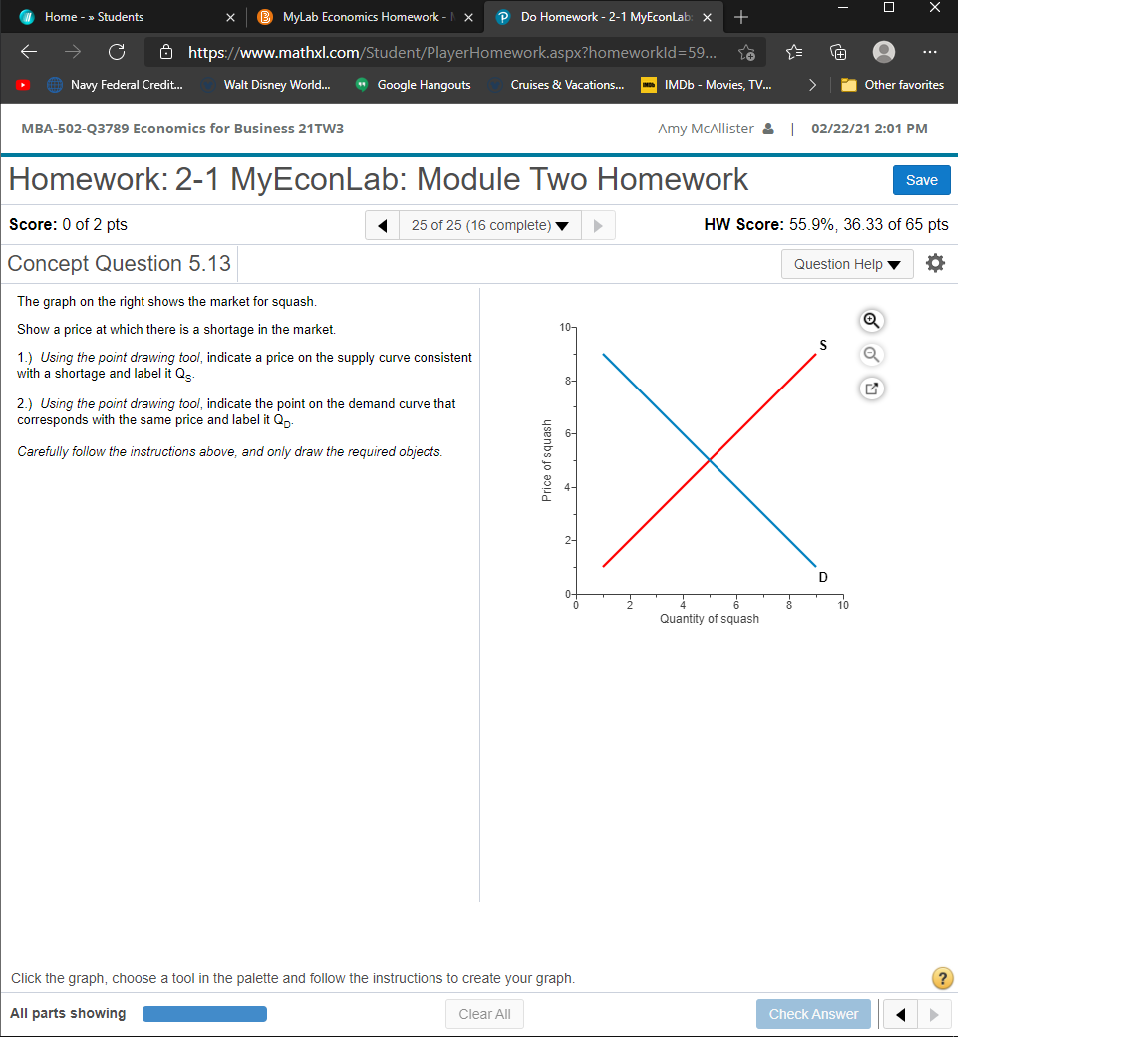

The graph on the right shows the market for squash.

Show a price at which there is a shortage in the market.

10-

1.) Using the point drawing tool, indicate a price on the supply curve consistent

with a shortage and label it Qs.

2.) Using the point drawing tool, indicate the point on the demand curve that

corresponds with the same price and label it Qn:

Carefully follow the instructions above, and only draw the required objects.

D

10

Quantity of squash

Click the graph, choose a tool in the palette and follow the instructions to create your graph.

All parts showing

Clear All

Check Answer

Price of squash

Expert Solution

arrow_forward

Step 1

A shortage occurs when the quantity demanded is greater than the quantity supplied. Prices below the equilibrium are the ones where shortage occurs.

From the graph, we can see that the equilibrium price is $5 and the equilibrium quantity 5units of squash.

If the price is below $5, the shortage will occur. It is also called excess demand. So, we are taking price=$4 at which shortage occurs. At this point, 7 units of quantity are demanded but the quantity supplied is only 4 units.

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Incorrect option too explainarrow_forwardFor each of the following articles below, analyze the impact of a change in demand or a change in supply or both (or it may not necessarily illustrate a change) on price equilibrium price, market price) for the good under consideration and draw the appropriate graph for each article. Use D., S.. P., and O. to symbolize initial demand, supply, equilibrium price and quantity respectively. Use D,, S., P., and Q, to represent the new demand, supply, equilibrium price and quantity respectively Slaughter rates dropped in 2019 because of low farm gate prices and weak pork demand, which contributed to a decline in 2019 swine meat production (plg333.com. March 26, 2020)arrow_forward24 of 100 Suppose that there is a freeze in California that damages the avocado crop. The effect on the market for avocados will be a in the equilibrium price. of the supply curve and a(n). DOOO leftward shift; decrease leftward shift; increase a rightward shift; increase rightward shift; decreasearrow_forward

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education