ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

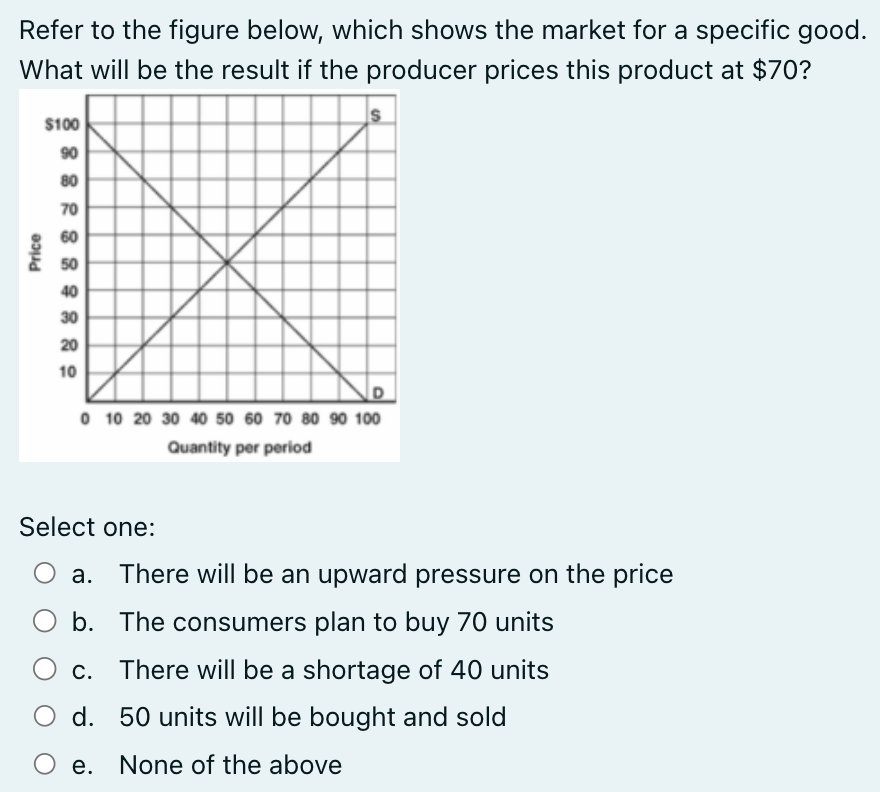

Transcribed Image Text:Refer to the figure below, which shows the market for a specific good.

What will be the result if the producer prices this product at $70?

Price

$100

90

80

70

60

50

40

30

20

10

0 10 20 30 40 50 60 70 80 90 100

Quantity per period

Select one:

There will be an upward pressure on the price

b. The consumers plan to buy 70 units

There will be a shortage of 40 units

d. 50 units will be bought and sold

None of the above

O e.

a.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Refer to the above graph, which shows the market for beef where demand shifted from D₁ to D₂. The change in equilibrium from E, to E, cannot be a result of Multiple Choice a health report warning of the dangers of beef consumption a decrease in the productivity of cattle farms. buyers' expectations of lower prices for beef in the very near future. a widespread concern about mad - cow disease. Price Per Pound Nº a E2 Q₂ Quantity UT Supply D₂ 3 Refer to the above graph, which shows the market for beef where demand shifted from D₁ to D₂. The change in equilibrium from E₁ to E2 cannot be a result ofarrow_forwardA taco hut is trying to determine its demand if it changes it's price. In 2019, they sold tacos for 1.00 and sold 6,000. In 2020, they increase the price of tacos to 1.50 and demand dropped to 5,500. In 2021, the owners of the taco hut want to increase taco price to 2.00 dollars. What would demand be for 2021? What if they lowered the price to .50, how much would demand be?arrow_forwardThe demand and supply curves for a product are given by: Qd = 600 - 2P Qs = 300 + 4P Find the equilibrium price and the equilibrium quantity. Carefully draw a graph to illustrate your answer. Make sure to write out the intercepts. Show the equilibrium price and the equilibrium quantity on your graph.arrow_forward

- Step 1: Fill in the appropriate values for original quantity, new quantity, original price, and new price. Step 2: Calculate the average quantity by adding the original quantity and the new quantity, and then dividing by two. Do the same for the average price. Step 3: Calculate the change in quantity by subtracting the original quantity from the new quantity. Do the same for the change in price. Step 4: Calculate the percentage change in quantity demanded by dividing the change in quantity by the average quantity. Do the same to calculate the percentage change in price. Step 5: Calculate the price elasticity of demand by dividing the percentage change in quantity demanded by the percentage change in price, ignoring the negative sign. Using the midpoint method, the elasticity of demand for headsets is about (.44/1.14/2.28/4.56)arrow_forwardWhat would cause an increase in quantity demanded?arrow_forwardCombine parts 1 and 2. Suppose that the FDA increase regulation of coffee, and a reputable study is published indicating that coffee drinkers have higher rates of Alzheimer’s. What with the combined impact have on the equilibrium price and quantity of coffee? Explain your reasoning and show graphically. Make sure you think this through carefully!arrow_forward

- Which of the following is one of the factors determining if demand for a good is price elastic or price inelastic? Select one: a. The cost of the resources used in producing the good. b. The relative share of the budget spent on the good. c. Whether the good is a substitute or a complement. d. Whether the good is imported or exported.arrow_forwardDraw a demand and supply graph, label all axes, and the equilibrium price and quantity. Once you have done this draw what would happen if there was a decrease in the number of buyers in the marketarrow_forwardIn this market there will be an excess supply of 1000 gardenburgers at a price of 2. If the price per garden burger is $6 there is aarrow_forward

- Price Refer to the below diagram, which shows demand and supply conditions in the competitive market for product X. A shift in the demand curve from D, to Do might be caused by B C Quantity O a decline in the number of buyers in the market. a decline in the price of a substitute good. an increase in incomes if the product is a normal good. an increase in incomes if the product is an inferior good.arrow_forwardConsider the weekly supply of gasoline in Figure 1. How much gasoline will producers wish to sell if the price of a gallon of gasoline is $1.20? A) 100K gallons b) 140K gallons C) 236K gallons D) 308K gallonsarrow_forwardThe task I am struggling with. Thank you.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education