ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

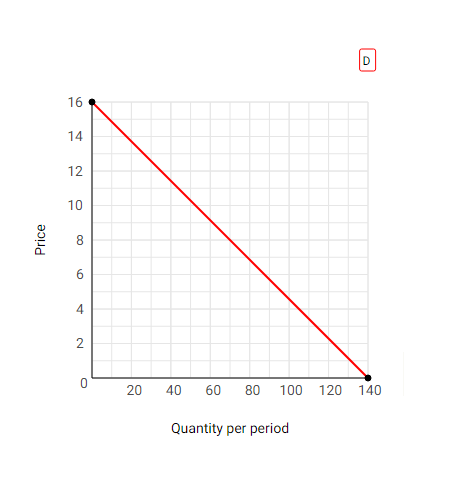

The graph below shows the daily demand curve for fresh spring water in a remote mountain village in the land of Far Country. The only spring is controlled by the village chief who earns revenue from the sale of water in order to cover the costs of running the village. The villagers bring their own jugs and pay a price per jug as they leave.

a. What quantity of jugs would be sold each day in order to maximize his total revenue?

Quantity:

b. What price would the chief charge?

Price: $

c. What is MR at this price and quantity?

MR:

d. Assuming no marginal costs, what price would the chief charge in order to maximize his total profits?

Price: $

Transcribed Image Text:16

14

12

10

6.

4

2

20

40

60

80

100 120 140

Quantity per period

Price

Co

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Every House in a small town has a well that provides water at no cost. However, if the town wants more than 10,000 gallons a day, it has to buy extra water from firms located outside of the town. The town currently consumes 9,000 gallons per day. a. Draw a linear demand curve b. The firm's supply curve is linear and starts at the origin. Draw the market supply curve, which includes the supply from the town's well. c. Show the equilibrium. What is the equilibrium quantity? What is the equilibrium price? Explain Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwarddo fast i will 5 upvotes.arrow_forwarda) Draw a graph with supply and demand curves that intersect and establish a market equilibrium price of $10 per unit and equilibrium market quantity of 100 units. Be sure to label your graph completely.arrow_forward

- The following graph illustrates the weekly demand curve for motorized scooters in Roanoke. Use the green rectangle (triangle symbols) to compute total revenue at various prices along the demand curve. Note: You will not be graded on any changes made to this graph. PRICE (Dollars per scooter) 300 275 250 200 175 150 125 100 75 50 0 0 + 3 6 9 x 4 * B Demand 12 15 18 21 24 27 QUANTITY (Scooters) 30 33 36 39 Total Revenue ?arrow_forwardWrite down the factors affecting demand. Which of the following factors will cause the following products to increase or decrease? Convenience food (sold in food shops and supermarkets) Products purchased in the internet Mobile phones Pay-per - view- television programming Books Airline travel within Us; air travel with UKarrow_forwardOnly one thing can cause movement along a product’s demand curve --- that is, cause a change in quantity demanded for that product --- and that’s a change in that product’s price. On the other hand, there are five key variables that can cause a product’s demand curve to shift to the left or right --- that is, lead to a change in demand. Coca-Cola is experiencing shifts in the U.S. demand curve for its famous cola soft drink, as the huge post-World War II “Baby Boom” generation has aged beyond their prime soft drink consumption years, and as the smaller generations behind the Baby Boomers have been buying relatively more energy drinks, water, juice, and tea, and relatively less soda than previous generations. What two key variables are affecting demand for Coca-Cola in the U.S., and in which direction are these variables shifting the demand curve for Coke?arrow_forward

- Paulina sells beef in a competitive market where the price is $8 per pound. Her total revenue and total costs are given in the table below. Quantity of Total revenue Total cost beef (lb.) 0 1 2 3 4 ($) 0 8 16 24 32 ($) 4 8 13 19 27 Profit ($) 0 8 pounds Marginal revenue ($) c. What is the profit-maximizing (or loss-minimizing) quantity? Marginal Marginal cost ($) profit ($) a. Complete the table. Instructions: Enter your answers as a whole number. If you are entering any negative numbers be sure to include a negative sign (-) in front of those numbers. b. At what quantity does marginal revenue equal marginal cost? pounds Aarrow_forwardExplain why the following might be true: A drought in the Caribbean raises the total revenue that producers receive from the sale of coffee, but a drought only in Grenada reduces the total revenue that Grenadian producers receive.arrow_forwardHow Should Demand be Managed when Price is Zero? Foodbanks During the COVID-19 Eraarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education