FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

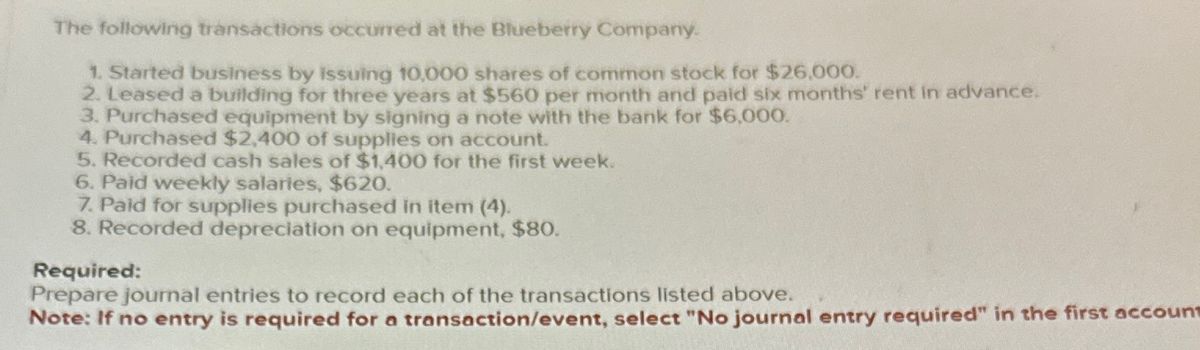

Transcribed Image Text:The following transactions occurred at the Blueberry Company.

1. Started business by issuing 10,000 shares of common stock for $26.000.

2. Leased a building for three years at $560 per month and paid six months' rent in advance.

3. Purchased equipment by signing a note with the bank for $6,000.

4. Purchased $2,400 of supplies on account.

5. Recorded cash sales of $1,400 for the first week.

6. Paid weekly salaries, $620.

7. Paid for supplies purchased in item (4).

8. Recorded depreciation on equipment, $80.

Required:

Prepare journal entries to record each of the transactions listed above.

Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 1 steps

Knowledge Booster

Similar questions

- The following transactions apply to Ozark Sales for Year 1: The business was started when the company received $48,000 from the issue of common stock. Purchased merchandise inventory of $176,000 on account. Sold merchandise for $202,000 cash (not including sales tax). Sales tax of 7 percent is collected when the merchandise is sold. The merchandise had a cost of $127,000. Provided a six-month warranty on the merchandise sold. Based on industry estimates, the warranty claims would amount to 4 percent of sales. Paid the sales tax to the state agency on $152,000 of the sales. On September 1, Year 1, borrowed $21,500 from the local bank. The note had a 5 percent interest rate and matured on March 1, Year 2. Paid $6,000 for warranty repairs during the year. Paid operating expenses of $55,500 for the year. Paid $124,300 of accounts payable. Recorded accrued interest on the note issued in transaction number 6. b1. Prepare the journal entries for the preceding transactions.b2. Post…arrow_forwardManjiarrow_forwardThe following transactions apply to Ozark Sales for Year 1: The business was started when the company received $50,000 from the issue of common stock. Purchased equipment inventory of $178,000 on account. Sold equipment for $192,000 cash (not including sales tax). Sales tax of 6 percent is collected when the merchandise is sold. The merchandise had a cost of $117,000. Provided a six-month warranty on the equipment sold. Based on industry estimates, the warranty claims would amount to 5 percent of sales. Paid the sales tax to the state agency on $142,000 of the sales. On September 1, Year 1, borrowed $21,500 from the local bank. The note had a 6 percent interest rate and matured on March 1, Year 2. Paid $5,900 for warranty repairs during the year. Paid operating expenses of $56,000 for the year. Paid $124,000 of accounts payable. Recorded accrued interest on the note issued in transaction no. 6. Required Record the given transactions in a horizontal statements model. Prepare the…arrow_forward

- Line following information applies to the questions displayed below.j The following transactions apply to Park Company for Year 1: 1. Received $31,000 cash from the issue of common stock. 2. Purchased inventory on account for $143,000. 3. Sold inventory for $172,500 cash that had cost $105,500. Sales tax was collected at the rate of 8 percent on the inventory sold. 4. Borrowed $24,000 from First State Bank on March 1, Year 1. The note had a 8 percent interest rate and a one-year term to maturity. 5. Paid the accounts payable (see transaction 2). 6. Paid the sales tax due on $153,500 of sales. Sales tax on the other $19,000 is not due until after the end of the year. 7. Salaries for the year for one employee amounted to $28,000. Assume the Social Security tax rate is 6 percent and the Medicare tax rate is 1.5 percent. Federal income tax withheld was $5,300. 8. Paid $2,600 for warranty repairs during the year. 9. Paid $12,000 of other operating expenses during the year. 10. Paid a…arrow_forwardprepare journal entries and T-accountarrow_forwardOn June 30, Year 3, Franklin Company's total current assets were $500,500 and its total current liabilities were $275,500. On July 1, Year 3, Franklin issued a short-term note to a bank for $39,400 cash. Required a. Compute Franklin's working capital before and after issuing the note. b. Compute Franklin's current ratio before and after issuing the note. (Round your answers to 2 decimal places.) a. Working capital b. Current ratio Before the transaction After the transactionarrow_forward

- ASSETS Current assets: Cash MANGO INC.. CONSOLIDATED BALANCE SHEET September 30, 2017 (dollars in millions) Short-term investments Accounts receivable Inventories Other current assets Total current assets Long-term investments Property, plant, and equipment, net Other noncurrent assets Total assets LIABILITIES AND STOCKHOLDERS' EQUITY Current Liabilities: Accounts payable Accrued expenses Unearned revenue. Short-term notes payable Total current liabilities Long-term debt Other noncurrent liabilities Total liabilities. Stockholders' equity: Common stock ($0.00001 per value) Additional paid-in capital Retained earnings Total stockholders' equity Total liabilities and shareholders' equity Assume that the following transactions fin $ 14,024 11,377 17,681 2,134 24,141 69,357 131,732 20,873 12,676 $234,638 $ 30,563 18,679 8,599 6,385 64,226 29,344 28,196 121,766 1 25,212 87,659 112,872 $234,638arrow_forwardCreate journal entries for each of the following transactions The company issues capital stock for $90,000. The company borrows $40,000 from the bank. The company pays its rent for one year in advance, $18,000. The company buys inventory for $30,000 on account. The company sells inventory costing $20,000 for $40,000 on account. The company pays its employees $1,000 for services rendered. The company buys inventory for $50,000 cash. The company sells inventory costing $40,000 for $80,000 cash. The company collects $20,000 from customers on account. The company pays $25,000 on account. One month of rent has expired. Dividends of $2,000 are paid.arrow_forwardWHAT IS THE INCOME STATEMENT FOR THE FOLLOWING During its first month of operation, the Quick Tax Corporation, which specializes in tax preparation, completed the following transactions. July 1 Began business by making a deposit in a company bank account of $60,000, in exchange for 6,000 shares of $10 par value common stock. July 3 Paid the current month's rent, $3,500 July 5 Paid the premium on a 1-year insurance policy, $4,200 July 7 Purchased supplies on account from Little Company, $1,000. July 10 Paid employee salaries, $3,500 July 14 Purchased equipment from Lake Company, $10,000. Paid $2,500 down and the balance was placed on account. Payments will be $500.00 per month until the equipment is paid. The first payment is due 8/1. Note: Use accounts payable for the balance due. July 15 Received cash for preparing tax returns for the first half of July, $8,000 July 19 Made payment on account to Lake Company, $500. July 31 Received cash for preparing tax returns for the last half of…arrow_forward

- Following are the transactions of JonesSpa Corporation, for the month of January. a Borrowed $30,000 from a local bank; the loan is due in 9 months. b. Lent $10,000 to an affiliate; accepted a note due in one year. c. Sold to investors 100 additional shares of stock with a par value of $0.10 per share and a market price of $5 per share; received cash. d. Purchased $15,000 of equipment, paying $5,000 cash and signing a note for the rest due in one year. e. Declared $2,000 in cash dividends to stockholders, to be paid in February. Prepare the journal entry to record each of the above transactions for the month of January, Note: If no entry is required for a transaction/event, select "No journal entry required" in the first account field. View transaction list Journal entry worksheet Record the receipt of the bank loan of $30,000. Note: Enter debits before credits Transaction 5 Record entry General Journal Clear entry Debit Credit View general journalarrow_forward"Marquis Smith started IT Consulting Services Incorporated on January 1, Year 1. The company experienced the following events during its first year of operation 1 On June 1 Year 1, the company borrowed $21.600 cash from the bank. The note had a one-year term and 6% annual interest rate 2. On December 31. Year 1, the company adjusted the accounting records to recognize accrued interest expense on the bank note Required: Use a horizontal financial statements model to show how each event affects the balance sheet, income statement, and statement of cash flows More specifically, record the amounts of the events into the model. Also, in the Statement of Cash Flows column, classify the cash flows as operating activities (OA), investing activities (IA), or financing activities (FA) Note: Enter any decreases to account balances and cash outflows with a minus sign. Leave cells blank if no input is needed. Event Number Assets Cash 21 600 2 Total CNet change in cash 01 21.600 Notes Payable 21,600…arrow_forwardAssume that the following transactions (in millions) occurred during the next fiscal year (ending on September 26, 2020): Borrowed $18,279 from banks due in two years. Purchased additional investments for $22,200 cash; one-fifth were long term and the rest were short term. Purchased property, plant, and equipment; paid $9,584 in cash and signed a short-term note for $1,422. Issued additional shares of common stock for $1,481 in cash; total par value was $1 and the rest was in excess of par value. Sold short-term investments costing $19,021 for $19,021 cash. Declared $11,138 in dividends to be paid at the beginning of the next fiscal year. Prepare a classified balance sheet for Orange at September 26, 2020, based on these transactions. please complete this with working and show how did you get the number with other work answer in text thanksarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education