Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

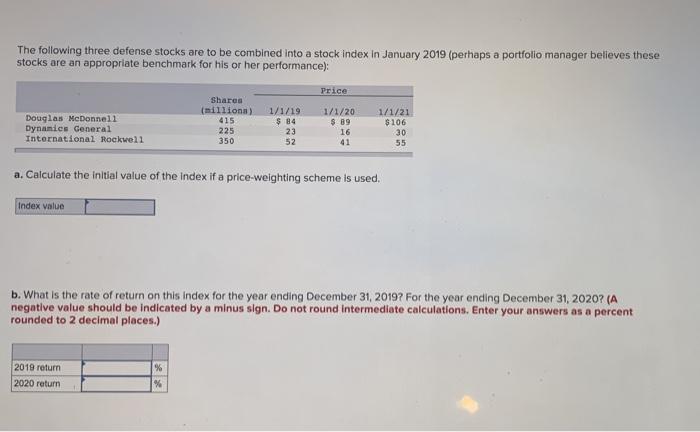

Transcribed Image Text:The following three defense stocks are to be combined into a stock index in January 2019 (perhaps a portfolio manager believes these

stocks are an appropriate benchmark for his or her performance):

Douglas McDonnell

Dynamics General

International Rockwell

Index value

2019 return

2020 return

Shares

(millions)

415

225

350

%

1/1/19

$84

23

52

a. Calculate the initial value of the index if a price-weighting scheme is used.

%

Price

1/1/20

$ 89

16

41

1/1/21

$106

b. What is the rate of return on this index for the year ending December 31, 2019? For the year ending December 31, 2020? (A

negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent

rounded to 2 decimal places.)

30

55

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 6 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The following information is related to X corporation: X's Beta was 1.3, market index 1 January 2020 was 100, market index 31 December 2020 was 110 and interest on treasury bills was 0.03 (risk free). Stock returns using the capital assets pricing model Question 20Answer a. 0.132 b. 0.143 c. 0.112 d. 0.121arrow_forwardYou are given the following information about the stock of Company ABC: Share price $80 risk free rate of interest is 6%, time to expiration is 6 months, annualised standard deviationis 0.5 and exercise price is $85. Calculate the appropriate call value of the stock according to the Black-Scholes option pricing formula. (Show your workings in full) Calculate an appropriate put premium. (Show your workings in full)arrow_forwardAn analyst gathered the following information for a stock and market parameters: stock beta= 1.08; • expected return on the Market = 11.97%; • expected return on T-bills = 1.55%; • current stock Price = $9.01; • expected stock price in one year = $11.14; • expected dividend payment next year = $3.23. Calculate the expected return for this stock. Please share your answer as a percentage rounded to 2 decimal places.arrow_forward

- The price of a stock was $45 at the beginning of 2019. If it showed a return of 8% at the end of 2019 and is projected to show a return of 14% at the end of 2020, what should the stock price be at the end of 2020?arrow_forwardGiven the following price and dividend information, calculate the lower bound to the 95th confidence interval. (Enter percentages as decimals and round to 4 decimals) Stock: MSFT Year Price Dividend 2017 $ 64.65 2018 $ 95.01 $ 1.72 2019 $ 104.43 $ 1.89 2020 $ 107.23 $ 2.09 2021 $231.96 $ 2.30 2022 $310.98 $ 2.54 2023 $247.81 $ 3.00arrow_forwardes The following three defense stocks are to be combined into a stock index in January 2022 (perhaps a portfolio manager believes these stocks are an appropriate benchmark for his or her performance): Douglas McDonnell Dynamics General International Rockwell Index value Shares (millions) 420 450 250 2022 return 2023 return a. Calculate the initial value of the index if a price-weighting scheme is used. 1/1/22 $ 63 53 82 Price 1/1/23 $ 67 47 71 % % b. What is the rate of return on this index for the year ending December 31, 2022? For the year ending December 31, 2023? Note: A negative value should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places. 1/1/24 $ 84 61 87arrow_forward

- Consider 2 stocks in the following table. We create a stock index of companies that make stuff for Spring Break. stocks PO Q0 P1 Q1 ABC, Inc. $850P0 150Q0 $ 830P1 150Q1 XYZ, Inc. $510P0 400Q0 $550P1 400Q1 What is the initial portfolio weight for stock ABC in a Price - weighted index of these two stocksarrow_forwardStocks A and B have the following historical returns: Year 2016 2017 2018 2019 2020 Stock A's Returns, ra (15.40%) 29.00 14.25 (5.00) 26.00 Stock B's Returns, ra (15.80%) 21.10 37.30 (6.20) 12.45 a. Calculate the average rate of return for each stock during the period 2016 through 2020. Round your answers to two decimal places. Stock A: Stock B: b. Assume that someone held a portfolio consisting of 50% of Stock A and 50% of Stock B. What would the realized rate of return on the portfolio have been each year Round your answers to two decimal places. Negative values should be indicated by a minus sign. Portfolio CV Year 2016 2017 2018 2019 2020 What would the average return on the portfolio have been during this period? Round your answer to two decimal places. % % % c. Calculate the standard deviation of returns for each stock and for the portfolio. Round your answers to two decimal places. Stock A Stock B Portfolio Standard Deviation d. Calculate the coefficient of variation for each…arrow_forwardHelp me pleasearrow_forward

- You are given the daily closing prices of a stock from Jan 1, 2018 to Jan 5, 2018: Date Stock price Jan 1 Jan 2 Jan 3 Jan 4 Jan 5 A 5.00 B 5.50 C 6.00 At the end of Jan 1, 2018, Jie purchased the following options that expire on Jan 5, 2018: (a) Arithmetic average strike Asian call option. (b) Up-and-in call option with a barrier of 110 and strike of 105. For both options, the underlying asset is the stock and the payoff is determined using the last 4 daily closing prices. Determine Jie's total payoff on Jan 5, 2018. D Possible Answers E 105 6.50 109 7.00 112 110 111arrow_forwardPlease answer fast I give you upvote.arrow_forwardConsider the following annual closing prices of stock A, values of market index (S&P 500) and Treasury bills rate. A B C с D Date Stock A Prices (in $) Market Index Value Risk Free Rate (in %) 2 Period 1 119 3 Period 2 100 11829 11843 9639 88 131 12854 9580 11640 8469 11412 9115 10682 NOSAWNH 1 4 Period 3 Period 4 6 Period 5 7 Period 6 8 Period 7 9 Period 8 10 Period 9 11 Period 10 12 O 1.1 13 What is the value of CAPM beta for stock A? O 1.4666 O 1.8333 O2.0533 82 113 O 0.3666 65 109 95 113 1.48 1.76 1.64 1.2 1.43 1.36 1.3 1.72 1.71 1.77arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education