ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

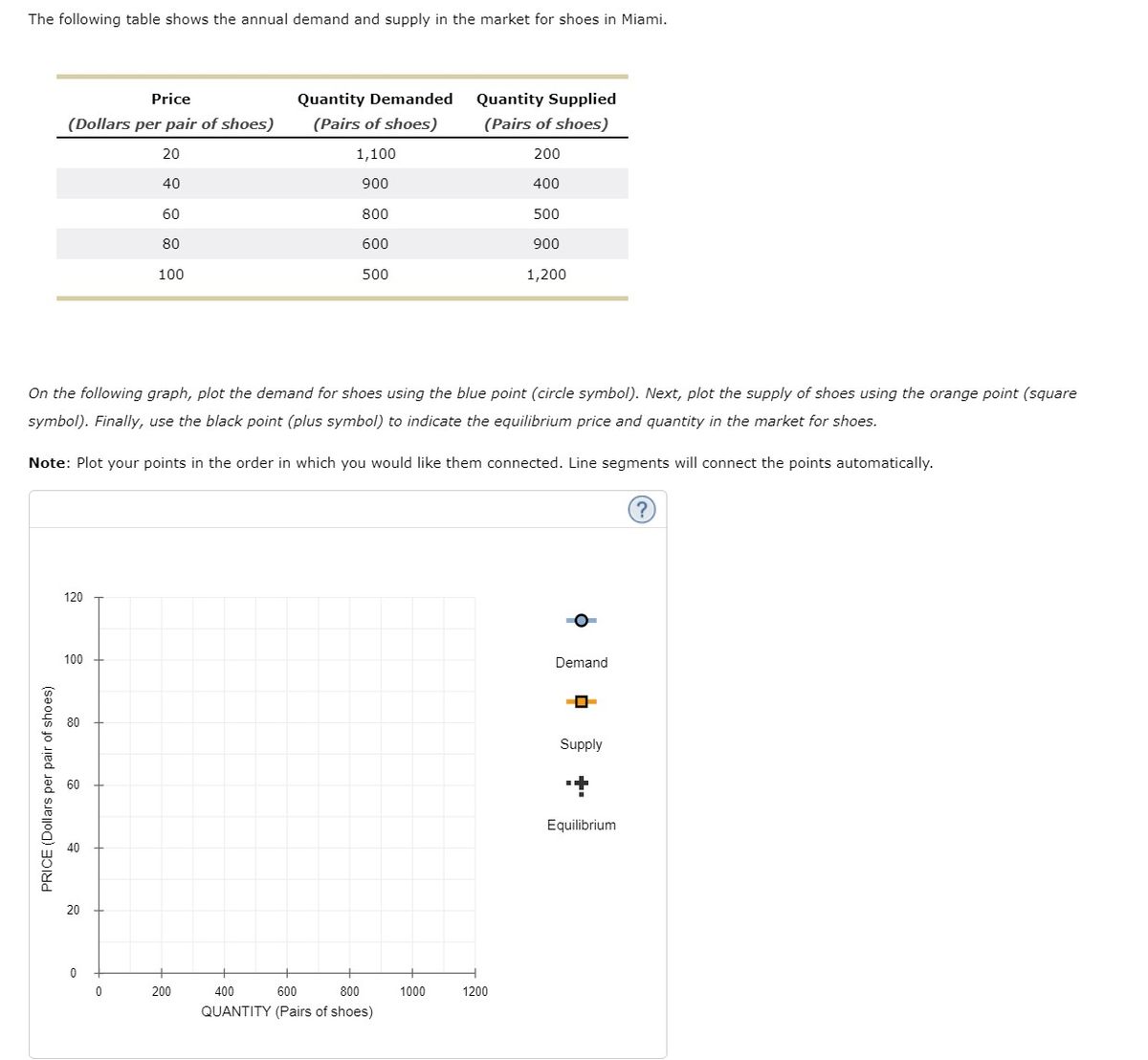

Transcribed Image Text:The following table shows the annual demand and supply in the market for shoes in Miami.

Price

(Dollars per pair of shoes)

20

40

60

80

PRICE (Dollars per pair of shoes)

120

100

20

On the following graph, plot the demand for shoes using the blue point (circle symbol). Next, plot the supply of shoes using the orange point (square

symbol). Finally, use the black point (plus symbol) to indicate the equilibrium price and quantity in the market for shoes.

Note: Plot your points in the order in which you would like them connected. Line segments will connect the points automatically.

0

100

0

Quantity Demanded

(Pairs of shoes)

1,100

900

800

200

600

500

400

600

800

QUANTITY (Pairs of shoes)

Quantity Supplied

(Pairs of shoes)

200

400

500

900

1000

1,200

1200

O

Demand

Supply

Equilibrium

Expert Solution

arrow_forward

Introduction:

A demand schedule is a table that lists the price of goods and the quantity demanded at those prices. It can be drawn for individuals as well as the entire market. It is beneficial to investigate the pattern in which consumers purchase the given good. The demand curve is also known as a demand schedule because it is a graphical representation of demand schedules.

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Draw a demand and supply graph for each of the following questions. For each question, start by drawing a correctly labeled graph of the market for cookies in equilibrium. Your starting graphs should each have correctly labeled axes and demand and supply curves. Label the equilibrium price and quantity as p1 and p2 on the axes of each of the starting graphs. 1. Show the effect on the equilibrium price and quantity in the market for cookies if the price of milk increases. Determine which curve is affected by the change in the price of milk and whether it increases or decreases. On your graph, draw a new curve indicating the shift- either to the right or the left. Label the new equilibrium price and quantity as p2 and q2. 2. Show the effect on the equilibrium price and quantity in the market for cookies if the price of flour decreases. Determine which curve is affected by the change in the price of flour and whether it increases or decreases. On your graph, draw a new curve indicating…arrow_forwardThanks in advance!!!! ( urgent!!!)arrow_forwardSuppose both the demand for olives and the supply of olives decline by equal amounts over some time period. Use graphical analysis to show the effect on equilibrium price and quantity. Instructions: On the graph below, use your mouse to click and drag the supply and demand curves as necessary. D1 Quantity of olives Price of olivesarrow_forward

- Consider the following two equations for the demand and supply: Supply curve: Qs = 10 + 2P Demand curve: Qd = 30 − 12P (a) What is the value of the equilibrium price? (b) What is the equilibrium quantity? Suppose that clothes workers at a certain factory accept a pay cut of $3 per hour. (a) Draw a graph to show how this would affect the market for clothes. (b) Why does this shift occur? How does that affect the equilibrium price and quantity? Suppose that the price of product A increases from $10 to $19. As a result, quantity demanded for product B changes from 300 to 265. What can we say about products A and B? Explain.arrow_forwardConsider two markets: the market for waffles and the market for pancakes. The initial equilibrium for both markets is the same, the equilibrium price is $6.50, and the equilibrium quantity is 35.0. When the price is $9.75, the quantity supplied of waffles is 57.0 and the quantity supplied of pancakes is 101.0. For simplicity of analysis, the demand for both goods is the same. Using the midpoint formula, calculate the elasticity of supply for pancakes. Please round to two decimal places. Supply in the market for waffles isarrow_forwardI need a unique solution within two hours, without copying the answer from websites.arrow_forward

- Hi, this question is difficult for me. Could you please help me?arrow_forward16. How shifts in demand and supply affect equilibrium Consider the market for pens. Suppose that the number of students with an allergy to pencil erasers increases, causing more students to switch from pencils to pens in school. Moreover, the price of plastic, an important input in pen production, has dropped considerably. On the following graph, labeled Scenario 1, indicate the effect these two events have on the demand for and supply of pens. Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back to its original position, just drag it a little farther. Scenario 1 10 Supply Demand Supply Demand 2 10 QUANTITY (Millions of pens) PRICE (Dollars per pen)arrow_forwardSuppose the equation for demand can be expressed as P = 40 – 2Q. The equation for supply can be expressed as P = Q. Find the equilibrium price and quantity. Be able to draw the graph that illustrates your answer.arrow_forward

- Tips ps Chapter 04 Homework The following table presents the monthly demand and supply in the market for oat milk in New York City. PRICE (Dolars per gallon of oat milk) 2 On the following graph, plot the demand for oat milk using the blue point (circle symbol). Next, plot the supply of oat milk using the orange point (square symbol). Finally, use the black point (plus symbol) to indicate the equilibrium price and quantity in the market for oat milk. Note: Plot your points in the order in which you would like them connected. Line segments will connect the points automatically. ? H 10 0 13 Price (Dollars per gallon of oat milk) 2 4 6 0 8 10 400 Quantity Demanded (Gallons of oat milk) 2,200 1,600 1,200 800 400 800 1200 1600 QUANTITY (Gations of oat mig 2000 Quantity Supplied (Gallons of oat milk) 400 1,000 1,800 2,000 2,400 12400 O Demand -P Supply + Equilibriumarrow_forwardthe combination of generous stimulus payments and the extremely successful Covid vaccination campaign should lead to a significant increase in the number of drivers getting back on the road. Using a graph, depict and explain the impact of the change. Which of the curve(s), if any, would shift, and why? Graphically indicate the new equilibrium, labeling it as P2 and Q2. What has happened to price? What has happened to quantity?arrow_forwardQuestion #24 You must use Illustration 8 below to help solve Question #24 Price Quantity Illustration 8 Check box once you answered question #24. QUESTION 24 You MUST refer to Illustration #8 for Question #24 in the Exam Worksheet. Problem: Assume there is a shift in supply and demand for a product where there is a Small increase in Demand and a Large increase in Supply. Note: Indicate whether Quantity and Price increases, decreases or is indeterminate (stays unchanged). What happens to each of the following? Price: Quantity: Use the exam worksheet to solve this problem then select your answer from one the four choice below. O Price increases and Quantity increases Price is decreases and Quantity in indeterminant Price decreases and Quantity increases Price decreases and Quantity decreasesarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education