ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

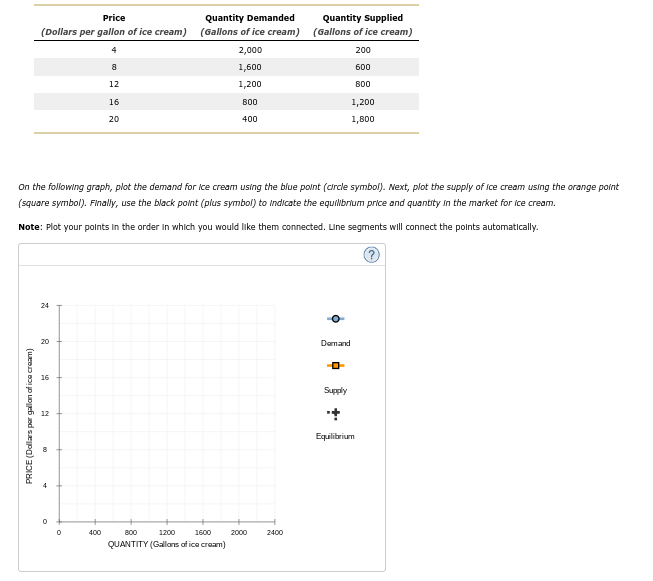

The following table shows the annual demand and supply in the market for ice cream in Houston.

|

|

Quantity Demanded

|

Quantity Supplied

|

|---|---|---|

|

(Dollars per gallon of ice cream)

|

(Gallons of ice cream)

|

(Gallons of ice cream)

|

| 4 | 2,000 | 200 |

| 8 | 1,600 | 600 |

| 12 | 1,200 | 800 |

| 16 | 800 | 1,200 |

| 20 | 400 | 1,800 |

On the following graph, plot the demand for ice cream using the blue point (circle symbol). Next, plot the supply of ice cream using the orange point (square symbol). Finally, use the black point (plus symbol) to indicate the equilibrium price and quantity in the market for ice cream.

Transcribed Image Text:Price

Quantity Demanded

(Dollars per gallon of ice cream) (Gallons of ice cream)

4

2,000

8

1,600

12

1,200

16

800

20

400

PRICE (Dollars pour gallon of ice cream)

On the following graph, plot the demand for ice cream using the blue point (circle symbol). Next, plot the supply of ice cream using the orange point

(square symbol). Finally, use the black point (plus symbol) to indicate the equilibrium price and quantity in the market for ice cream.

Note: Plot your points in the order in which you would like them connected. Line segments will connect the points automatically.

24

8

16

N

09

0

0

400

800

1200

1600

QUANTITY (Gallons of ice cream)

2000

Quantity Supplied

(Gallons of ice cream)

200

600

800

2400

o

Demand

-0-

1,200

1,800

Supply

Equilibrium

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- PRICE (Dollars per cup) Suppose that Brian and Crystal are the only suppliers of iced lattes in some hypothetical market. Their monthly supply schedules are given by the following table: Price (Dollars per cup) Brian's Quantity Supplied Crystal's Quantity Supplied (Cups) (Cups) 1 0 3 2 4 6 3 6 8 4 7 10 5 8 11 On the following graph, plot Brian's supply of iced lattes using the green points (triangle symbol). Next, plot Crystal's supply of iced lattes using the purple points (diamond symbol). Finally, plot the market supply of iced lattes using the orange points (square symbol). Note: Line segments will automatically connect the points. Remember to plot from left to right. 5 0 0 4 8 12 16 20 24 QUANTITY (Cups) Brian's Supply Crystal's Supply --- Market Supplyarrow_forwardConsider the market for beer in the diagram below: Price (S) 70 60 50 40 30 20 10 D 100 200 300 400 500 600 700 800 900 1,000 Beer (millions of cases) Suppose demand shifts to the right by 200 million cases of beer. What would be the new equilibrium price and quantity of beer as a result of this increase in demand? $55 and 500 million cases of beer $65 and 500 million cases of beer $55 and 550 million cases of beer $60 and 600 million cases of beerarrow_forwardDemand and supply often shift in the retail market for gasoline. Here are two demand curves and two supply curves for gallons of gasoline in the month of May in a small town in Maine. Some of the data are missing.Using the table, answer the following questions: Quantities Demanded Quantities Supplied Price D1 D2 S1 S2 $7.00 5,000 7,500 9,000 9,500 6,000 8,000 8,000 9,000 5.00 8,500 8,500 9,000 5,000 Use the following facts to fill in the missing data in the table. If demand is D1 and supply is S1, the equilibrium quantity is 7,000 gallons per month. When demand is D2 and supply is S1, the equilibrium price is $6.00 per gallon. When demand is D2 and supply is S1, there is an excess demand of 4,000 gallons per month at a price of $4.00 per gallon. If demand is D1 and supply is S2, the equilibrium quantity is 8,000 gallons per month. b. Compare the two equilibriums: In the first,…arrow_forward

- There has been explosive growth in the demand for the green leafy vegetable kale in recent years as consumers learned of its health benefits. The demand curve has shifted significantly rightward. However, the price of a bunch of kale in the grocery store has been fairly stable. Draw a supply and demand diagram showing the market for kale, and show how the price of kale could remain stable in the face of such an enormous growth in demand. 1.) please plot the new supply and demand curves on a diagram and label the lines properly. 2.) please also indicate the new equilibrium point at the same price as the original equilibrium and label it.arrow_forwardConsider the market for pens. Suppose that the number of students with an allergy to pencil erasers Increases, causing more students to switch from pencils to pens In school. Moreover, the price of plastic, an important input in pen production, has dropped considerably. On the following graph, labeled Scenario 1, indicate the effect these two events have on the demand for and supply of pens. Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back to its original position, just drag it a little farther. Scenarlo 1 10 Supply Demand Supply Demand 01 0 1 2 3 6 7. 9 10 4 QUANTITY (Millions of pens) Next, complete the following graph, labeled Scenario 2, by shifting the supply and demand curves in the same way that you did on the Scenario 1 graph. PRICE (Dollars per pen)arrow_forwardSuppose both the demand for olives and the supply of olives decline by equal amounts over some time period. Use graphical analysis to show the effect on equilibrium price and quantity. Instructions: On the graph below, use your mouse to click and drag the supply and demand curves as necessary. D1 Quantity of olives Price of olivesarrow_forward

- QUESTION 7 To mark national burger day there is a nationwide 50% sale on burgers during May. A recent survey, of those who bought burgers at supermarkets and food trucks, found that 99% of people will only eat burgers in a bun. Which of the following statements are true: The decrease in the price of burgers during May will cause a decrease in the quantity demanded of burgers. The decrease in the price of burgers in May will cause an increase in both demand and quantity demanded for buns. The decrease in the price of burgers in May will only result in an increase in the quantity demanded for buns. Economic theory is unable to predict if there would be any shift in demand for buns with the discount on burgers in May.arrow_forwardSupply and Demand Problem Set[1] Use the following graph to answer questions 1 through 3: Plot the following Price and Quantity combinations: (4, 8), (1, 2), (5, 10) Is your graph more likely to be a demand curve or a supply curve? Why? Using the equation of a line, and P for price and Q for quantity, what is the algebraic formula of this curve? Use the following graph to answer questions 4 and 5: Plot the following Price and Quantity combinations. Note that the points are given in the format (Quantity, Price).(0, 50), (2, 40), (4, 30), (6, 20), (8, 10) Using the equation of a line, what is the algebraic formula of this demand curve? Use the following information to answer questions 6 through 10: Suppose the equation of the line changes to . Compute the quantity demanded at each indicated price. Price: $50, Quantity: Price: $40, Quantity: Price: $30, Quantity: Price: $20, Quantity: Price: $10, Quantity: Use the following graph to answer questions 11…arrow_forwardConsider the following graph of a supply curve: Price P=Y Axis Quantity Q= X Axis Units of Y 2 C. D 3 6 B 9 Units of X 12 Write the linear equation and compute the slope and the intercept b. Write the equation for the 45 degree line starting at zero. Is this line above or below the supply curve? What would be the price for a supplied amount of 14?arrow_forward

- 8. Shifts in supply or demand I The following graph plots the market for electric guitars in Chicago, where there are always over 1,000 music stores. Suppose the price of acoustic guitars decreases. (Assume that people regard electric guitars and acoustic guitars as substitutes.) Show the effect of this change on the market for electric guitars by shifting one or both of the curves on the following graph, holding all else constant. Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back to its original position, just drag it a little farther. PRICE (Dollars per guitar) QUANTITY (Guitars) Supply Demand Demand Supply ? Now suppose Congress passes a new tax that decreases the income of Chicago reside If electric guitars are a normal good, this will cause the demand for electric guitars to decrease increasearrow_forwardThe demand and supply curves for a product are given by: Qd = 600 - 2P Qs = 300 + 4P Find the equilibrium price and the equilibrium quantity. Carefully draw a graph to illustrate your answer. Make sure to write out the intercepts. Show the equilibrium price and the equilibrium quantity on your graph.arrow_forwardThe following graph presents the market for motorcycles in 2015. Between 2015 and 2016, the equilibrium quantity of motorcycles remained constant, but the equilibrium price of motorcycles decreased. Given this information, you can conclude that between 2015 and 2016, the supply of motorcycles and the demand for motorcycles Make changes to the graph to illustrate your answer by showing the positions of the supply and demand curves in 2016. Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back to its original position, just drag it a little farther." lars per motorcycle) Supply Demand Supply ?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education