ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

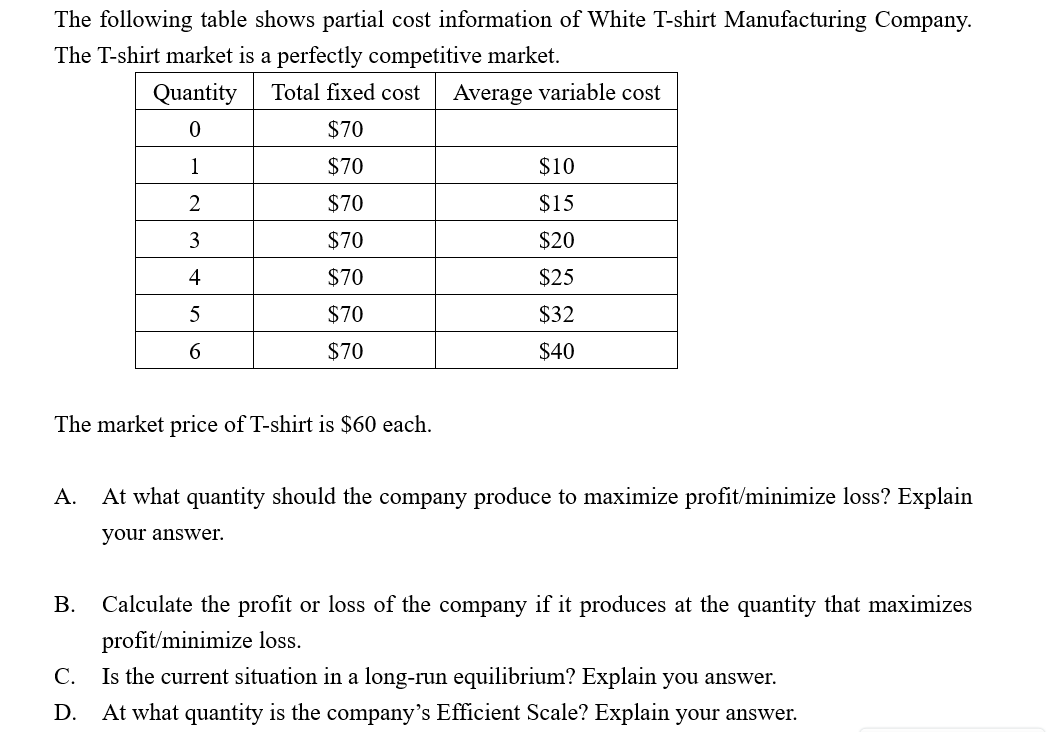

The following table shows partial cost information of White T-shirt Manufacturing Company. The T-shirt market is a

thanks!

Transcribed Image Text:The following table shows partial cost information of White T-shirt Manufacturing Company.

The T-shirt market is a perfectly competitive market.

Quantity

Total fixed cost

Average variable cost

$70

$70

$10

1

$70

$15

$70

$20

3

$70

$25

4

$70

$32

$70

$40

The market price of T-shirt is $60 each.

At what quantity should the company produce to maximize profit/minimize loss? Explain

A.

your answer.

Calculate the profit or loss of the company if it produces at the quantity that maximizes

B.

profit/minimize loss.

Is the current situation in a long-run equilibrium? Explain you answer.

C.

At what quantity is the company's Efficient Scale? Explain your answer.

D.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Amos McCoy is currently raising corn on his 100-acre farm and earning an accounting profit of $100 per acre. However, if he raised soybeans, he could earned an accounting profit of $200 per acre. Is he currently earning an economic profit?arrow_forwardQUESTION 10 Jack sells water bottles. Assume the market for water bottles is perfectly competitive. Jack sells his water bottles at the market price of $9.00. At the profit-maximising output level of 51 water bottles, Jack's average total cost is $4.40 per water bottle. The minimum average variable cost is $3.90 per water bottle. Answer the following questions: a. Jack's economic profit or loss is decimal places (ie: to the nearest cent). (use a negative value if a loss). Answer in dollars, rounded to two b. State whether the following statement is true or false: "At the profit-maximising quantity, Jack is making an economic profit of $4.60 per water bottle." Type T for true, or F for false c. State whether the following statement is true or false: "Jack should shut down if the market price is $3.85 per water bottle." Type T for true, or F for falsearrow_forward1) The cost curves for a firm in a perfectly competitive industry are given below. Complete the table. If the firm operates in a perfectly competitive market, and the market price is $25 per unit, what Quantity should this firm produce at? TFC TC TVC AVC ATC MC TR S100 S100 1 S100 S130 2 S100 S150 S100 S160 S100 S172 5 S100 S185 6 S100 $210 S100 $240 S100 $280 S100 $330 10 S100 $390 Table 9.1arrow_forward

- Use the graph to answer the following question: Is the running shoes market in long run equilibrium? Explain.arrow_forwardCrabby Bob’s is a seafood restaurant in a beach resort in Delaware. Crabby Bob’s earns a profit each month from May through September, suffers losses in October, November, and April but remains open, and remains closed from December through March. Given that the restaurant market in this town is perfectly competitive, how would you explain Crabby Bob’s decisions?arrow_forwardDetermine a perfectly competitive firm’s profit-maximizing output level and profit in the short run.arrow_forward

- Can you think of a product that meets at least most of the criteria required for a perfectly competitive market? Which criteria does it fail to meet?arrow_forwardWhen would a profit-maximizing firm shut down in the short run?arrow_forwardDefine the aspects of perfect competitive market in detail.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education