ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

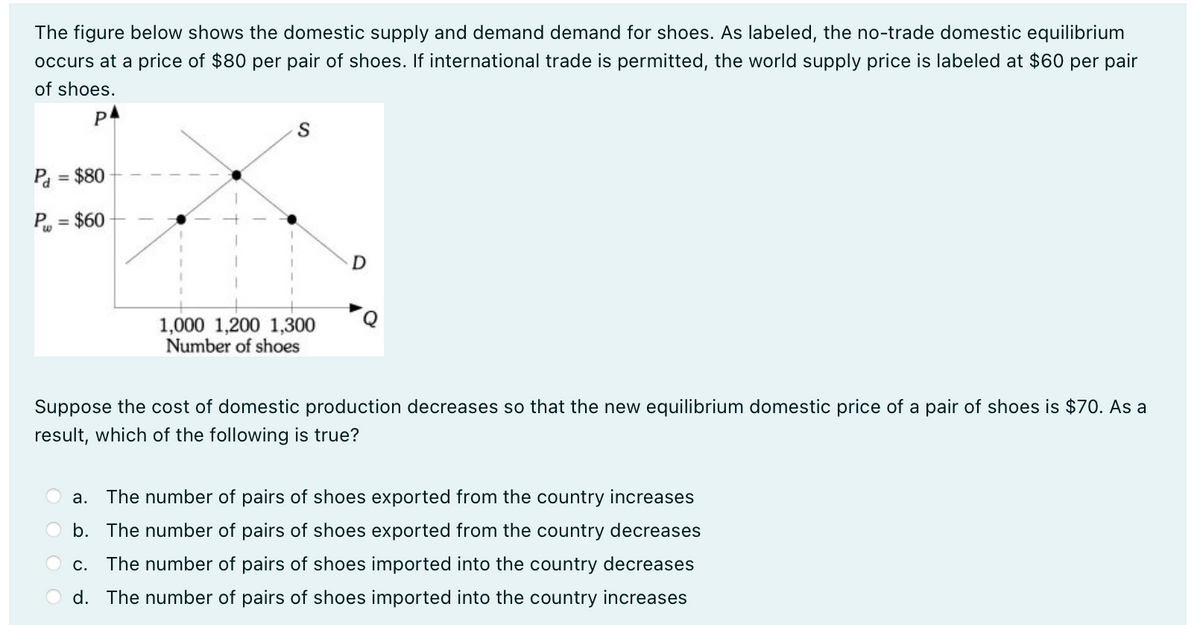

Transcribed Image Text:The figure below shows the domestic supply and demand demand for shoes. As labeled, the no-trade domestic equilibrium

occurs at a price of $80 per pair of shoes. If international trade is permitted, the world supply price is labeled at $60 per pair

of shoes.

P

P₁ = $80-

P = $60

S

1,000 1,200 1,300

Number of shoes

D

Suppose the cost of domestic production decreases so that the new equilibrium domestic price of a pair of shoes is $70. As a

result, which of the following is true?

a. The number of pairs of shoes exported from the country increases

b. The number of pairs of shoes exported from the country decreases

C. The number of pairs of shoes imported into the country decreases

d. The number of pairs of shoes imported into the country increases

Transcribed Image Text:The figure below shows the domestic supply and demand demand for shoes. As labeled, the no-trade domestic equilibrium

occurs at a price of $80 per pair of shoes. If international trade is permitted, the world supply price is labeled at $60 per pair

of shoes.

P

P₁ = $80

P = $60

S

1,000 1,200 1,300

Number of shoes

D

Suppose the government implements an import quota of 200 pairs of shoes. Which of the following statements is false?

a. Producers will be made better off.

b. The resulting equilibrium price will be higher than $60.

c. The resulting equilibrium price will be higher than $80.

d. The number of pairs of shoes imported into the country will decrease.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Two countries, Home (H) and Foreign (F) trade agricultural and manufacturing goods (A and M, respectively). Production of either good requires skilled and unskilled labor. Unskilled workers can freely move from one sector to another, while skilled workers cannot. Identify mobile and industry-specific factors of production (b) Suppose Home is relatively more productive in agriculture than Foreign. Draw two diagrams, one for H one for F, which illustrate no-trade equilibrium in each county. Compare relative price of agricultural goods in two countries.arrow_forwardSuppose a large country A initially imposed a tariff on its imports and is now considering removing its tariff. Use a domestic-market graph to a) show the effect of country A’s tariff removal on the world’s price, country A’s import price, import quantity, consumer surplus, producer surplus, and government revenue. b) identify country A’s net welfare change as a result of its tariff removal. Is country A unambiguously better off? c) Use a different graph to show how foreign producers will be affected by country A’s tariff removal? d) What factor determines the level of optimal tariff for country A? Please make sure to graph fpr both parts "a" and "c"arrow_forwardPrice of Clothing Market for Clothing in Pakistan Domestic Demand Quantity of Clothing Domestic Supply New World Price A Consumer Surplus Producer Surplus ? Suppose the following graph represents the market of clothing in Denmark prior to the expansion of China's clothing industry. Denmark is an exporter of clothing because the world price is above the domestic equilibrium price.arrow_forward

- Suppose that the world price for a good is 60 and the domestic demand-and-supply curves are given by the following equations: Demand: P = 100 – 4Q %3D Supply: P = 10 + 5Q %3D If a tariff of 20 percent is imposed, by how much do consumption and domestic production change?arrow_forwardCountry X has 100 units of labour and country Y has 200 units of labour. Both countries produce computers and televisions. The unit labour requirements are given in the table below: Computers Televisions Country X 50 Country Y 100 Assume that free trade exists and that the relative price is such that both countries specialize completely in the industry in which they have a comparative advantage (neither country produces both goods). The supply of computers relative to televisions will be Select one: a. 0.02 (or 1/50) O b. 0.013 (or 1/75) c. 0.01 (or 1/100) d. impossible to determine without knowing the relative price of computers in terms of televisionsarrow_forwardIf the world price the price you can get for a box of your contact lenses is greater than the domestic equilibrium price of $120 will you increase or decrease your quantity supplied of contact lensesarrow_forward

- Suppose that under free trade a final good F has a price of $1,000 and that the prices of two inputs, A and B, used in the production of F are PA = $300 and PB = 500 and that one unit each of A and B is used in producing one unit of F. Suppose also that a tariff of 20 percent is placed on good F, while imported inputs had tariffs of 20 percent and 30 percent respectively. Calculate the effective rate of tariff protection for domestic industry producing good F and interpret the meaning of your result (All steps must be shown to obtain full credit). Note: v = value added without tariff and v' = value added with tariff.arrow_forwardNow, suppose that Island is a large exporting country with the following demand and supply functions and the free-trade world price is $5,000 per unit. D = 900,000 − 150P and S = 100,000 + 50P The Island government offers an export subsidy that increases the domestic market price to $5,500 and lowers the world price to $4,500. However, starting next month, the Island government will be removing the export subsidy in compliance with the latest international trade pact. A. What is the impact of the removal of the subsidy on domestic consumers? B. What is the change in producer surplus due to the movement to free trade? C. What is the net effect of moving to free trade on Island welfare?arrow_forwardWhich statement BEST reflects the difference between tariffs and quotas? Tariffs raise prices on imports, while quotas set limits on imports Tariffs raise prices on exports, while quotas set limits on exports Tariffs raise prices on imports, while quotas set limits on exports Tariffs raise prices on exports, while quotas set limits on importsarrow_forward

- QD = 100 – 2p QS = 2p – 20 Find the domestic market equilibrium. Graph the impact of opening to international trade with a world price of 48, clearly labelling the new consumer surplus and producer surplus. Find the exact numerical amounts of consumer surplus, producer surplus, government revenue, and total welfare, for the case of autarky and the case of international trade. What would happen if the government imposed a tariff of 20/unit in this market? Explain.arrow_forwardThe small nation of Capralia has an abundant stock of Pashmina goats, a breed that yields high-quality cashmere. Capralia's authorities are still debating whether to open their economy to international trade. The international price of cashmere is $70,000 per metric ton, and the Capralian cashmere sells for $50,000 per metric ton. Place the consumer surplus triangle (CS) and the producer surplus triangle (PS) to correctly depict consumer and producer surplus if Capralia chooses to open its borders to the international cashmere trade. 100 Price (metric ton) 90 80 70 80 50 40 30 20 10 10 0 Capralia's Domestic Cashmere Market 6 domestic supply domestic equilibrium 12 18 24 30 36 42 Quantity (thousands of metric tons) 48 54 60 CS Capralia will import 36,000 metric tons of cashmere. Capralia will export 24.000 metric tons of cashmere. Capralia will not engage in international trade. Capralia will export 12,000 metric tons of cashmere. Capralia will import 24,000 metric tons of cashmere. PS…arrow_forwardIf Bangladesh is open to international trade of wheat without any restrictions, it will import the full value for your answer, accounting for the horizontal axis units.) Suppose the Bangladeshi government wants to reduce imports to exactly 200,000 bushels of wheat to help domestic producers. A tariff of S per bushel will achieve this. A tariff set at this level would raise $ bushels of wheat. (Note: Be sure to enter in revenue for the Bangladeshi government.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education