ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

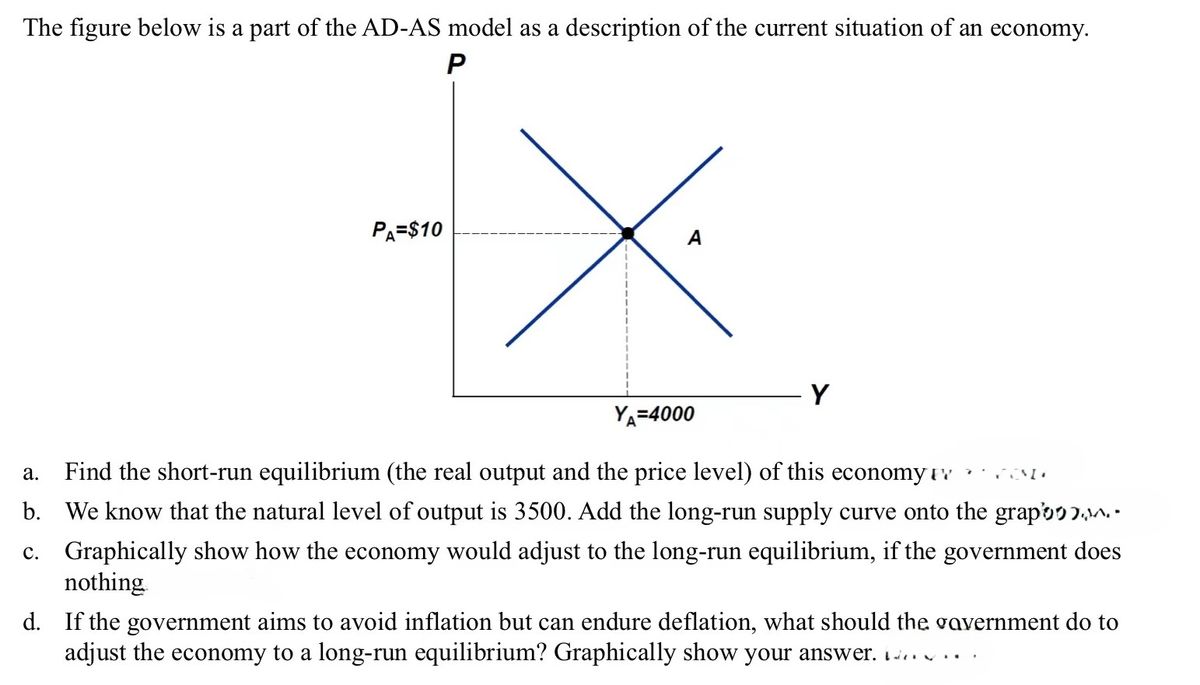

Transcribed Image Text:The figure below is a part of the AD-AS model as a description of the current situation of an economy.

P

PA=$10

A

YA=4000

Y

a. Find the short-run equilibrium (the real output and the price level) of this economy v

b. We know that the natural level of output is 3500. Add the long-run supply curve onto the grap

c. Graphically show how the economy would adjust to the long-run equilibrium, if the government does

nothing

d. If the government aims to avoid inflation but can endure deflation, what should the government do to

adjust the economy to a long-run equilibrium? Graphically show your answer. .

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 3 images

Knowledge Booster

Similar questions

- Suppose that the economy is initially in long-run equilibrium with the price level of 800. Now suppose that the Aggregate Demand (AD) curve shifts left from AD1 (blue) to AD2 (green). 1200 ADX 1100- 1000 Price Level ADX 900- 800 700 600 50% RASI 400* 300- 200 100- LRAS 400 500 600 700 100 200 300 Real GDP What is the new price level in the short-run as a result of this shift? 800 900 1000 1100 120 aarrow_forwardPlease write on the space provided what happens to each variable -- indicate whether each variable increases, decreases, or remains unchanged. Please show in the graphs the initial equilibrium, short run equilibrium, and final long run equilibrium. If possible, please provide only two graphs, one for IS-LM and one for AD-AS that show all of the equilibrium positions Suppose the economy is initially in a long-run equilibrium. Starting from this position, assume that an exogenous shock such as the Covid 19 pandemic pushes the economy away from the equilibrium. Using the IS-LM and AD-AS framework, indicate what happens in the short run to output, unemployment, prices, interest rate, consumption, investments, and real money balances, as the economy moves from long-run equilibrium to short-run equilibrium. What economic condition is the economy in after the shock? __________________ Short-run Output ________________ Unemployment _________________ Prices…arrow_forwardOn the following graph, use the black point (cross symbol) to show the short-run equilibrium. Then use the grey point (star symbol) to show the long- run equilibrium. PRICE LEVEL 120 110 100 1 LRAS REAL GOP In the short run, the price level is Natural Real GDP SRAS, SRAS, AD SRAS, AD AD₂ and Real GDP is ++ Short-Run Equilibrium ✡ Long-Run Equilibrium ? Natural Real GDP. In the long run, the price level is and Real GDP is Aarrow_forward

- Brent, the international oil marker, hit US$130 a barrel on 8th March 2022. The oil price is close to 90 per cent above their level at the same point in time last year. Suppose that the rise in oil price is permanent. It creates an inflation shock and, at the same time, reduces potential output. With the aid of AD-AS model, show the difference in the effects of the oil price increase on output and the inflation rate in the long run if the government does not engage in stabilization policy and if the government does engage in stabilization policy to keep the inflation level low. Please elaborate your answer verbally.arrow_forwardWhich of the figures above illustrates an economy in long-run equilibrium? A) Figure A B) Figure B C) Figure Carrow_forwardFor each of the following economic events, analyze the short-run and long-run transitions of the economy without and with government intervention. For each question, start from the initial long run equilibrium, point A. G point D, point C point E, point B SRAS Q10. There is a sudden decrease in oil price. Without government intervention, this would move the economy from point A to in the long run in the short run, then to point G, point A point G, point B AD₂arrow_forward

- Why is price “stickiness” or “rigidity” important for understanding macroeconomic adjustments? How would policy recommendations be different if prices adjusted immediately?arrow_forwardAssume an ecomy operates in the intermediate range of its aggregate supply curve. State the direction of shif for the aggregate demand curve or aggregate supply curve for each of the following changes in conditions. What is the effect on the price level? On real GDP? On employment?arrow_forwardPLEASE ANSWER ALL PARTS OF QUESTIONS 1 AND 2.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education