ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

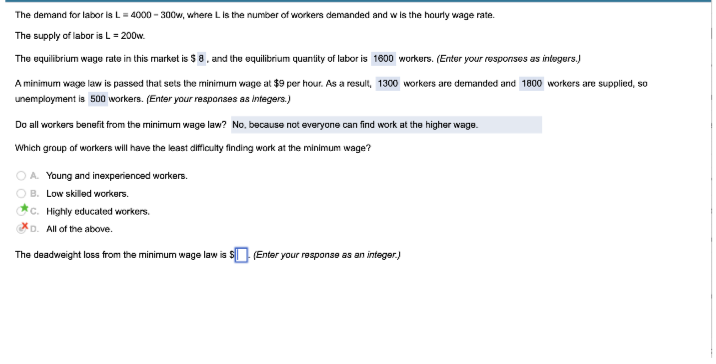

Transcribed Image Text:The demand for labor is L= 4000 - 300w, where L is the number of workers demanded and w is the hourly wage rate.

The supply of labor is L = 200w.

The equilibrium wage rate in this market is $ 8. and the equilibrium quantity of labor is 1600 workers. (Enter your responses as integers.)

A minimum wage law is passed that sets the minimum wage at $9 per hour. As a result, 1300 workers are demanded and 1800 workers are supplied, so

unemployment is 500 workers. (Enter your responses as integers.)

Do all workers benefit from the minimum wage law? No. because not everyone can find work at the higher wage.

Which group of workers will have the least dificulty finding work at the minimum wage?

A. Young and inexperienced warkers.

B. Low skilled workers.

C. Highly educated workers.

D. All of the above.

The deadweight loss from the minimum wage law is

(Enter your response as an integer.)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider a perfectly competitive labor market in which the demand for labor isgiven by E = 48,000 – (2,000/3)W, and the supply of labor is given by E = -8,000+ 1,000W. In these equations, E is the number of employee-hours per day, and Wis the hourly wage.a. What is the equilibrium number of employee-hours each day?b. Compute the employer surplus and the workers surplusc. Suppose the government imposes a minimum wage of $24 per hour. Whatwill be the resulting number of employee-hours after the imposition of thisminimum wage?d. What is the number of employee-hours per day hired and the number ofemployeese. Based on the question © Compute the employer surplus and the workerssurplusf. Compute the dead weight loss in this labor market with minimum wageProblem Varrow_forwardFour (TYPE I) firms sell Product X in competitive markets at a price of 10. They each operate with the production function: x = 100L – L². Another firm with monopoly power (TYPE II) sells faces demand curve P = 160 – Y and has production function Y = 5L. All five firms hire as wage-takers in the same market where labour supply is w = 2L. Illustrate and quantify the equilibrium wage and the number of workers hired by each firm. а. Solve for the equilibrium wage and employment by each firm. b. Provide a 3-panel diagram. 6.arrow_forwardEconomic theory suggests that an increase in the minimum wage will prompt firms to hire fewer low skill workers. true or falsearrow_forward

- What are the pros and cons of increasing the minimum wagearrow_forwardA company has 350 employees who work 120 hours a month each. Each worker earns $21 per hour. There is a profitable project the company would like to start, but it would require an additional 21,000 working hours within three months to be completed, and all the employees are fully loaded with other projects. The company does not want to hire new staff; they would like the project to be completed by the current workforce instead.Given that the wage elasticity of labor supply is 0.8, calculate the hourly wage the company should offer its employees to encourage them to work on the new project. Use the midpoint method and round to two decimal places throughout your calculations.arrow_forwardPlease help with the following.arrow_forward

- The following graph shows the labor market for research assistants in the fictional country of Universalia. The equilibrium wage is $10 per hour, and the equilibrium number of research assistants is 250. Suppose the government has decided to institute a $4-per-hour payroll tax on research assistants and is trying to determine whether the tax should be levied on the employer, the workers, or both (such that half the tax is collected from each side). Use the graph input tool to evaluate these three proposals. Entering a number into the Tax Levied on Employers field (initially set at zero dollars per hour) shifts the demand curve down by the amount you enter, and entering a number into the Tax Levied on Workers field (initially set at zero dollars per hour) shifts the supply curve up by the amount you enter. To determine the before-tax wage for each tax proposal, adjust the amount in the Wage field until the quantity of labor supplied equals the quantity of labor demanded. You will not be…arrow_forwardExplain the challenges of an increasing minimum wage for an economyarrow_forwardCan you let me know if i got these correct. thanksarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education