ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

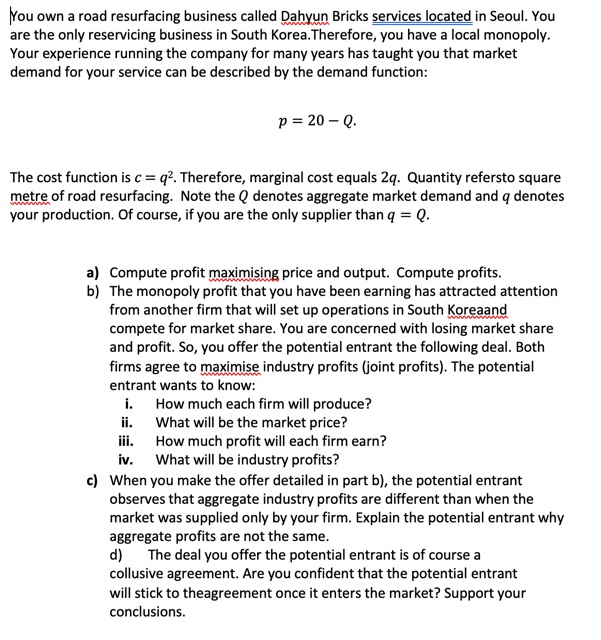

Transcribed Image Text:You own a road resurfacing business called Dahyun Bricks services located in Seoul. You

are the only reservicing business in South Korea. Therefore, you have a local monopoly.

Your experience running the company for many years has taught you that market

demand for your service can be described by the demand function:

p = 20 - Q.

The cost function is c =q². Therefore, marginal cost equals 2q. Quantity refersto square

metre of road resurfacing. Note the Q denotes aggregate market demand and q denotes

your production. Of course, if you are the only supplier than q = Q.

a) Compute profit maximising price and output. Compute profits.

b) The monopoly profit that you have been earning has attracted attention

from another firm that will set up operations in South Koreaand

compete for market share. You are concerned with losing market share

and profit. So, you offer the potential entrant the following deal. Both

firms agree to maximise industry profits (joint profits). The potential

entrant wants to know:

i.

How much each firm will produce?

What will be the market price?

ii.

iii.

How much profit will each firm earn?

iv. What will be industry profits?

c) When you make the offer detailed in part b), the potential entrant

observes that aggregate industry profits are different than when the

market was supplied only by your firm. Explain the potential entrant why

aggregate profits are not the same.

d) The deal you offer the potential entrant is of course a

collusive agreement. Are you confident that the potential entrant

will stick to theagreement once it enters the market? Support your

conclusions.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The next three problems are from Unit 10. You are provided with a pair of demand and cost functions. P=20,000-15.60 TC = 400,000 + 4640 Q + 100 Use the above functions and derive the maximum profits for the firm: Optimal Q = Optimal P = Optimal TR = Optimal profits - =arrow_forwardASK YOUR TEACHER Your college newspaper, The Collegiate Investigator, sells for 90¢ per copy. The cost of producing x copies of an edition is given by C(x) = 50 + 0.10x + 0.001x2 dollars.' (a) Calculate the marginal revenue R'(x) and profit P'(x) functions. HINT [See Example 2.] R'(x) = P'(x) = (b) Compute the revenue and profit, and also the marginal revenue and profit, if you have produced and sold 500 copies of the latest edition. revenue profit 24 marginal revenue 24 X per additional copy marginal profit $ X per additional copy Interpret the results. The approximate loss x from the sale of the 501st copy is $ (c) For which value of x is the marginal profit zero? X = X copies Interpret your answer. The graph of the profit function is a parabola with a vertex at x = so the profit is at a maximum when you produce and sell X copies. Need Heln?arrow_forwardA firm supplies its product to a number of UK cities. Its overall cost function can be expressed as TC = 40q² + 900q – 250. The Demand function in Lancaster is given by p = 3600 - 10q and that in Norwich by p = 5040-6q. i) What prices should the firm charge for its product in Lancaster and Norwich? ii) If the firm only supplies its output to Lancaster and Norwich, is it profitable? Interpret your answer; why might the firm be unable to pursue this strategy? 5.arrow_forward

- A microbrewery operates next to the Bushville Lake and uses water from the lake during production. The marginal cost of beer production is: MC = 8 + 2Q where Q is the quantity of beer produced (keg). The brewery sells its output at a market price of $40/keg. Because the industry is perfectly competitive, the brewery’s action does not affect the market price. The Bushville Lake is also used for kayaking and recreational fishing, but pollution from the brewery reduces the quantity of fish available and makes the lake very unpleasant. Each keg of beer produced emits a pound of pollutants that causes a loss of recreation opportunities worth $3. a) How much beer will be produced? b) What is the efficient level of beer production? If the government used a Pigouvian tax to achieve this goal, what would the tax be?arrow_forwardBased on the best available econometric estimates, the market elasticity of demand for your firm's product is -3.0. The marginal cost of producing the product is constant at $150, while average total cost at current production levels is $215. Determine your optimal per unit price if: Instructions: Enter your responses rounded to two decimal places. a. you are a monopolist. 2$ b. you compete against one other firm in a Cournot oligopoly. $ C. you compete against 19 other firms in a Cournot oligopoly. 2$arrow_forwarda) What is the per unit cost of the product? b) What are the demand and inverse demand functions? Now assume the local government begins to provide 100 units per week at the market price. c) What is the residual demand left for the monopolist?arrow_forward

- Babydrink is a monopolist due to its patent in infant formula. The total cost for production in dollars is given by C(q) = 24q2 + 600q +9600. a) What is the fixed cost? b) Find a function that gives the marginal cost. c) Find a function that gives the average cost. d) Find the efficient scale (that minimizes the average cost). e) Verify it is the most efficient not the least efficient.arrow_forwardAssume that you are an economic consultant. The firm that hired you has provided the information below. The firm is a price searcher and wants to maximize its profit (or minimize its loss). InformationPrice: $4Elasticity of demand at price of $4 is Ed=-1Quantity of output: 2000Total variable cost: 4000Average fixed cost: 1Marginal cost is constant and equal to the average variable cost: MC=ACV=2. Which of the following answers correctly describes this case? a) The firm is maximizing profits at the current price of $4.b) The firm should increase price and reduce quantity produced.c) None of the other answersd) Firm should reduce price and increase quantity produced.arrow_forward2. You are the Southeastern Michigan regional manager at Coca-Cola, responsible forproduction and pricing in the Metro Detroit area. Your primary competitor is Pepsi. The marketresearch team at Coca-Cola is thinking about launching a new product, Orange Vanilla Coke, toboost the brand. The cost function to produce a 12-pack of 12 fl. oz. cans of Orange VanillaCoke is C(qcoke) = 0.25qcoke and the market research team has estimated inverse market demandfor a 12-pack of this new “pop” in Southeastern Michigan to be P = 10.25 – 0.00025Q. a. Assuming Pepsi decides not to produce a similar product, allowing Coca-Cola to maintainmonopoly power in the market for orange vanilla cola, what price and quantity will youchoose to maximize profit? How much profit does Coca-Cola earn?b. What price and quantity you would choose to maximize profit if Pepsi spies discover yourproduct before launch, allowing Pepsi to produce and launch an identical product at the sametime. For your answer, assume the cost…arrow_forward

- Hand written solutions are strictly prohibitedarrow_forwardBased on the best available econometric estimates, the market elasticity of demand for your firm's product is -2.0. The marginal cost of producing the product is constant at $75, while average total cost at current production levels is $140. Determine your optimal per unit price if: Instructions: Enter your responses rounded to two decimal places. a. you are a monopolist. $ b. you compete against one other firm in a Cournot oligopoly. $ 139 * c. you compete against 19 other firms in a Cournot oligopoly. S 130arrow_forwardThe demand for home firm product is given by the inverse demand function: P = 120 −QD. The company’s costs are: T C = 20Q+ 200 and MC = $20.2. Suppose the home country open up to free trade and a foreign competitor enters the market. Assume thatthe foreign firm has the same cost structure as the home firm (the monopoly from the previous question).A) Derive the best response function for each firm (h-home and f-foreign)B) Find each firms’ output, the home market price, and each firms’ profit from the home marketarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education