Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

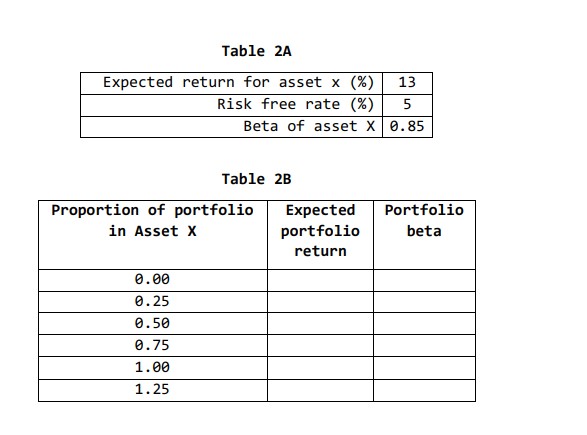

Consider the information given in the Table 2A and complete Table 2B.

From the completed Table 2B, use the information to grpahically

present the Security Market Line (SML). Compute the slope of this

line.

Hints:

i) When 100% money is invested in asset X (portfolio weight =

1), the beta of the portfolio is 0.85

ii) Since the risk-free asset is, well, risk-free, its beta will

be zero

Transcribed Image Text:Table 2A

Expected return for asset x (%)

Risk free rate (%)

13

5

Beta of asset X 0.85

Proportion of portfolio

in Asset X

0.00

0.25

0.50

0.75

1.00

1.25

Table 2B

Expected

Portfolio

portfolio

beta

return

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- Which asset in the following table has the most market risk (also known as systematic or non-diversifiable risk)? (Ch. 8) Asset Return Beta Standard Deviation Asset A 9% 0.95 20% Asset B 13% 1.10 35% Asset C 10% 1.00 40% Group of answer choices Asset A Asset C Asset B and Asset C Asset Barrow_forwardWhich asset in the following table has the most market risk (also known as systematic or non- diversifiable risk)? Asset A B Asset B Asset A Return Both Assets A and C Asset C (10% 12% 14% Beta 0.74 1.00 1.25 Standard Deviation 20% 40% 30%arrow_forwardWhat is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation (SDi), covariance (COVij), and asset weight (Wi) are as shown below? Asset (A) E(R₂) = 25% SDA = 18% WA = 0.75 COVA, B = -0.0009 Select one: A. 13.65% B. 20 U ODN 20.0% C. 18.64% D. 22.5% Asset (B) E(R₂) = 15% SDB = 11% WB = 0.25arrow_forward

- Compute the VaR(95%) and ES(95%) of the portfolio managed by Absolute Asset Management if its returns, r, follow the distribution specified below: = 1 10 - |r 100| – 10arrow_forwardBerdasarkan informasi tersebut a. Expected return Asset A b. Standard Deviation Asset A dan Asset B c. Portfolio AB Expected Return. d. Coefficient Correlation AB e. Portofolio AB Standard Deviation Please explain by Microsoft excelarrow_forward13arrow_forwardState ofEconomy Probabilityof State Return on AssetDin State Return on AssetEin State Return on AssetFin State Boom 0.35 0.060 0.310 0.25 Normal 0.50 0.060 0.180 0.20 Recession 0.15 0.060 -0.210 0.10 A. Calculate the expected return (mean) for each security.arrow_forwardQ10 In the standalone statements of the venturer, the investments are accounted at______. Select one: a. cost b. market value c. replacement value d. net realizable valuearrow_forward2. Assuming the following: Average Return (Risky Portfolio) 3.86% Standard Dev (Risky Portfolio) 10.56% Average Risk Free Rate 2.18% Return on Risk Free Asset Avg 4.15% Using the formula: E(rc)=rf + y* (E(rp) - rf) Solve for: 1. % of Risky Assets (y): 2. % of Risk Free Assets (1-y): Note: You wish to generate a 7% return for your complete portfolio E(rc)arrow_forwardQu. 5 please help and show all steps with formulas usedarrow_forwardState ofEconomy Probabilityof State Return on AssetDin State Return on AssetEin State Return on AssetFin State Boom 0.35 0.060 0.310 0.25 Normal 0.50 0.060 0.180 0.20 Recession 0.15 0.060 -0.210 0.10 1. Calculate the standard deviation for each security.arrow_forwardWhat is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation (SDi), covariance (COVij), and asset weight (Wi) are as shown below? Asset (A) E(RA) = 25% SDA = 18% WA = 0.75 COVAB= -0.0009 Asset (B) E(R₂) = 15% SDB = 11% W₁ = 0.25arrow_forwardarrow_back_iosSEE MORE QUESTIONSarrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education