FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

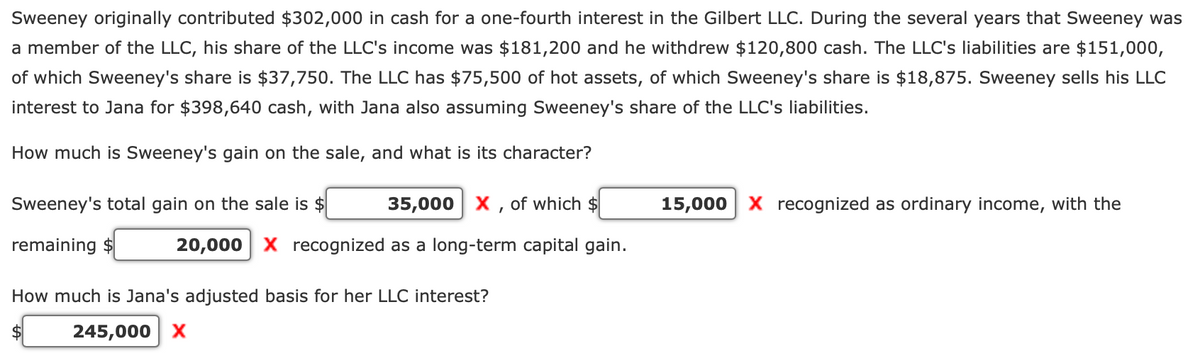

Transcribed Image Text:Sweeney originally contributed $302,000 in cash for a one-fourth interest in the Gilbert LLC. During the several years that Sweeney was

a member of the LLC, his share of the LLC's income was $181,200 and he withdrew $120,800 cash. The LLC's liabilities are $151,000,

of which Sweeney's share is $37,750. The LLC has $75,500 of hot assets, of which Sweeney's share is $18,875. Sweeney sells his LLC

interest to Jana for $398,640 cash, with Jana also assuming Sweeney's share of the LLC's liabilities.

How much is Sweeney's gain on the sale, and what is its character?

Sweeney's total gain on the sale is $

35,000 X , of which $

15,000 x recognized as ordinary income, with the

remaining $

20,000 X recognized as a long-term capital gain.

How much is Jana's adjusted basis for her LLC interest?

245,000 X

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- [The following information applies to the questions displayed below] Ray and Matias own 50 percent capital and profits interests in Alpine Properties LLC. Alpine builds and manages rental real estate, and Ray and Matias each work full time (over 1,000 hours per year) managing Alpine. Alpine's liabilities (at both the beginning and end of the year) consist of $1,540,000 in nonrecourse mortgages obtained from an unrelated bank and secured by various rental properties. At the beginning of the current year, Ray and Matias each had a tax basis of $250,000 in his respective LLC interest, including his share of the nonrecourse mortgage liability. Alpine's ordinary business losses for the current year totaled $608,000, and neither member is involved in other activities that generate passive income Note: Leave no answer blank. Enter zero if applicable. Problem 20-79 Part b (Algo) b. How much of each member's loss is suspended because of the at-risk limitation? Loss suspended Ray Matiasarrow_forwardMatthew, Inc., owns 30 percent of the outstanding stock of Lindman Company and has the ability to significantly influence the investee's operations and decision making. On January 1, 2021, the balance in the Investment in Lindman account is $365,000. Amortization of excess fair value associated with the 30% ownership is $12,600 per year. In 2021, Lindman earns an income of $132,000 and declares cash dividends of $33,000. Previously, in 2020, Lindman had sold inventory costing $33,600 to Matthew for $56,000. Matthew consumed all but 20 percent of this merchandise during 2020 and used the rest during 2021. Lindman sold additional inventory costing $44,800 to Matthew for $80,000 in 2021. Matthew did not consume 40 percent of these 2021 purchases from Lindman until 2022. a. What amount of equity method income would Matthew recognize in 2021 from its ownership interest in Lindman? b. What is the equity method balance in the Investment in Lindman account at the end of 2021? a. b. Equity…arrow_forwardBedrock Incorporated is owned equally by Barney and his wife Betty, each of whom holds 840 shares in the company. Betty wants to reduce her ownership in the company, and it was decided that the company will redeem 420 of her shares for $25, 400 per share on December 31 of this year. Betty's tax basis in each share is $7, 200. Bedrock has current E&P of $ 10, 580,000, and accumulated E&P was $50, 780,000 at the beginning of the year. a. What is the amount and character (capital gain or dividend) recognized by Betty as a result of the stock redemption, assuming only the "substantially disproportionate with respect to the shareholder" test is applied? b. Given your answer to part (a), what is Betty's income tax basis in the remaining 420 shares she owns in the company? c. By what amount does Bedrock reduce its E&P because of the redemption? d. Can Betty argue that the redemption is "not essentially equivalent to a dividend" and should be treated as an exchange?arrow_forward

- Dave LaCroix recently received a 10 percent capital and profits interest in Cirque Capital LLC in exchange for consulting services he provided. If Cirque Capital had paid an outsider to provide the advice, it would have deducted the payment as compensation expense. Cirque Capital's balance sheet on the day Dave received his capital interest appears below: Assets: Cash Investments Land Totals Liabilities and capital: Nonrecourse liabilities Lance" Robert Totals Basis $ 130,000 180,000 210,000 $ 520,000 Tax basis $ 190,000 165,000 165,000 $ 520,000 Dave Fair Market Value *Assume that Lance's basis and Robert's basis in their LLC interests equal their tax basis capital accounts plus their respective shares of nonrecourse liabilities. (Leave no answer blank. Enter zero if applicable.) Lance a. Compute and characterize any gain or loss Dave may have to recognize as a result of his admission to Cirque Capital. Gain or loss recognized as Ordinary income $ 130,000 207,000 320,000 $ 657,000 b.…arrow_forward[The following information applies to the questions displayed below.] Dave LaCroix recently received a 10 percent capital and profits interest in Cirque Capital LLC in exchange for consulting services he provided. If Cirque Capital had paid an outsider to provide the advice, it would have deducted the payment as compensation expense. Cirque Capital's balance sheet on the day Dave received his capital interest appears below: Fair Market Value Basis Assets: Cash Investments $ 220,000 300,000 100,000 $ 220,000 330,000 260,000 Land Barca Totals $ 620,000 $ 810,000 Liabilities and capital: DLAD Nonrecourse liabilities $ 200,000 $ 200,000 Lance* 210,000 210,000 305,000 305,000 Robert* Totals $ 620,000 $ 810,000 *Assume that Lance's basis and Robert's basis in their LLC interests equal their tax basis capital accounts plus their respective shares of nonrecourse liabilities. (Leave no answer blank. Enter zero if applicable.) c. Prepare a balance sheet for Cirque Capital immediately after…arrow_forwardHelen owns 30% of a flow-through entity. The capital gain comes from the sale of a piece of equipment that Helen contributed to the entity. At the time of contribution, the piece of equipment had a basis of $45,000 and a fair market value of $50,000. The entity reports the following amounts before any payments to the owners: O/S Item Amount Sales Revenue 30,000 Dividends received 10,000 Tax-exempt interest income 15,000 Capital gain 5,000 Charitable contributions 1,000 Cost of Goods Sold 10,000 General Business Expenses 3,000 a) In the O/S column above, write ‘O’ for any ordinary business items and write ‘S’ for any separately stated items. b) Assume that the entity is an S-Corp, and that Helen is also an employee of the…arrow_forward

- Yager Corporation purchased residential real estate several years ago for $225,000, of which $50,000 was allocated to the land and $175,000 was allocated to the building. Yager took straight-line MACRS deductions of $40,000 during the years it held the property. In the current year, Yager sells the property for $275,000, of which $55,000 is allocated to the land and $220,000 is allocated to the building. Requirement What are the amount and character of Yager's recognized gain or loss on the sale? Begin by computing the gain or loss on sale. Select the formula and then enter the amounts and compute the gain or loss on the sale for the land, building and for the total Land Building Total Recognized gain Next, determine the character of the gain or loss on sale of the land and building. (Complete all input fields. For items with a 0 balance, make sure to enter a 0 in the appropriate cell.) Building Total Land Recognized gain or lossarrow_forwardSuzy contributed assets valued at $360,000 (basis of $200,000) in exchange for her 40% interest in Suz-Anna GP (a general partnership in which both partners are active owners). Anna contributed land and a building valued at $640,000 (basis of $380,000) in exchange for the remaining 60% interest. Anna’s property was encumbered by qualified nonrecourse financing of $100,000, which was assumed by the partnership. The partnership reports the following income and expenses for the current tax year. What is the beginning and ending nonrecourse values. Beg $0 ending $40,000 What is the beginning Capital amount ? Sales $560,000 Utilities, salaries, depreciation, other operating expenses 360,000 Short-term capital gain 10,000 Tax-exempt interest income 4,000 Charitable contributions (cash) 8,000 Distribution to Suzy 10,000 Distribution to Anna 20,000 At the end of the year, Suz-Anna held recourse debt of $100,000 for partnership accounts payable…arrow_forwardTo acquire a 1/3 interest in the T LLC (a partnership), on January 1 of this year D contributed some land he held for investment. He purchased the land for $120,000. Unfortunately, the land decreased in value and was only worth $90,000 on the date of contribution. A few years later, T LLC sells the land for $84,000. At the beginning of that year, D's capital account was $200,000. Compute the gain or loss to T LLC when it sold the land_____________________ Compute the capital account for D immediately after the sale________________arrow_forward

- Dave and his friend Stewart each owns 50 percent of KBS. During the year, Dave received $96,000 compensation for services he performed for KBS during the year. He performed a significant amount of work for the entity, and he was heavily involved in management decisions for the entity (he was not a passive investor in KBS). After deducting Dave's compensation, KBS reported taxable income of $38,400. How much FICA and/or self-employment tax is Dave required to pay on his compensation and his share of the KBS income if KBS is formed as a C corporation, an S corporation, or a limited liability company (taxed as a partnership) (ignore the 0.9 percent additional Medicare tax)? How much FICA tax would the entity be required to pay on the compensation paid to Dave? Note: Do not round any percentage calculations. Round other intermediate calculations and final answers to the nearest whole dollar amount. C Corporation S Corporation Limited liability company FICA Tax that Dave pays FICA Tax that…arrow_forwardOn January 1, 2023, Kinney, Inc., an S corporation, reports $33,600 of accumulated E & P and a balance of $84,000 in AAA. Kinney has two shareholders, Erin and Frank, each of whom owns 500 shares of Kinney's stock. Kinney's nonseparately stated ordinary income for the year is $42,000. Kinney distributes $50,400 to each shareholder on July 1, and it distributes another $25,200 to each shareholder on December 21. How are the shareholders taxed on the distributions? Ignore the 20% QBI deduction. Do not round intermediate computations. If required, round your final answers to the nearest dollar. Erin and Frank each report $ dividend income for the July 1 distribution and $ distribution. Assuming that the shareholders have sufficient basis in their stock, Erin and Frank each receive a tax-free distribution from AAA. $ each for the December 21arrow_forwardMr. Beaver and Ms. Duck decide to form a new corporation named BD Inc. Mr. Beaver transfers $20,000 cash, equipment (FMV $40,000; adjusted tax basis $41,500) and business inventory ($20,000 FMV; adjusted tax basis $12,000), and Ms. Duck drafts the legal documents and designs the accounting and information systems for BD. These services are valued at $10,000. BD issues 1000 shares of common stock to its two shareholders. a. How many shares should Mr. Beaver and Ms. Duck each receive? Beaver __________ Duck __________ b. Compute Mr. Beaver’s realized and recognized gain on his exchange of property for stock, and determine his tax basis in his BD common shares. Beaver realized gain ______________ Beaver recognized gain ___________ Beaver’s basis in BD stock _________ c. Compute Ms. Duck’s realized and recognized gain on her exchange of services for stock, and determine her tax basis in her BD common shares. Duck realized gain ______________ Duck recognized gain ___________…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education