ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

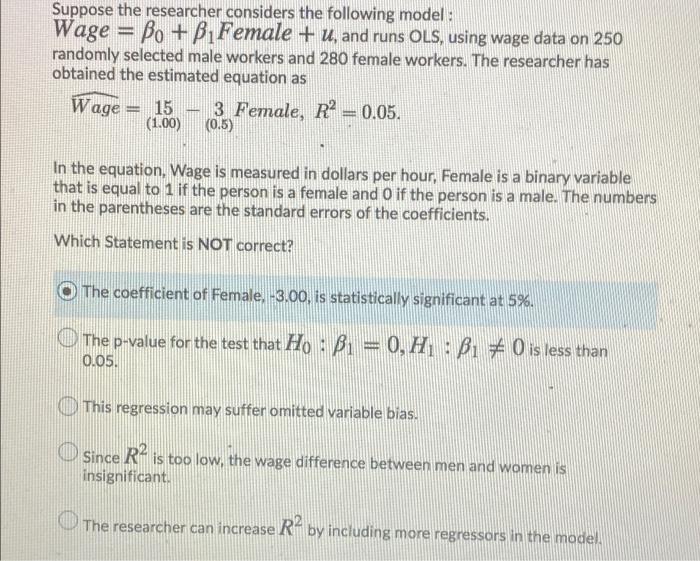

Transcribed Image Text:Suppose the researcher considers the following model :

Wage = Bo+B,Female + u, and runs OLS, using wage data on 250

randomly selected male workers and 280 female workers. The researcher has

obtained the estimated equation as

Wage = 15

(1.00)

3 Female, R = 0.05.

(0.5)

In the equation, Wage is measured in dollars per hour, Female is a binary variable

that is equal to 1 if the person is a female and O if the person is a male. The numbers

in the parentheses are the standard errors of the coefficients.

Which Statement is NOT correct?

The coefficient of Female, -3.00, is statistically significant at 5%.

O The p-value for the test that Ho: B = 0, H : B 0 is less than

0.05.

This regression may suffer omitted variable bias.

R

Since

insignificant.

is too low, the wage difference between men and women is

The researcher can increase R- by including more regressors in the model.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- "In the regression model InY=b0+b1*InX+u, the coefficient b1 is interpreted as" O the intercept O A covariance O A regressor O An elasticityarrow_forwardThe following data from a random sample of individuals that are 25 years old. Note, wage is the hourly earnings in US dollars and educ is years of education. i 1 2 3 4 wage 12.18 12.18 20.09 7.39 educ 13 11 16 12 Consider the following model: In(wage)-Bo+B₁educ+u. Calculate the estimate of B₁. Round your answer to two decimal places.arrow_forwardThe measure of standard error can also be applied to the parameter estimates resulting from linear regressions. For example, consider the following linear regression equation that describes the relationship between education and wage: WAGE: = Bo + B₁ EDUC; + &i where WAGE; is the hourly wage of person i (i.e., any specific person) and EDUC; is the number of years of education for that same person. The residual ₂ encompasses other factors that influence wage, and is assumed to be uncorrelated with education and have a mean of zero. Suppose that after collecting a cross-sectional data set, you run an OLS regression to obtain the following parameter estimates: WAGE;= -10.7+ 3.1 EDUC; If the standard error of the estimate of B₁ is 1.04, then the true value of B₁ lies between grows, you would expect this range to in size. and . As the number of observations in a data setarrow_forward

- The measure of standard error can also be applied to the parameter estimates resulting from linear regressions. For example, consider the following linear regression equation that describes the relationship between education and wage: WAGEi=β0+β1EDUCi+εi where WAGEi is the hourly wage of person i (i.e., any specific person) and EDUCiEDUCi is the number of years of education for that same person. The residual εiεi encompasses other factors that influence wage, and is assumed to be uncorrelated with education and have a mean of zero. Suppose that after collecting a cross-sectional data set, you run an OLS regression to obtain the following parameter estimates: WAGEi=−12.3+4.4 EDUCi If the standard error of the estimate of β1 is 1.29, then the true value of β1 lies between (2.465, 3.11, 3.755, 1.82) and (5.69, 6.98, 5.045) . As the number of observations in a data set grows, you would expect this range to (INCREASE OR DECREASE) in size.arrow_forwardE3arrow_forwardplease answer in text form and in proper format answer with must explanation , calculation for each part and steps clearlyarrow_forward

- Consider the following regression estimates (FN2) Linear regression belavg abvavg female married _cons b. 1 wage O C. 5 O d. 4 Robust Coef. Std. Err. 3047845 3150202 2820787 -1.063254 .0693348 -2.751963 .9686236 .2612646 6.699098 .2889831 Number of obs F(4, 1255) Prob > F R-squared Root MSE t P>|t| -3.49 0.001 0.22 0.826 -9.76 0.000 3.71 0.000 23.18 0.000 |||||||||| = = .45606 6.132155 = -1.661197 -.5486894 -3.305361 = = [95% Conf. Interval] 1,260 56.35 0.0000 0.1121 4.3987 assume that MLR 1-6 hold. In the regression above, how many coefficients (including the constant) are statistically significant at the 1% level? a. 3 -.4653108 .687359 -2.198565 1.481187 7.266042arrow_forwardUse matrices to solve the following pairs of simultaneous equations: 3x + 4y = -1 and 5x - y = 6arrow_forwardExplain the OLS Estimator in Multiple Regression in detail?arrow_forward

- Consider the population regression of log earnings [Y;, where Y,= In(Earnings,;)] against two binary variables: whether a worker is married (D₁, where D₁;= 1 if the th person is married) and the worker's gender (D2;, where D₂;= 1 if the th person is female), and the product of the two binary variables Y₁ = Po+B₁D₁+P₂D2i + P3 (D₁¡ × D₂i) + Hi- The interaction term: O A. indicates the effect of being married on log earnings. B. does not make sense since it could be zero for married males. C. allows the population effect on log earnings of being married to depend on gender. D. cannot be estimated without the presence of a continuous variable.arrow_forwardSuppose we are interested in evaluating the impact on wages of being a college graduate and of residing in California. To this end we define the following dummy variables if college graduate if not college graduate coll = ncoll = if not college graduate if college graduate 1 cali = if residing in California S 1 if not residing in California ncali = if not residing in California if residing in California and for wages denoting yearly wages, we estimate the following model of returns to education wages = B1 coll+ B2ncoll + B3 cali + B4(coll x cali) + e where E[e|coll, cali] = 0. Which parameter or combination of parameters measures the increase in expected wages from obtaining a college degree (comparing to not having a college degree) when residing California? O a. None of the other options is correct O b. Bi – B2 O c. B1 – B2 + ß4 O d. B4 O e. Bi + B3 – ßi – B4 O f. Bi + B4 – ß2 – B4 Clear my choicearrow_forwardFind the degrees of freedom in a regression model that has 10 observations and 7 independent variablesarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education