ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Economics

Options for the first 3 blanks (increase, derease, no change,)

Option for last: rational expectations theory, monetarism, keynesian theory

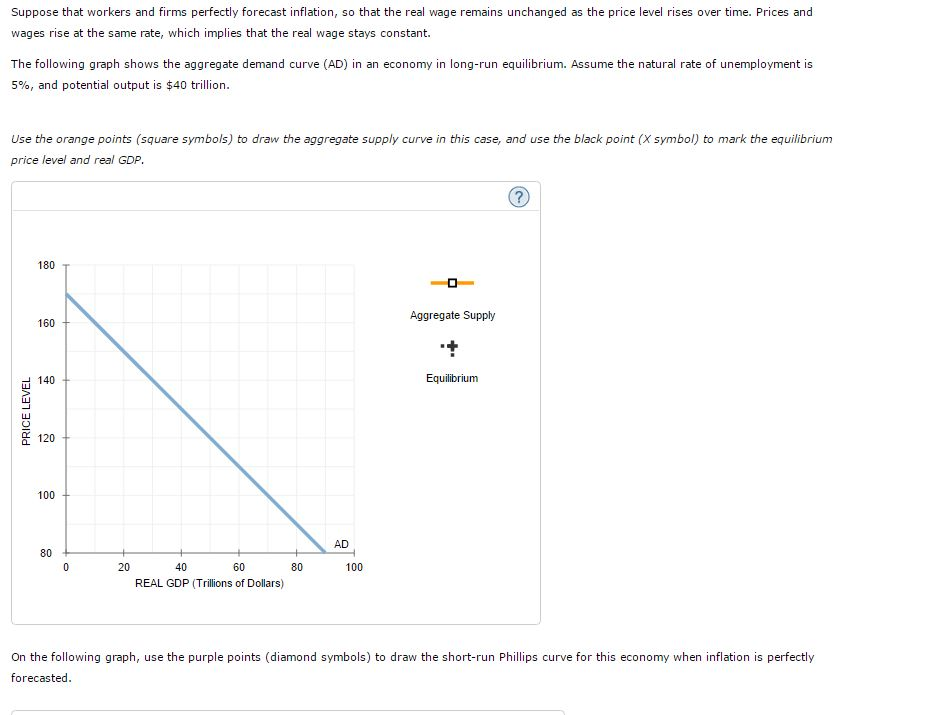

Transcribed Image Text:Suppose that workers and firms perfectly forecast inflation, so that the real wage remains unchanged as the price level rises over time. Prices and

wages rise at the same rate, which implies that the real wage stays constant.

The following graph shows the aggregate demand curve (AD) in an economy in long-run equilibrium. Assume the natural rate of unemployment is

5%, and potential output is $40 trillion.

Use the orange points (square symbols) to draw the aggregate supply curve in this case, and use the black point (X symbol) to mark the equilibrium

price level and real GDP.

PRICE LEVEL

180

160

140

120

100

80

0

20

40

60

REAL GDP (Trillions of Dollars)

80

AD

100

Aggregate Supply

Equilibrium

?

On the following graph, use the purple points (diamond symbols) to draw the short-run Phillips curve for this economy when inflation is perfectly

forecasted.

Transcribed Image Text:On the following graph, use the purple points (diamond symbols) to draw the short-run Phillips curve for this economy when inflation is perfectly

forecasted.

INFLATION RATE (Percent)

10

8

0

0

2

4

6

UNEMPLOYMENT RATE (Percent)

8

10

Short run Phillips curve

(?)

Now suppose the Federal Reserve increases the money supply. Assume that an increase in the equilibrium price level translates into a higher level of

inflation, and a decrease in the price level translates into a lower level of inflation. The effect of the Fed's policy is

in the inflation.

rate,

in the unemployment rate, and

▼in real GDP.

The school of economic thought most closely associated with this analysis is

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Price Level P P Q AS₂ Multiple Choice AS₁ Y₁ Real GDP e3 A shift from AS₁ to AS2 would be consistent with what economic event in U.S. history? demand-pull inflation in the late 1960s cost-push inflation in the mid-1970s full-employment in the late 1990s AS3 Great Recession in 2007-2009 AD₁arrow_forwardMatch the statement to whether it describes rational expectations or adaptive expectations: A. Decisions are relatively slow to respond to new information about the economy B. If people expect it to rain a lot next month, they will start buying umbrellas today to take advantage of the relatively lower prices 1. Rational expectations 2. Adaptive expectationsarrow_forwardPlease answer question. Thanks.arrow_forward

- (23) Assume that the economy begins in long-run equilibrium and that the federal reserve decides to use open market operations to sell bonds. In the short run, what happens to the price level? Group of answer choices (A) It goes down. (B) It goes up. (C) It stays the same.arrow_forwardPick one answer for each question. 1. According to a neoclassical economist, the government should respond to a decrease in aggregate demand by ______. A. raising interest rates B. doing nothing C. balancing the budget 9. From a neoclassical perspective, the Phillips curve is vertical because ______. A. long-run unemployment is fixed at the natural rate of unemployment B. long-run aggregate supply is always the same as short-run aggregate supply c. the inflation rate is fixed in the long-runarrow_forwardI'd like help on first 3 subsectionsarrow_forward

- What does a decrease in federal government purchases do to the Neo-Keynesian model used in class? Group of answer choices It shifts long run aggregate supply left. It shifts long run aggregate supply right. It shifts short run aggregate supply left. It shifts aggregate demand left. It shifts short run aggregate supply right. It shifts aggregate demand right.arrow_forwardQ : Explain what it means that the phillips curve presents policy makers with a menu of choices?arrow_forwardAccording to the Rational Expectation Theory, A) people reformulate their expectations of inflation once a change in the inflation rate has occurred. B) people never reformulate their expectations of inflation. C) expectations of inflation are based only on past values of the inflation rate. D) people reformulate their expectations of inflation once a change in policy has occurred. E) none of the above.arrow_forward

- The Phillips curve is the relationship between (a) Change in GDP from potential and inflation. (b) GDP and unemployment. (c) The percent change in GDP and inflation. (d) The percent change in GDP and unemployment.arrow_forwardInflation redistributes wealth from creditors to debtors when inflation is Question 10 options: high, whether it is expected or not. low, whether it is expected or not. unexpectedly high. unexpectedly low.arrow_forwardExplain different approaches – Neo Keynesian, Friedman, and Lucas – of Philips curve in the short – run and Phillips curve in the long – runarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education