Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

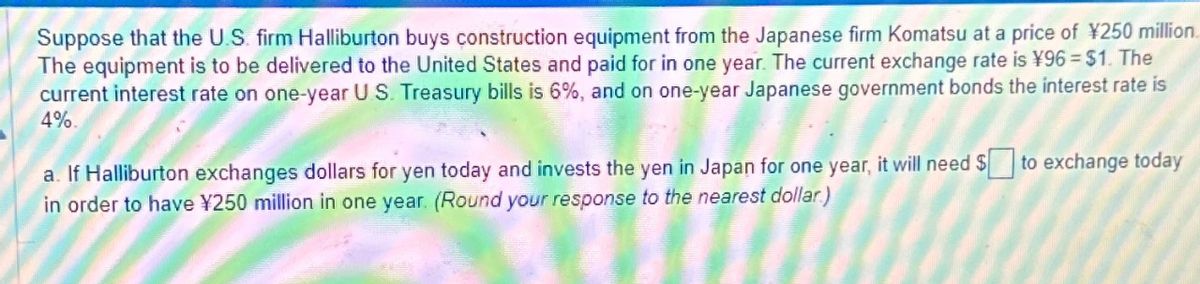

Transcribed Image Text:Suppose that the U.S. firm Halliburton buys construction equipment from the Japanese firm Komatsu at a price of ¥250 million

The equipment is to be delivered to the United States and paid for in one year. The current exchange rate is ¥96 = $1. The

current interest rate on one-year U.S. Treasury bills is 6%, and on one-year Japanese government bonds the interest rate is

4%.

a. If Halliburton exchanges dollars for yen today and invests the yen in Japan for one year, it will need to exchange today

in order to have ¥250 million in one year. (Round your response to the nearest dollar)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Manshukharrow_forwardSuppose that Retrojo Inc. is a U.S. based MNC that will need to purchase F$1.10 million (Fijian dollars, F$) worth of imports from Fiji in 90 days. Currently, the spot rate for the Fijian dollar is $0.53 per F$. If Retrojo were to exchange U.S. dollars for the required F$1,100,000.00 Fijian dollars, it would need $ (U.S. dollars). If Retrojo waits 90 days to make this exchange (perhaps due to insufficient funds on hand), and the Fijian dollar appreciates to $0.64 during those 90- days, then Retrojo would need $ (U.S. dollars). Thus, if Retrojo believes that the Fijian dollar will appreciate, it can its exposure to such exchange rate risk by locking in the original exchange rate through the use of a forward contract.arrow_forwardSuppose that the U.S. firm Halliburton buys construction equipment from the Japanese firm Komatsu at a price of ¥300 million. The equipment is to be delivered to the United States and paid for in one year. The current exchange rate is ¥100 = $1. The current interest rate on one-year U.S. Treasury bills is 6%, and on one-year Japanese government bonds the interest rate is 4%. a. If Halliburton exchanges dollars for yen today and invests the yen in Japan for one year, it will need $ to exchange today in order to have ¥300 million in one year. (Round your response to the nearest dollar)arrow_forward

- OneUSF, a U.S. MNC based in Florida, is considering making a fixed direct investment in Italy. The Italian government has offered OneUSF a concessionary loan of €2,700,000 at a rate of 3 percent per annum. The current spot rate is $1.36/€1.00 and the expected inflation rate is 4% in the U.S. and 2% in Italy. The normal borrowing rate is 7 percent in dollars and 6 percent in euros. The loan schedule calls for the principal to be repaid in three equal annual installments. The marginal corporate tax rate in Italy and the U.S. is 35%. What is the present value of the benefit of the concessionary loan? (Please keep 2 digits in decimals to get the right answer) $117,160 None of the above with the $10,000 of the correct answer $51,360 $1,165,209 $1,310,116arrow_forwardA UK company owes an American company $100,000 due to be paid in three months. The company wishes to avoid exchange rate risk, so borrows enough in sterling now and converts it immediately to dollars which are invested to bring in the required amount in three months' time. The following information is available: Spot rate $/£ 1.7755 - 1.7765 3-month interest rates: Sterling 3.250% US dollar 2.425% How much will the UK company have to borrow now to clear the debt in three months? A. £54,958 B. £54,989 £56,744 D. £56,775 C.arrow_forwardA U.S. firm, sells merchandise today to a British company for £100,000. The current exchange rate is $1.38/£, the account is payable in three months, and the firm chooses to hedge by borrowing £98,765.43 today and exchanging the proceeds today for dollars; the loan will be paid back with the £100,000 accounts receivable (money market hedge). If Husky converted the borrowed pounds into dollars today and invested that amount at its WACC of 6% (1.5% for 90 days), how much much money in U.S. dollars will Husky Sporting Goods Company have in 90 days?arrow_forward

- Boeing just signed a contract to sell a Boeing 737 aircraft to Air France. Air France will be billed €19 million which is payable in one year. The current EUR/USD rate is 1.0651 and the one-year forward rate is 1.0898. The annual interest rate is 4.9% in the U.S. and 2.7% in France. Boeing is concerned with the volatile exchange rate between the dollar and the euro and would like to hedge exchange exposure. It is considering to hedge borrowing euros from Credit Lyonnaise against the euro receivable. How much will they receive in one year? (USD, no cents) The answer is 20,670,407 I cannot figure out how. Thanks!arrow_forwardLakonishok Equipment has an investment opportunity in Europe. The project costs €15,200,000 and is expected to produce cash flows of €3, 800,000 in Year 1, €4, 800,000 in Year 2, and €5, 200,000 in Year 3. The current spot exchange rate is $.83/€ and the current risk - free rate in the United States is 2.6 percent, compared to that in euroland of 2.1 percent. The appropriate discount rate for the project is estimated to be 11 percent, the U.S. cost of capital for the company. In addition, the subsidiary can be sold at the end of three years for an estimated €9, 700,000. What is the NPV of the project in U.S. dollars? (Do not round intermediate calculations and enter your answer in dollars, not in millions of dollars, rounded to 2 decimal places, e.g., 1,234,567.89.)arrow_forwardABC Company wants to possibly expand its plant in Europe. The current spot exchange rate is for Euro is €0.83. The initial investment is €2.1, with projected cash flows for three years at €950,000. The discount rate is 10%. The risk-free rate in the US is 5 percent and the risk-free rate in Europe is 7 percent. Calculate the NPV of the project into US Dollars, rounding to the nearest cent, format as "XXX,XXX.XX"arrow_forward

- Consider this case: Sebrele Enterprises Inc. is a U.S. firm evaluating a project in Australia. You have the following information about the project: The project requires an investment of AU$915,000 today and is expected to generate cash flows of AU$900,000 at the end of each of the next two years. The current exchange rate of the U.S. dollar against the Australian dollar is $0.7823 per Australian dollar (AUS). The one-year forward exchange rate is $0.8102 / AU$, and the two-year forward exchange rate is $0.8412 / AU$. The firm's weighted average cost of capital (WACC) is 9.5%, and the project is of average risk. What is the dollar-denominated net present value (NPV) of this project? $610,602 $726,908 $581,526 $639,679arrow_forwardSun Bank USA has purchased a 8 million one-year Australian dollar loan that pays 12 percent interest annually. The spot rate of U.S. dollars for Australian dollars (AUD/USD) is $0.625/A$1. It has funded this loan by accepting a British pound (BP)-denominated deposit for the equivalent amount and maturity at an annual rate of 10 percent. The current spot rate of U.S. dollars for British pounds (GBP/USD) is $1.60/£1. a. What is the net interest income earned in dollars on this one-year transaction if the spot rate of U.S. dollars for Australian dollars and U.S. dollars for BPs at the end of the year are $0.588/A$1 and $1.848/£1, respectively? (Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Round your final answer to the nearest whole number. (e.g., 32)) b. What should the spot rate of U.S. dollars for BPs be at the end of the year in order for the bank to earn a net interest income of $200,000 (disregarding any change in principal values)?…arrow_forwardSun Bank USA has purchased a 16 million one-year Australian dollar loan that pays 12 percent interest annually. The spot rate of U.S. dollars for Australian dollars (AUD/USD) is $0.757/A$1. It has funded this loan by accepting a British pound (BP)-denominated deposit for the equivalent amount and maturity at an annual rate of 10 percent. The current spot rate of U.S. dollars for British pounds (GBP/USD) is $1.320/£1. a. What is the net interest income earned in dollars on this one-year transaction if the spot rate of U.S. dollars for Australian dollars and U.S. dollars for BPs at the end of the year are $0.715/A$1 and $1.520/£1, respectively? (Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers in dollars, rather than in millions of dollars. Round your final answer to the nearest whole dollar. (e.g., 32)) b. What should the spot rate of U.S. dollars for BPs be at the end of the year in order for the bank to earn a net interest…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education