ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

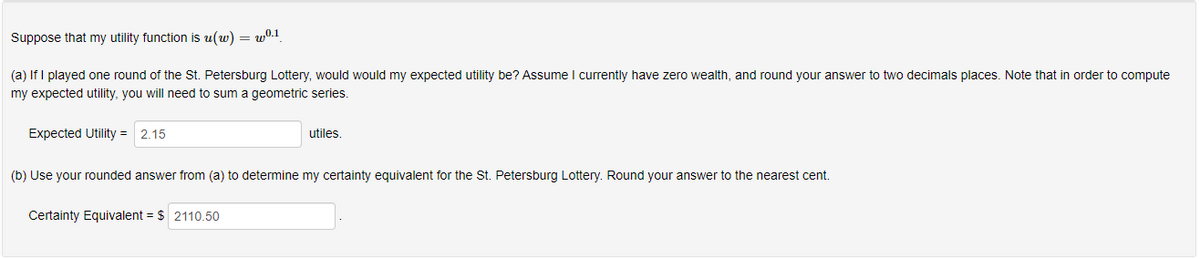

Transcribed Image Text:Suppose that my utility function is u(w) = wº.1

(a) If I played one round of the St. Petersburg Lottery, would would my expected utility be? Assume I currently have zero wealth, and round your answer to two decimals places. Note that in order to compute

my expected utility, you will need to sum a geometric series.

Expected Utility = 2.15

utiles.

(b) Use your rounded answer from (a) to determine my certainty equivalent for the St. Petersburg Lottery. Round your answer to the nearest cent.

Certainty Equivalent = $ 2110.50

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 5 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider the lottery that assigns a probability T of obtaining a level of consumption CH and a probability 1-T an individual facing such a lottery with utility function u(c) that has the properties that more is better (that is, a strictly positive marginal utility of consumption at all levels of c) and diminishing marginal utility of consumption, u"(c) CL. Consider du(c) for the first derivative of the utility function with respect to dc du(c) du' (c) consumption and u"(c) (which is also the derivative of the first derivative of the utility function). to be the second derivative of the utility function dc dc2 1. Provide a definition for the certainty equivalent level of consumption for the simple lottery described above.arrow_forwardplease only do: if you can teach explain each partarrow_forwardThelma is indifferent between $100 and a bet with a 0.6 chance of no return and a 0.4 chance of $200. If U(0) = 20 and U(200) = 220, then U(100) = :arrow_forward

- answer this properly, remember (0.35x50)+(0.65x10)=£24 herearrow_forwardProspect Y = ($6, 0.25 ; $15, 0.75) If Will's utility of wealth function is given by u(x)=x0.25, what is the value of CE(Y) for Will? (In other words, what is Will's certainty equivalent for prospect Y?) (The certainty equivalent represents the maximum amount a person would be willing to pay to acquire a risky prospect, and equivalently, the lowest price for which they would be willing to sell a risky prospect if they already owned it) (Note: The answer may not be a whole number; please round to the nearest hundredth) (Note: The numbers may change between questions, so read carefully)arrow_forward1 Q1. Jerry has wealth of $60 and derives utility from this according to the utility function U(w) = 1 - Where w is his wealth. Jerry now finds a lottery ticket (the drawing takes place the next day) that offers a 50% chance of winning $5. W a) What is the expected value of Jerry if he takes the lottery ticket? (pay attention, it's not jerry's wealth) b) What is the minimum amount for which Jerry would be willing-to-sell the ticket? (Hint: sets a price of p, and at the minimum amount, the expected utility of selling and not selling should be the same) c) Which is bigger, your answer to (a) or (b), and suggest whether Jerry is a risk averse person based on the previous conclusion? d) If he does not sell the ticket, what is Jerry's cost of risk? (The cost of risk is the difference between the expected wealth and the certainty equivalence)arrow_forward

- Priyanka has an income of £90,000 and is a von Neumann-Morgenstern expected utility maximiser with von Neumann-Morgenstern utility index . There is a 1 % probability that there is flooding damage at her house. The repair of the damage would cost £80,000 which would reduce the income to £10,000. a) Would Priyanka be willing to spend £500 to purchase an insurance policy that would fully insure her against this loss? Explain. b) What would be the highest price (premium) that she would be willing to pay for an insurance policy that fully insures her against the flooding damage?arrow_forwardMax Pentridge is thinking of starting a pinball palace near a large Melbourne university. His utility is given by u(W) = 1 - (5,000/W), where W is his wealth. Max's total wealth is $15,000. With probability p = 0.9 the palace will succeed and Max's wealth will grow from $15,000 to $x. With probability 1 - p the palace will be a failure and he’ll lose $10,000, so that his wealth will be just $5,000. What is the smallest value of x that would be sufficient to make Max want to invest in the pinball palace rather than have a wealth of $15,000 with certainty? (Please round your final answer to the whole dollar, if necessary)arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education